fascinating @adam_tooze on whether we'll see Russia abandon its Wall Street Consensus macrofinancial regime - fiscal austerity, floating exchange rate, domestic bond finance - that it deployed to accumulate a foreign reserves war chest.

adamtooze.substack.com/p/chartbook-91…

adamtooze.substack.com/p/chartbook-91…

first, the constraint of market access - so very familiar to poor & middle income countries negotiating Debt Service Suspension Initiative - is gone.

if you dont care what foreign investors think of your macro stance, the world is your oyster.

if you dont care what foreign investors think of your macro stance, the world is your oyster.

your oyster as in you can:

1. Choose to reorient your macro choices towards aggressive short-run stabilisation

2. Bring back developmental state that aims to structurally change your economy

both require an ideological cover, and MMT can offer that

1. Choose to reorient your macro choices towards aggressive short-run stabilisation

2. Bring back developmental state that aims to structurally change your economy

both require an ideological cover, and MMT can offer that

problem for short-run demand management: Russia's mon policy rate at 20% + sanctions-related supply bottlenecks that increase inflationary pressures.

So war Keynesianism means it cannot fight inflation via aggregate demand management but price controls (ahem @IsabellaMWeber )

So war Keynesianism means it cannot fight inflation via aggregate demand management but price controls (ahem @IsabellaMWeber )

with extensive price controls, Russia can then unleash massive fiscal expansion - compensation for families of dead soldiers, for massive unemployment caused by sanctions/withdrawal of multinational corporations/loss of export markets

the shortage economy is baaaack!

the state channels petrodollars into war spending + safety net for citizens + industrial policy.

and industrial policy speaks to ideas of transforming the central bank into an 'institute for development'

the state channels petrodollars into war spending + safety net for citizens + industrial policy.

and industrial policy speaks to ideas of transforming the central bank into an 'institute for development'

to be clear, I dont think MMT ever claimed to be a theory of the developmental state.

MMT is a theory of why the macro constraint to a developmental state project is not 'how will we pay for it'.

MMT is a theory of why the macro constraint to a developmental state project is not 'how will we pay for it'.

MMT is right that you cannot have a developmental state project under Wall Street Consensus macrofinance.

but once you make that intellectual leap, slope just gets steeper.

reviving a developmental state project under conditions of war and sanctions is, in my view, impossible

but once you make that intellectual leap, slope just gets steeper.

reviving a developmental state project under conditions of war and sanctions is, in my view, impossible

a developmental state first needs goal for structural transformation - I doubt it would be decarbonisation since this is a a petrodollar state.

traditionally, it used to be industrial upgrading, for which you need export markets - but where? China/African countries?

traditionally, it used to be industrial upgrading, for which you need export markets - but where? China/African countries?

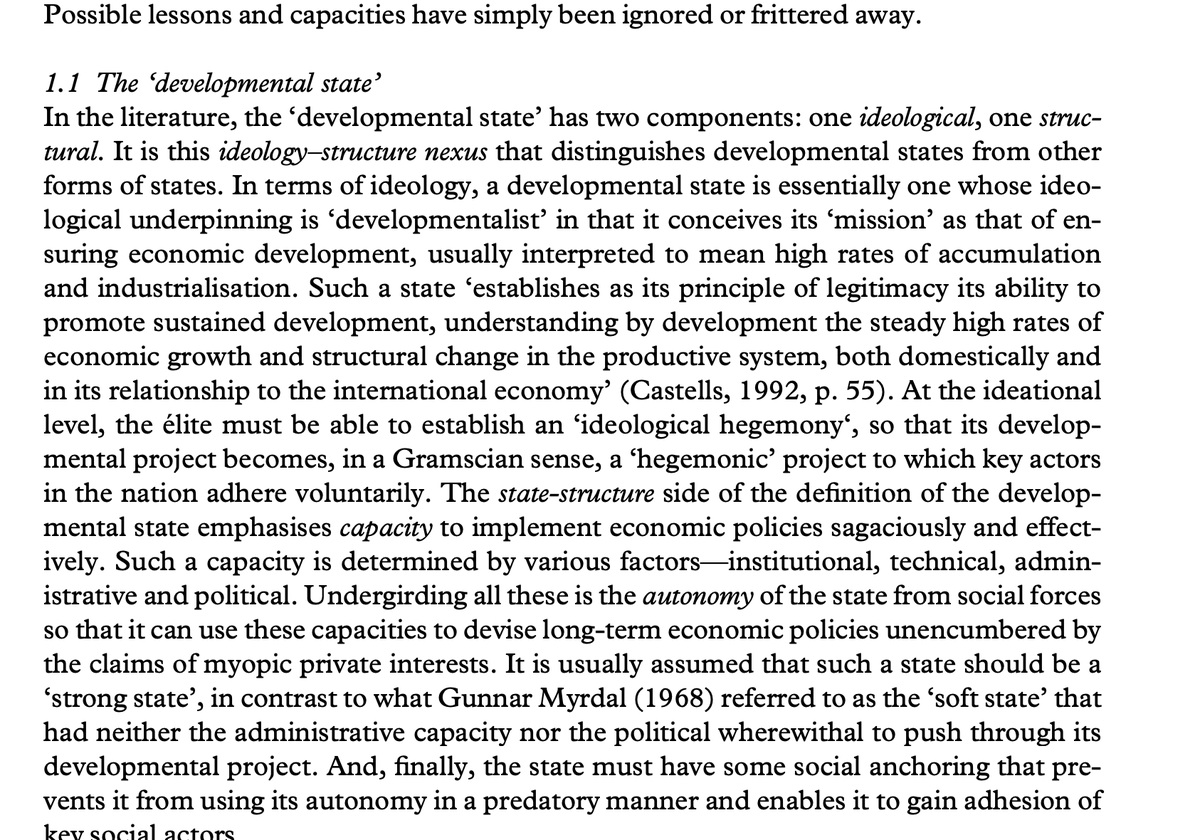

then the Mkandawire test for developmental state:

1. Ideologically, it needs social consensus around developmental project. Being a dictatorship helps.

2. Structurally, it needs technocracy that can design and implement a project that upends a 30 year old macro consensus.

1. Ideologically, it needs social consensus around developmental project. Being a dictatorship helps.

2. Structurally, it needs technocracy that can design and implement a project that upends a 30 year old macro consensus.

With ideology/structure nexus in place, developmental state has to overcome twin financial & technological dependency.

It needs hard cash to import capital/intermediary inputs for new industries it plans to promote.

Russia has hard cash but sanctions make it difficult to use

It needs hard cash to import capital/intermediary inputs for new industries it plans to promote.

Russia has hard cash but sanctions make it difficult to use

Some have argued sanctions won't bite if Russia turns to China/Asia + Africa. But Russia decoupling from 'Western' liberal capitalism doesnt mean countries in Asia/Africa would join it.

And btw I am not an 'optimist' on macrofinancial regime change in Russia - I am just mapping potential avenues. Very skeptical on revival of developmental state, somewhat skeptical on short-run aggressive stabilization

https://twitter.com/SHamiltonian/status/1499677883710664704?t=dOrahRKf2cfZGLgjNssrfw&s=19

mind blown by trolls who think you can run a war economy on tight status-quo macro

yet again, the question inevitably will be what can Russia spend its petrodollars on - cc @dsquareddigest

https://twitter.com/BuddyYakov/status/1499780257745752064?s=20&t=P704saY97NsVm_eXOqD8Iw

@dsquareddigest it may not even be about a new growth model, but the implosion of the existing one

https://twitter.com/DAlperovitch/status/1499639074814058499?s=20&t=P704saY97NsVm_eXOqD8Iw

how many of these can survive under sanctions hitting critical imports @BuddyYakov?

• • •

Missing some Tweet in this thread? You can try to

force a refresh