🐻♉️↗️↘️↔️⚠️🚩🔺🔻🧮 💰

Global Macro Review

September 12, 2022

1/10

Comping against the June lows, equities, yields, and #bitcoin ripped ↗️ as the USD and vol 🌊 ↘️ even as a litany of #FedHeads reaffirmed more 👊🥣 removal

Let’s dig into the 🧮!

Global Macro Review

September 12, 2022

1/10

Comping against the June lows, equities, yields, and #bitcoin ripped ↗️ as the USD and vol 🌊 ↘️ even as a litany of #FedHeads reaffirmed more 👊🥣 removal

Let’s dig into the 🧮!

2/10

The $USD 🎳 paused while ECB, BOC, RBA hiked 75 BPS

$FXY -1.7% (w) -6.0% (T)

$UUP -0.65% (w), +4.9% (T)

$FXA +0.6% (w), -3.0% (T)

$FXE +0.91% (w), -4.75% (T)

$FXC +1.04% (w), -1.9% (T)

$FXF +2.14% (w), +2.6% (T)

Chart: capitulatory selling in $FXY 💴

The $USD 🎳 paused while ECB, BOC, RBA hiked 75 BPS

$FXY -1.7% (w) -6.0% (T)

$UUP -0.65% (w), +4.9% (T)

$FXA +0.6% (w), -3.0% (T)

$FXE +0.91% (w), -4.75% (T)

$FXC +1.04% (w), -1.9% (T)

$FXF +2.14% (w), +2.6% (T)

Chart: capitulatory selling in $FXY 💴

3a/10

Treasury bond ETFs were 🪓 as the $UST10Y +9.8 BPS to 3.3.15%

10/2s to -24.8 BPS

MOVE 121.54 🛗

$TLT -1.75% (w), -4.8% (T)

$TIP -1.05% (w), -5.05% (T)

$IEF -0.85% (w), -1.05% (T)

Chart: $TLT oversold and exploring a double bottom

Treasury bond ETFs were 🪓 as the $UST10Y +9.8 BPS to 3.3.15%

10/2s to -24.8 BPS

MOVE 121.54 🛗

$TLT -1.75% (w), -4.8% (T)

$TIP -1.05% (w), -5.05% (T)

$IEF -0.85% (w), -1.05% (T)

Chart: $TLT oversold and exploring a double bottom

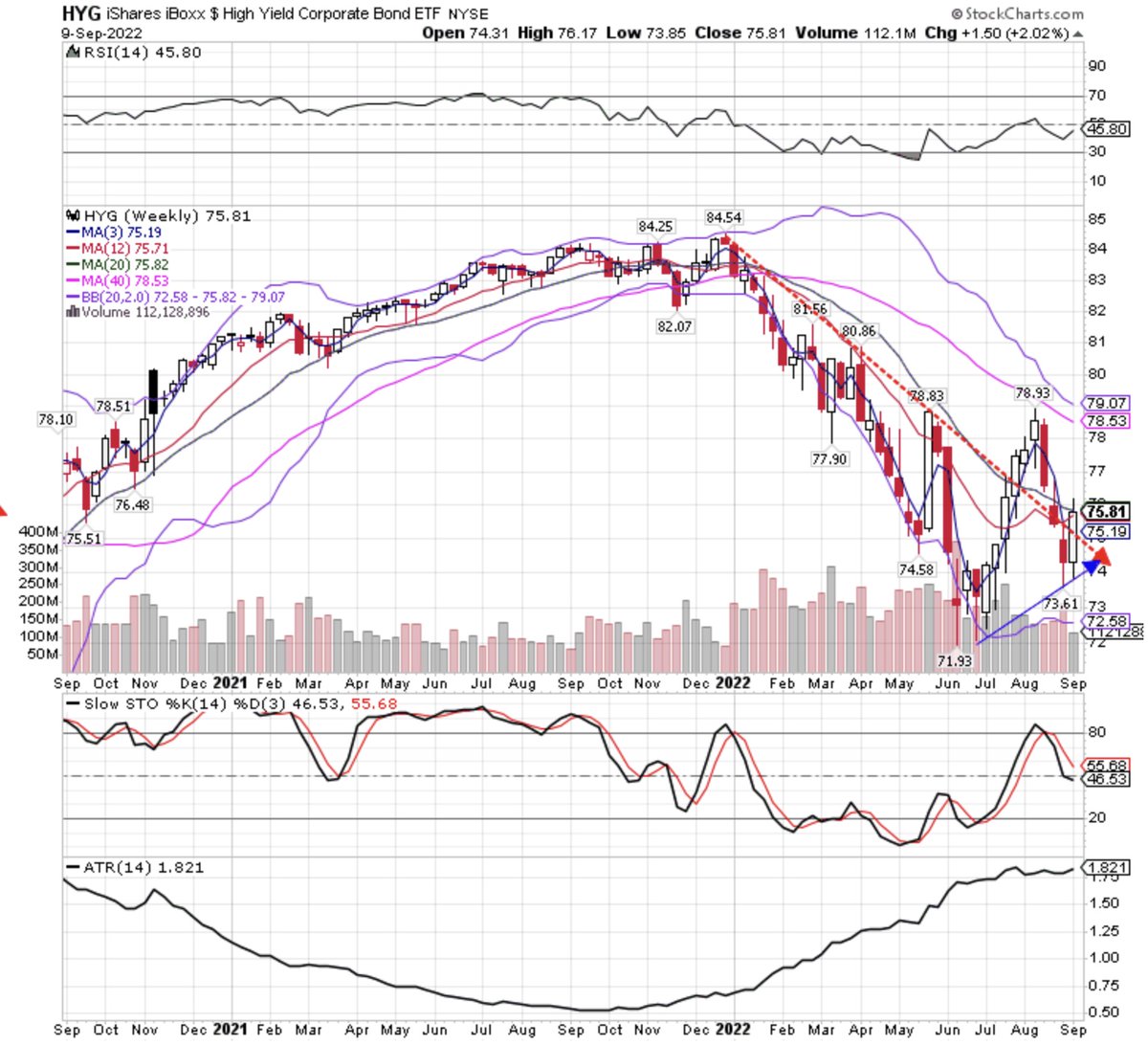

3b/10

Junk and convertibles found a bid ↗️ along with equities

$CWB +2.49% (w), +2.8% (T)

$HYG +2.0%(w), 0.25% (T)

$LQD unch (w), -1.95% (T)

Chart: HYG overbought but with a big higher low

Junk and convertibles found a bid ↗️ along with equities

$CWB +2.49% (w), +2.8% (T)

$HYG +2.0%(w), 0.25% (T)

$LQD unch (w), -1.95% (T)

Chart: HYG overbought but with a big higher low

4/10

Equity vol 🌊 came in ↘️ across the complex

$VIX 22.79 -2.68

$VXN 29.23 -3.09

$RVX 27.29 -2.69

$VSTOXX 24.88 -0.62

$VXEEM 21.22 -3.58

Chart: $VXEEM - EM vol contained within the box lending support to $EEM +0.62%

Equity vol 🌊 came in ↘️ across the complex

$VIX 22.79 -2.68

$VXN 29.23 -3.09

$RVX 27.29 -2.69

$VSTOXX 24.88 -0.62

$VXEEM 21.22 -3.58

Chart: $VXEEM - EM vol contained within the box lending support to $EEM +0.62%

5a/10

🇺🇸 equities 🚀 to ♉️ Trend = (T) = 3 mos price momentum

$SPX +3.65% (w), +2.8% (T)

$IWM +4.05% (w), +4.95% (T)

$COMPQ +4.15% (w), +6.8% (T)

Chart: $COMPQ arrested a 3-week decline but is -7.15% over the past month (t).

🇺🇸 equities 🚀 to ♉️ Trend = (T) = 3 mos price momentum

$SPX +3.65% (w), +2.8% (T)

$IWM +4.05% (w), +4.95% (T)

$COMPQ +4.15% (w), +6.8% (T)

Chart: $COMPQ arrested a 3-week decline but is -7.15% over the past month (t).

5b/10

Every 🇺🇸 sector closed ↗️ on the week

$XLY +5.8% (w), +13.85% (T)

$XLB +5.0% (w), -4.4% (T)

$XLF +4.45% (w), +5.65% (T)

$XLV +4.4% (w), +4.0% (T)

Chart: $XLY consumer discretionary expressing a #quad1 Goldilocks 👱♀️ view

Every 🇺🇸 sector closed ↗️ on the week

$XLY +5.8% (w), +13.85% (T)

$XLB +5.0% (w), -4.4% (T)

$XLF +4.45% (w), +5.65% (T)

$XLV +4.4% (w), +4.0% (T)

Chart: $XLY consumer discretionary expressing a #quad1 Goldilocks 👱♀️ view

6/10

China led internat’l indices ↗️

$SSEC +2.35% (w), -0.7% (T)

$NIKK +2.05% (w), +1.4% (T)

$CAC +0.75% (w), +0.4% (T)

$DAX +0.3% (w), -4.9% (T)

$HSI -0.45% (w), -11.2% (T)

$KOSPI -1.05% (w), -8.15% (T)

Chart: $KOSPI with room to go ↘️

Is there a doctor 👩🏻⚕️ in the house?

China led internat’l indices ↗️

$SSEC +2.35% (w), -0.7% (T)

$NIKK +2.05% (w), +1.4% (T)

$CAC +0.75% (w), +0.4% (T)

$DAX +0.3% (w), -4.9% (T)

$HSI -0.45% (w), -11.2% (T)

$KOSPI -1.05% (w), -8.15% (T)

Chart: $KOSPI with room to go ↘️

Is there a doctor 👩🏻⚕️ in the house?

7/10

Industrial metals ripped ↗️ within 🐻 (T)s

$PLAT +7.15% (w), -9.7% (T)

$SILVER +5.0% (w), -14.4% (T)

$COPPER +4.7% (w), -16.8% (T)

$GOLD +0.35% (w), -7.85% (T)

Chart: Dr. $COPPER with a big higher low

Industrial metals ripped ↗️ within 🐻 (T)s

$PLAT +7.15% (w), -9.7% (T)

$SILVER +5.0% (w), -14.4% (T)

$COPPER +4.7% (w), -16.8% (T)

$GOLD +0.35% (w), -7.85% (T)

Chart: Dr. $COPPER with a big higher low

8/10

Hydrocarbons ↘️ on the week 🛢⛽️

$WTIC -0.1% (w), -28.1% (T)

$BRENT -0.2% (w), -23.85% (T)

$GASO -1.1% (w), -41.75% (T)

$NATGAS -8.9% (w), -9.6% (T) 🐻

Chart: Thanks to Uncle Joe, $GASO ⛽️ -43.9% from the June high 🗳

Hydrocarbons ↘️ on the week 🛢⛽️

$WTIC -0.1% (w), -28.1% (T)

$BRENT -0.2% (w), -23.85% (T)

$GASO -1.1% (w), -41.75% (T)

$NATGAS -8.9% (w), -9.6% (T) 🐻

Chart: Thanks to Uncle Joe, $GASO ⛽️ -43.9% from the June high 🗳

9/10

Grains ↔️ to ↗️ on the week 🌾🌽

$WHEAT +7.2% (w), -18.8% (T)

$CORN +2.9% (w), -11.4% (T)

$SUGAR unch (w), -3.7% (T)

$SOYB -0.7% (w), -19,1% (T)

Chart: $DBA +1.4% (w) finding resistance at fib 38.2

Grains ↔️ to ↗️ on the week 🌾🌽

$WHEAT +7.2% (w), -18.8% (T)

$CORN +2.9% (w), -11.4% (T)

$SUGAR unch (w), -3.7% (T)

$SOYB -0.7% (w), -19,1% (T)

Chart: $DBA +1.4% (w) finding resistance at fib 38.2

10/10

So, the setup is risk assets ↗️ into Tuesday’s #CPI print and #OPEX on Friday.

CPI expectations at +8.1% y/y and the Fed 🦅

I am 🐻 but the big higher lows in $SPX need to be respected, as does Chair Powell

⚠️🚩 and have a super profitable 💰 week!

So, the setup is risk assets ↗️ into Tuesday’s #CPI print and #OPEX on Friday.

CPI expectations at +8.1% y/y and the Fed 🦅

I am 🐻 but the big higher lows in $SPX need to be respected, as does Chair Powell

⚠️🚩 and have a super profitable 💰 week!

• • •

Missing some Tweet in this thread? You can try to

force a refresh