🇷🇺 NEW | Monthly analysis of Russian fossil fuel exports & sanctions

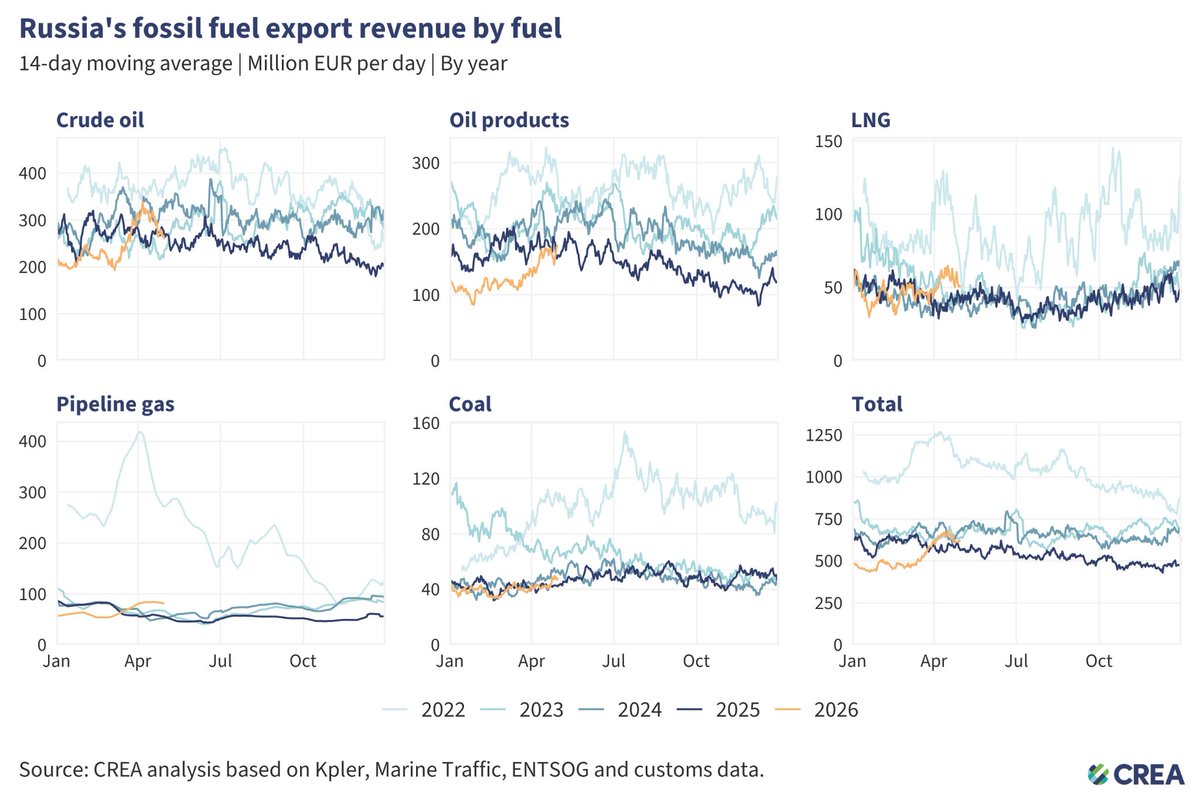

📈In April 2026, Russia’s monthly fossil fuel export revenues rose a further 4% to EUR 734mn / day, the highest in 2.5 years

📈In April 2026, Russia’s monthly fossil fuel export revenues rose a further 4% to EUR 734mn / day, the highest in 2.5 years

🚢Russia’s seaborne crude oil export volumes dropped 24% Month-on-Month, influenced by Ukraine’s drone strikes

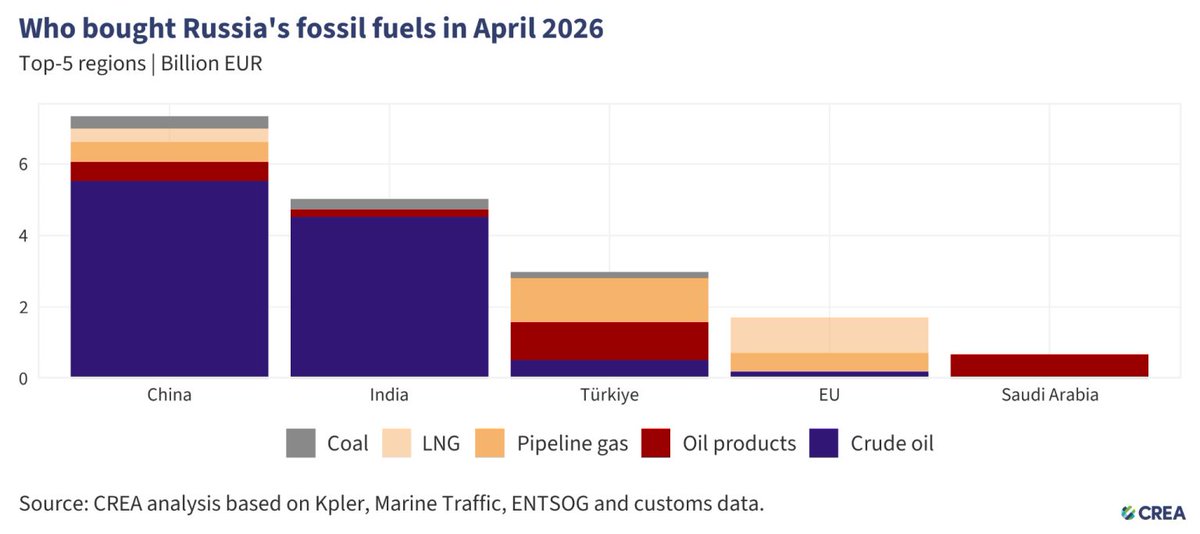

In April, the top importers of RU fossil fuels were:

🇨🇳 China

🇮🇳 India

🇹🇷 Turkiye

🇪🇺 EU

🇸🇦 Saudi Arabia

📉China’s imports of seaborne Russian crude saw a 24% month-on-month decrease, meanwhile, the Dalian refinery unloaded its first shipment since Sept 2025

🇨🇳 China

🇮🇳 India

🇹🇷 Turkiye

🇪🇺 EU

🇸🇦 Saudi Arabia

📉China’s imports of seaborne Russian crude saw a 24% month-on-month decrease, meanwhile, the Dalian refinery unloaded its first shipment since Sept 2025

🛢️India’s total crude imports recorded a 3.7% reduction in April, while volumes from Russia fell 19.4% month-on-month

🇪🇺 Despite the EU’s ban on Russian spot LNG imports taking effect on 25 April 2026, unloaded volumes fell by just 8% month-on-month

🇪🇺 Despite the EU’s ban on Russian spot LNG imports taking effect on 25 April 2026, unloaded volumes fell by just 8% month-on-month

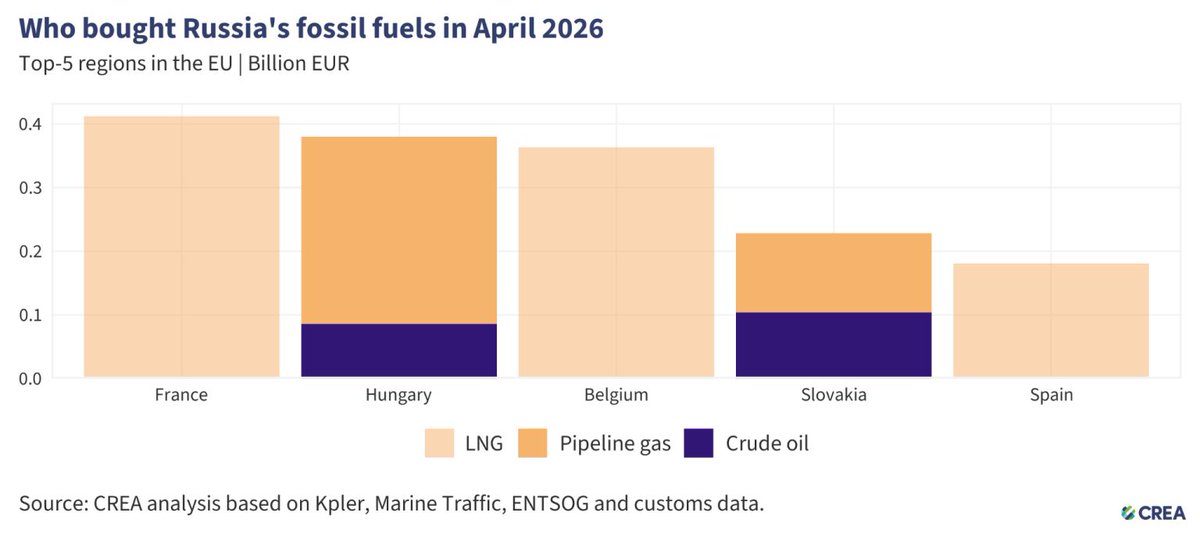

In March, the top EU importers were

🇫🇷 France

🇭🇺 Hungary

🇧🇪 Belgium

🇸🇰Slovakia

🇪🇸 Spain

📈 Russia exported EUR 189mn of crude oil via the Druzhba pipeline in April, delivered to Hungary and Slovakia after the pipeline resumed operations following nearly 3 months of inactivity

🇫🇷 France

🇭🇺 Hungary

🇧🇪 Belgium

🇸🇰Slovakia

🇪🇸 Spain

📈 Russia exported EUR 189mn of crude oil via the Druzhba pipeline in April, delivered to Hungary and Slovakia after the pipeline resumed operations following nearly 3 months of inactivity

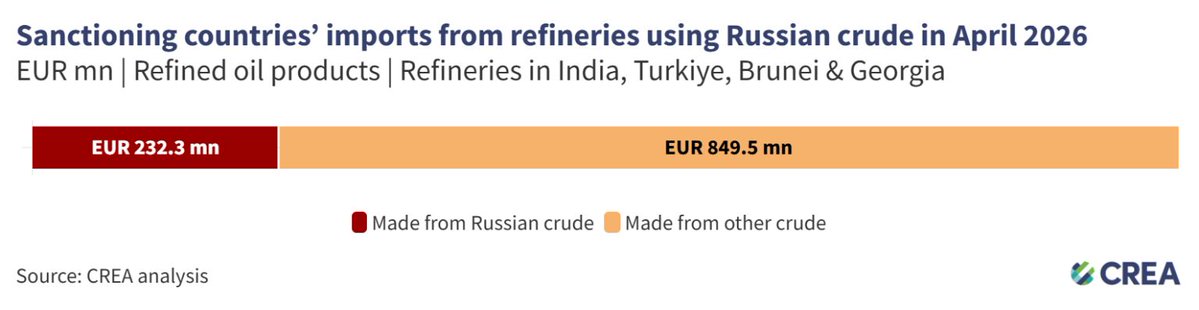

Despite the EU’s ban on oil products made from Russian crude, 8 shipments still unloaded at EU ports from refineries running on Russian crude

Seven of these shipments departed from Turkiye’s refineries and 1 from Georgia

Seven of these shipments departed from Turkiye’s refineries and 1 from Georgia

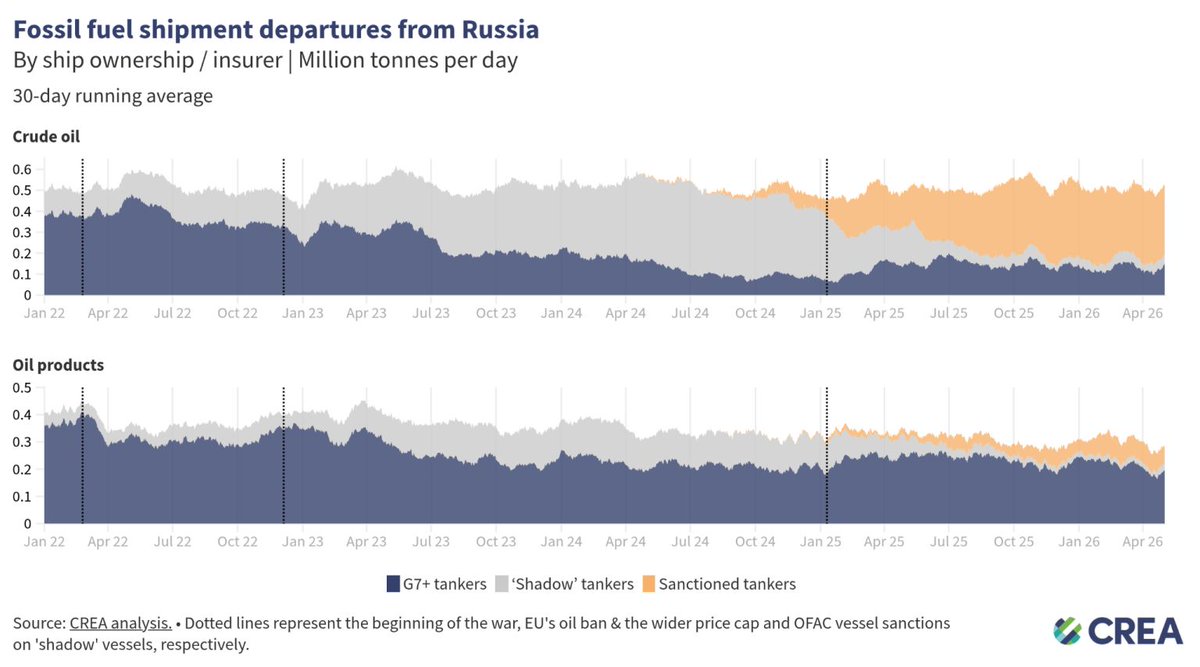

🚢In April 2026, over half (54%) of Russia’s seaborne oil was transported by sanctioned ‘shadow’ tankers, the highest share on record

🏴☠️13% of the 47 false-flag vessels most recently loaded Iranian, not Russian crude or oil products; the majority alternated between the two

🏴☠️13% of the 47 false-flag vessels most recently loaded Iranian, not Russian crude or oil products; the majority alternated between the two

🛑The number of reported detentions and inspections of Russian ‘shadow’ tankers fell from 4 in March 2026 to just 1 in April

A massive oil prices spike following the Strait of Hormuz closure has led to a rethink of a Russian oil maritime services ban to ensure supplies for global markets

CREA reiterates the need to practice strong enforcement of the price cap policy & address attestation fraud to adequately crunch Russian revenues

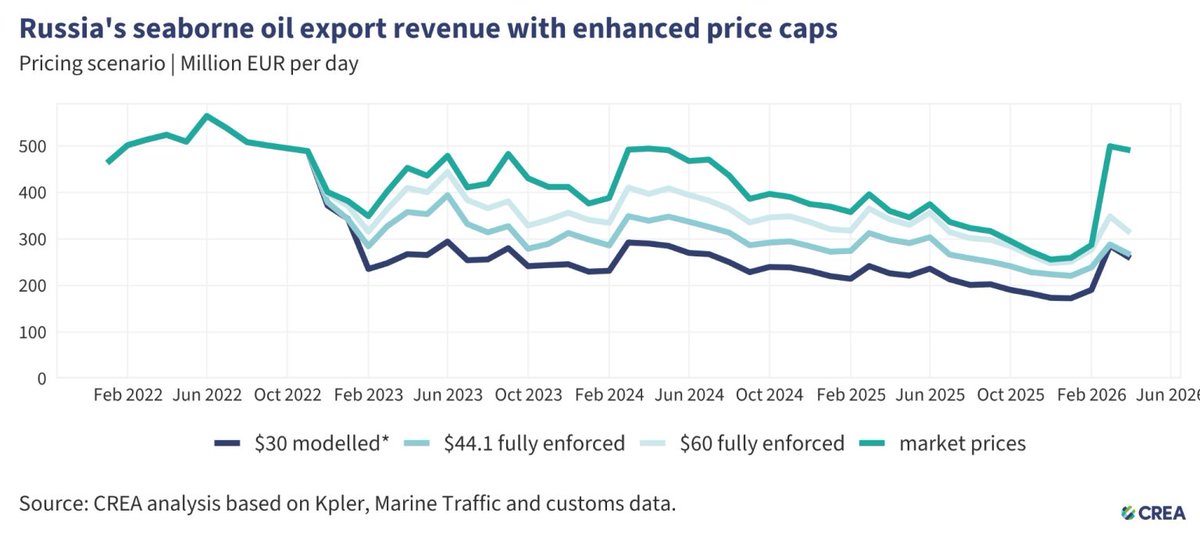

In April 2026, full enforcement of the USD 44.1 per barrel price cap would have reduced revenues by 46%

In April 2026, full enforcement of the USD 44.1 per barrel price cap would have reduced revenues by 46%

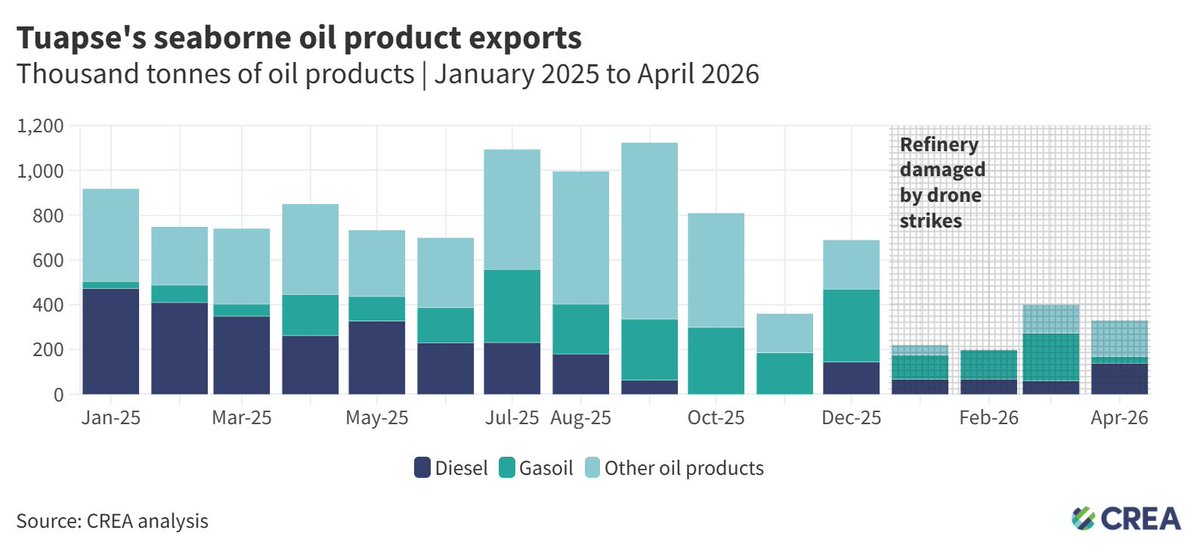

💥Repeated Ukrainian drone strikes on Rosneft’s Tuapse refinery drove a 65% year-on-year drop in Russian oil product exports in Jan–Apr 2026

🇷🇺 CREA’s April analysis on fossil fuel exports from Russia is now available here in EN & 🇺🇦 UA soon to follow:

➡️energyandcleanair.org/april-2026-mon…

Find all related CREA data here:

➡️ energyandcleanair.org/financing-puti…

➡️energyandcleanair.org/april-2026-mon…

Find all related CREA data here:

➡️ energyandcleanair.org/financing-puti…

• • •

Missing some Tweet in this thread? You can try to

force a refresh