A Small Thread on Chemplast Sanmar

A Chemical Company in the PVC Space !

Dominant producer of paste PVC

2nd Largest in PVC Suspension

EPS CAGR = 37%

A Chemical Company in the PVC Space !

Dominant producer of paste PVC

2nd Largest in PVC Suspension

EPS CAGR = 37%

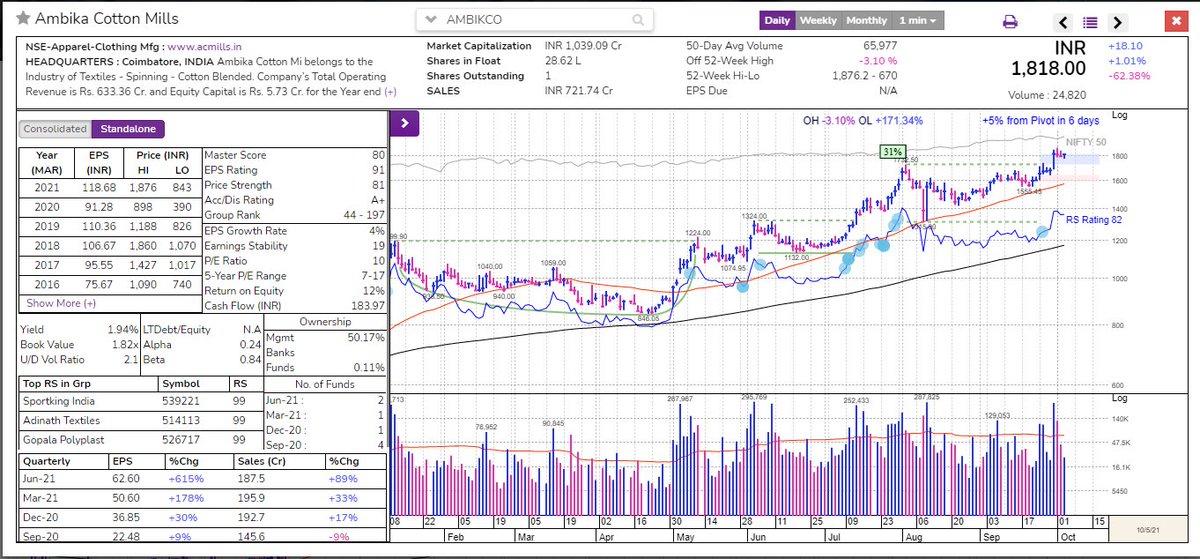

PE 22.5

When ROCE / ROE is above the PE then it generally means that there is a good chance of Revaluation .. ( Backtesting some value winners )

Acc to Management they will be able to sustain the margins to a good level

Execution from management should be good , but lets see

When ROCE / ROE is above the PE then it generally means that there is a good chance of Revaluation .. ( Backtesting some value winners )

Acc to Management they will be able to sustain the margins to a good level

Execution from management should be good , but lets see

Valuation parameters from Screener.in

Margins are improving and currently at 20%+ Excellent

As most speciality chemicals are getting beaten up this might look the same . But now this looks like a good opportunity in my View with base of the Ipo as Stop loss to preserve capital as always

When a sector is downtrend this will follow simple logic

When a sector is downtrend this will follow simple logic

The PVC sector is seeing some rampant development in my view and also the caustic soda prices have dipped and hence could be the fall .. Which if stabilises can improve the Margins of the company

Technicals :

Bouncing off near the IPO Base and also from the Anchored VWAP ( Avg Price of Buying )

Buyers will defend that price

Bouncing off near the IPO Base and also from the Anchored VWAP ( Avg Price of Buying )

Buyers will defend that price

Stop Loss could be IPO day Low if one does want to view it as medium term Investment and not a trade ..

All updates about the company are available in @nid_rockz Timeline as he tracks this company also

https://twitter.com/nid_rockz/status/1454113427798904839?s=20

Buying as an Inv from 585 Levels in the last three days and mentioned many times

Do like share and retweet if you find this a decent pick at a decent time and you find this thread of some knowledge

@ishmohit1 Will soon come with a video on detailed analysis of the Biz. i guess

Do like share and retweet if you find this a decent pick at a decent time and you find this thread of some knowledge

@ishmohit1 Will soon come with a video on detailed analysis of the Biz. i guess

• • •

Missing some Tweet in this thread? You can try to

force a refresh