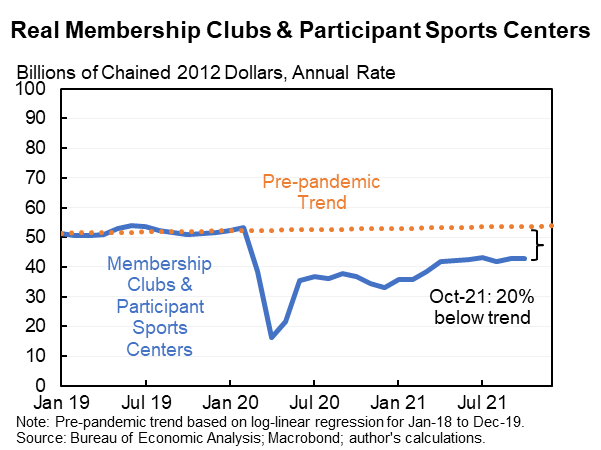

Updated the blog Willie & I posted yesterday to add quits as a measure of labor market tightness (ty @MayankSeksaria). We added it--and the answer is it is the best or nearly the best predictor of nominal wages and Core CPI. piie.com/blogs/realtime…

This matters because quits is even more off-the-charts tight right now than even unemployment/job openings. Which is tighter than unemployment which is tighter than EPOP.

Here's a thread I did on our blog yesterday, doesn't have quits but all the same ideas apply--if anything is a little stronger now.

https://twitter.com/jasonfurman/status/1462944118691315721?s=20

The blog reports more results but you can see the quits story in this picture (actually is 1 - quits so lower means tighter labor market).

• • •

Missing some Tweet in this thread? You can try to

force a refresh