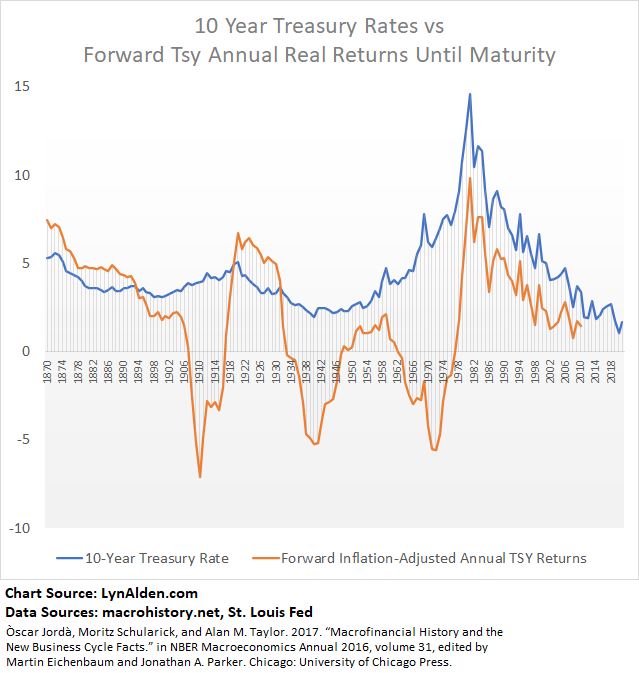

Back in 2020 when a lot of folks were expecting ongoing disinflation, that was actually the bottom and a big inflationary surge was forming.

In late 2021 or early 2022 when a lot of folks are expecting permanent high inflation, that may be a local top for a period.

In late 2021 or early 2022 when a lot of folks are expecting permanent high inflation, that may be a local top for a period.

Inflation in the 1940s and 1970s was cyclical as well.

US job market, European energy, and global supply chains are still inflationary. US fiscal cliff is disinflationary.

Unclear what China will do for the lead up to their late-2022 national congress. Probably reflationary.

US job market, European energy, and global supply chains are still inflationary. US fiscal cliff is disinflationary.

Unclear what China will do for the lead up to their late-2022 national congress. Probably reflationary.

To be clear, the November CPI numbers (reported tomorrow) are still going to be hot with likely new year-over-year cycle highs (housing and used cars both up a lot, for example).

• • •

Missing some Tweet in this thread? You can try to

force a refresh