Friday Musings:

Amidst this taper, my focus is Cloud, Security & AI/ML:

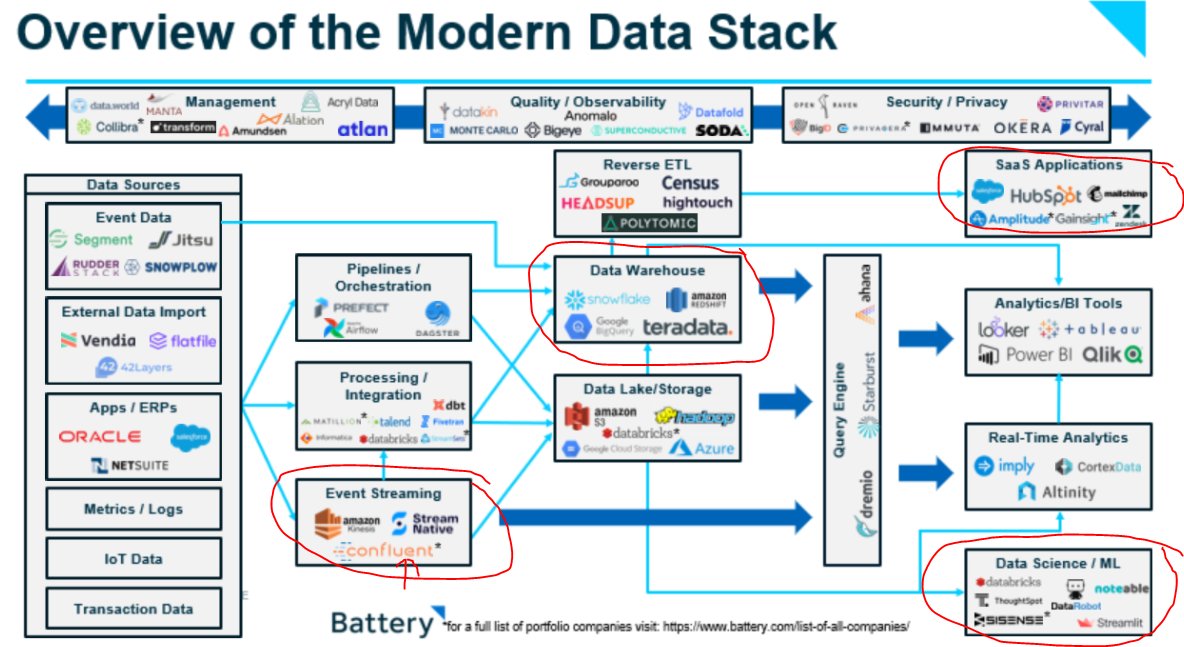

• $SNOW | $S

• $ZS*

• $DDOG*

• $PLTR* | $NET

Non-SaaS:

• $TOST | $DLO

• $GLBE

• $BILL*

• $AFRM*

*Existing positions

+Others: Watchlist

The internet has not broken yet.

Some quick thoughts 1/

Amidst this taper, my focus is Cloud, Security & AI/ML:

• $SNOW | $S

• $ZS*

• $DDOG*

• $PLTR* | $NET

Non-SaaS:

• $TOST | $DLO

• $GLBE

• $BILL*

• $AFRM*

*Existing positions

+Others: Watchlist

The internet has not broken yet.

Some quick thoughts 1/

2/ My priority is to focus on companies that can sustain 30-40% growth rates for a 3-5yr.

The market is looking for companies that have growth PLUS (optionality, product-lock-in, switching costs, mission-critical) to deduce the durability of a 3-yr CAGR to decide its multiple.

The market is looking for companies that have growth PLUS (optionality, product-lock-in, switching costs, mission-critical) to deduce the durability of a 3-yr CAGR to decide its multiple.

3/ Other things is looking for 30%+ CAGR Rev growth combined with lock-in, high land & expand DBNRR?

Alternatively, for non-SaaS companies. I'm looking for companies that are still relatively early in capturing their TAM and are showing qualities that they are market leaders?

Alternatively, for non-SaaS companies. I'm looking for companies that are still relatively early in capturing their TAM and are showing qualities that they are market leaders?

4/ There are MANY value traps that will not recover for years.

The biggest question to ask yourself before buying any dips is-

Based on a company's competitive advantage, what's the durability of their rev growth and eventual earnings power over 3-4yrs based on today's prices?

The biggest question to ask yourself before buying any dips is-

Based on a company's competitive advantage, what's the durability of their rev growth and eventual earnings power over 3-4yrs based on today's prices?

5/ My sympathies to anyone in $ASAN, $DOMO and $DOCU. In my opinion, the extra sting in their severe dip over the last 24-hours is that the markets hates deceleration and doubts the durability of their LT moat/growth.

Vice-versa: Look at strength in $DDOG, $SNOW, $ZS etc.

Vice-versa: Look at strength in $DDOG, $SNOW, $ZS etc.

5i/ The challenge is that the most durable and high-quality companies will not become "cheap" by traditional valuation metrics.. You've gotta pick your spots.

As my friend @convequity points, SaaS companies quality, TAM expansions, and margins are higher than "07, dot com.

As my friend @convequity points, SaaS companies quality, TAM expansions, and margins are higher than "07, dot com.

6/ For GARP'y names:

I've been building a strong position already in $GDYN 2-weeks ago but might add more (This is the strongest name in this market!). GDYN is a AI/ML Tech consultancy in the middle of digital transformation.

Other boring strong SaaS Co's: $FTNT, $PANW, $OKTA

I've been building a strong position already in $GDYN 2-weeks ago but might add more (This is the strongest name in this market!). GDYN is a AI/ML Tech consultancy in the middle of digital transformation.

Other boring strong SaaS Co's: $FTNT, $PANW, $OKTA

7/ Likely things get worse over the upcoming weeks since the Nasdaq is only down 7%. Usually, these corrections bottom at 12%-18%.

This sounds crazy but I've borrowed and transferred new cash into my account as historically, the Fed Taper is the ULTIMATE buying opportunity !!

This sounds crazy but I've borrowed and transferred new cash into my account as historically, the Fed Taper is the ULTIMATE buying opportunity !!

8/ This is an important period to be level-headed.

Personally, I've got lots of work and analysis to do this weekend before deploying my new cash. Will share along if I have enough time.

IMO, we'll look back to this period as a generational buy opportunity. Choose wisely. HAGW!

Personally, I've got lots of work and analysis to do this weekend before deploying my new cash. Will share along if I have enough time.

IMO, we'll look back to this period as a generational buy opportunity. Choose wisely. HAGW!

My portfolio is still very much intact from what I shared last weekend btw.

All the companies above are just some high conviction portfolio names and some watchlist companies that's I'm focused during this period (Dec - Jan 22). Cheers.

All the companies above are just some high conviction portfolio names and some watchlist companies that's I'm focused during this period (Dec - Jan 22). Cheers.

• • •

Missing some Tweet in this thread? You can try to

force a refresh