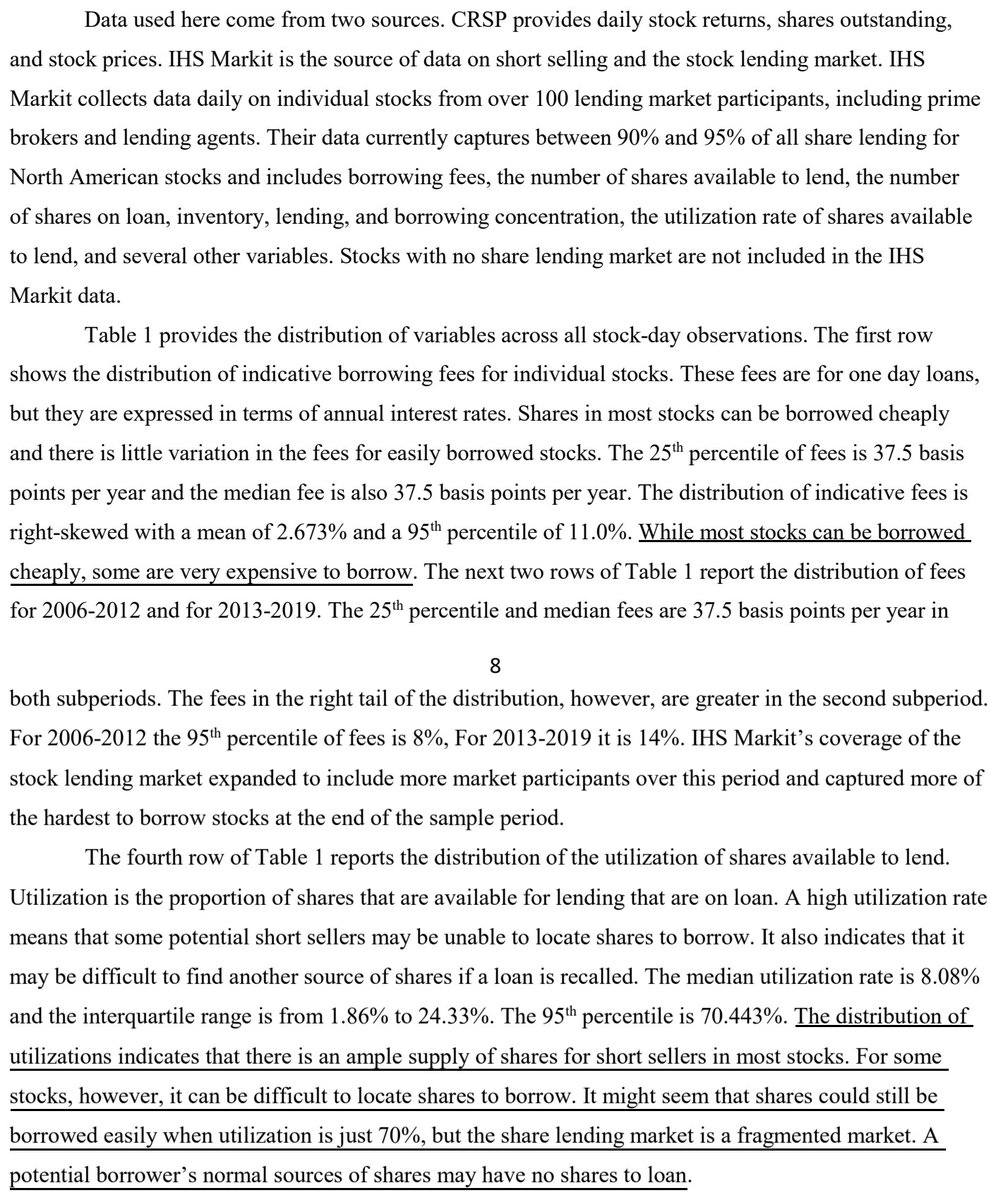

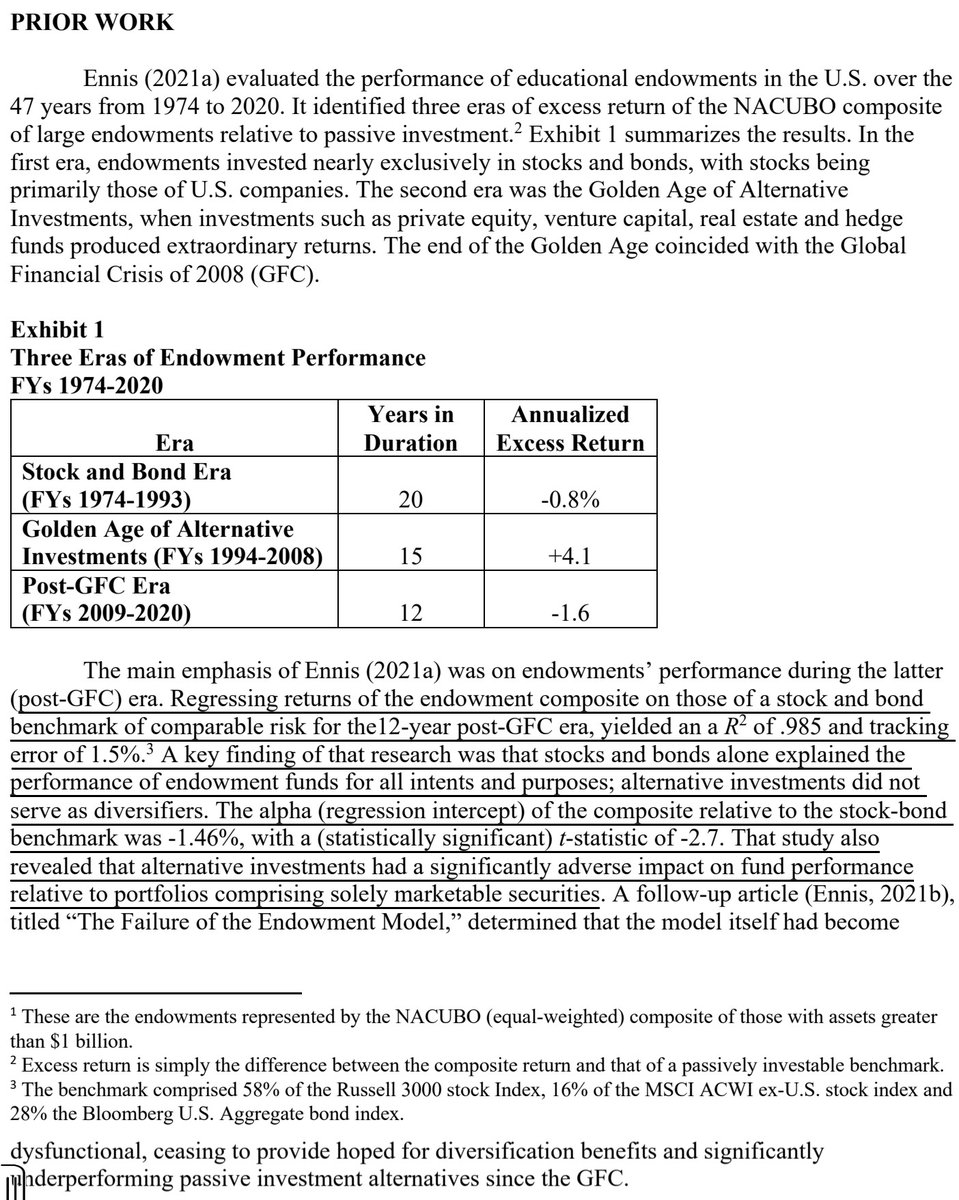

1/ Imagine the board game Risk, quant style.

In the quant version, replace continents with big asset managers.

Instead of country cards, draw 'power up' cards for value, momentum, leverage, etc. that can be hoarded, used in combination, then discarded.

boardgamegeek.com/boardgame/181/…

In the quant version, replace continents with big asset managers.

Instead of country cards, draw 'power up' cards for value, momentum, leverage, etc. that can be hoarded, used in combination, then discarded.

boardgamegeek.com/boardgame/181/…

2/ Value, momentum: +1 defensive, +1 offensive (if attacking, you get +1 and subtract 1 from your partner's dice roll; vice versa if you are defending)

Quality, trend: +2 defensive

Carry: +2 offensive

Growth, market beta: +1 offensive, -1 defensive

Leverage: 2x gains & losses

Quality, trend: +2 defensive

Carry: +2 offensive

Growth, market beta: +1 offensive, -1 defensive

Leverage: 2x gains & losses

3/ As in standard risk, draw a 'power up' card if you end a turn with more territories than when you started. Up to five cards can be hoarded and used when you are either attacking or defending. They can be used during that entire encounter and then discarded.

4/ Quant Risk could be used to explore ideas about diversification, leverage, and position sizing.

It would also be nice to have a finance game that doesn't teach players to constantly overleverage and double down (*cough* Monopoly, Cashflow).

boardgamegeek.com/boardgame/6552…

It would also be nice to have a finance game that doesn't teach players to constantly overleverage and double down (*cough* Monopoly, Cashflow).

boardgamegeek.com/boardgame/6552…

• • •

Missing some Tweet in this thread? You can try to

force a refresh