Founder/CEO of Arkomina | Investor | Macroeconomist | Stock Picker | Not investment advice (see disclaimer) | https://t.co/RKwv0ZOS4v

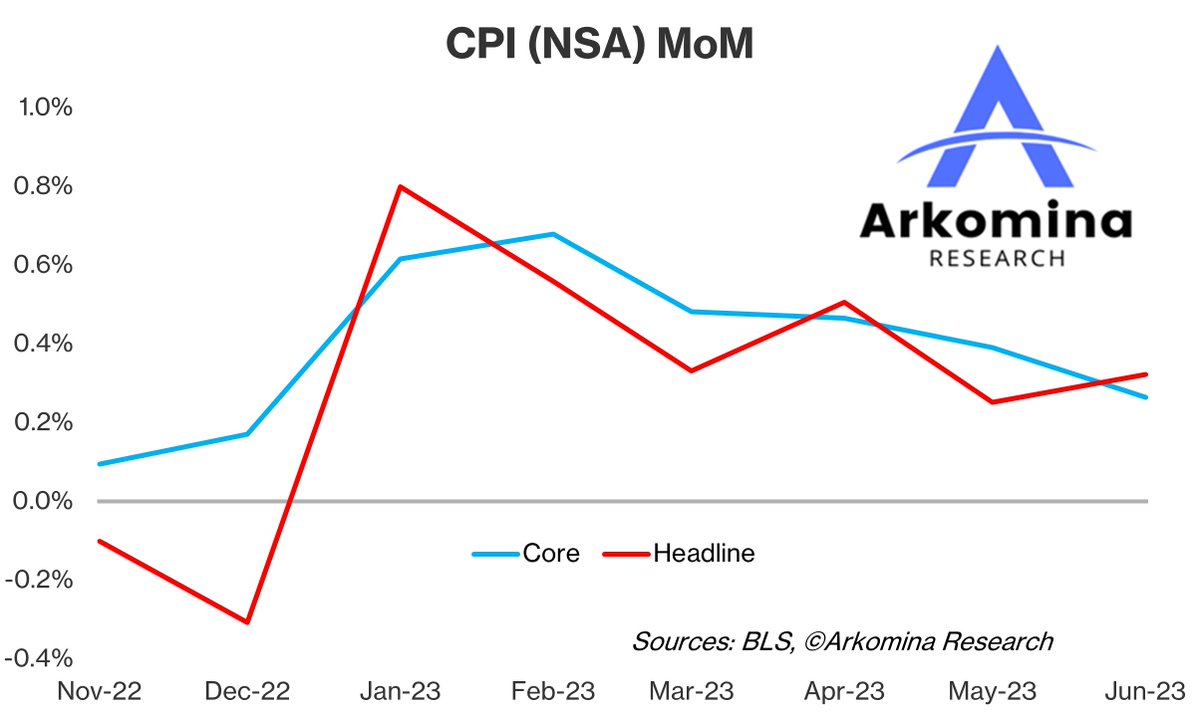

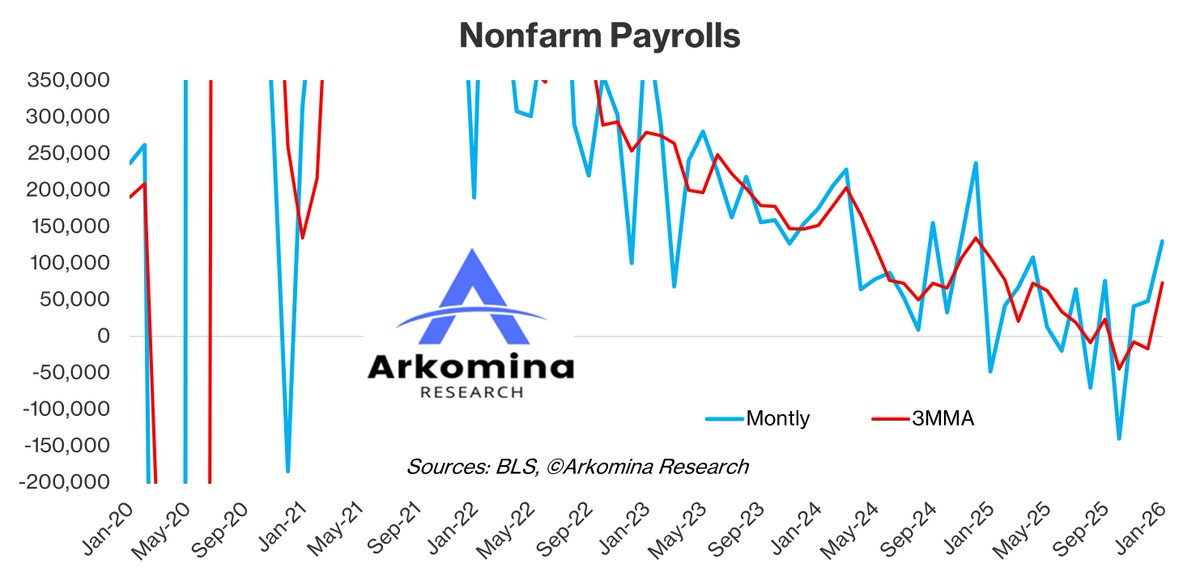

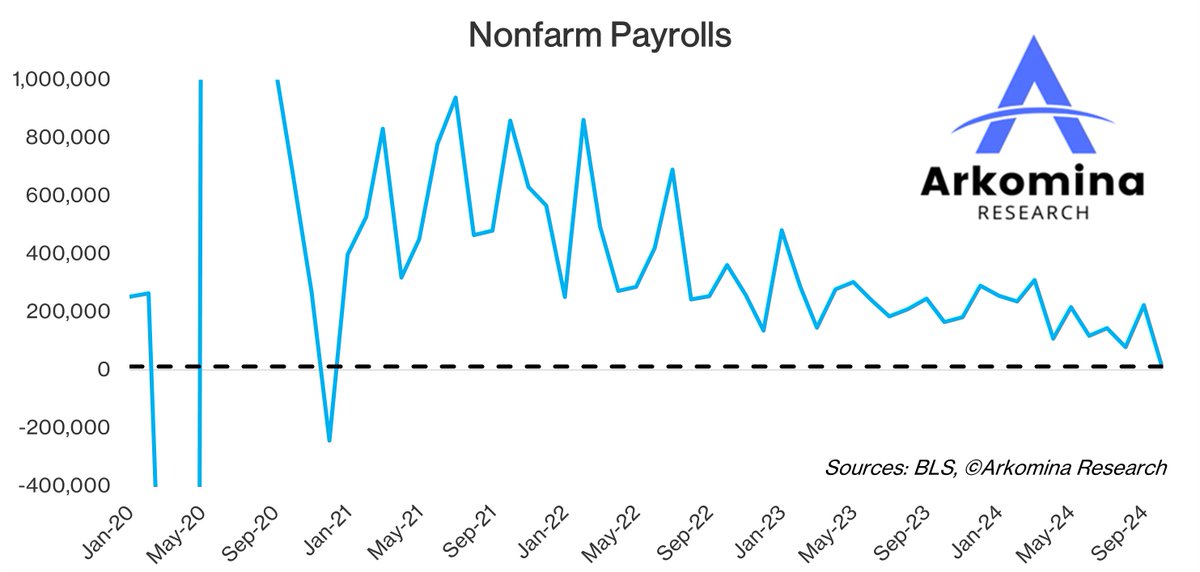

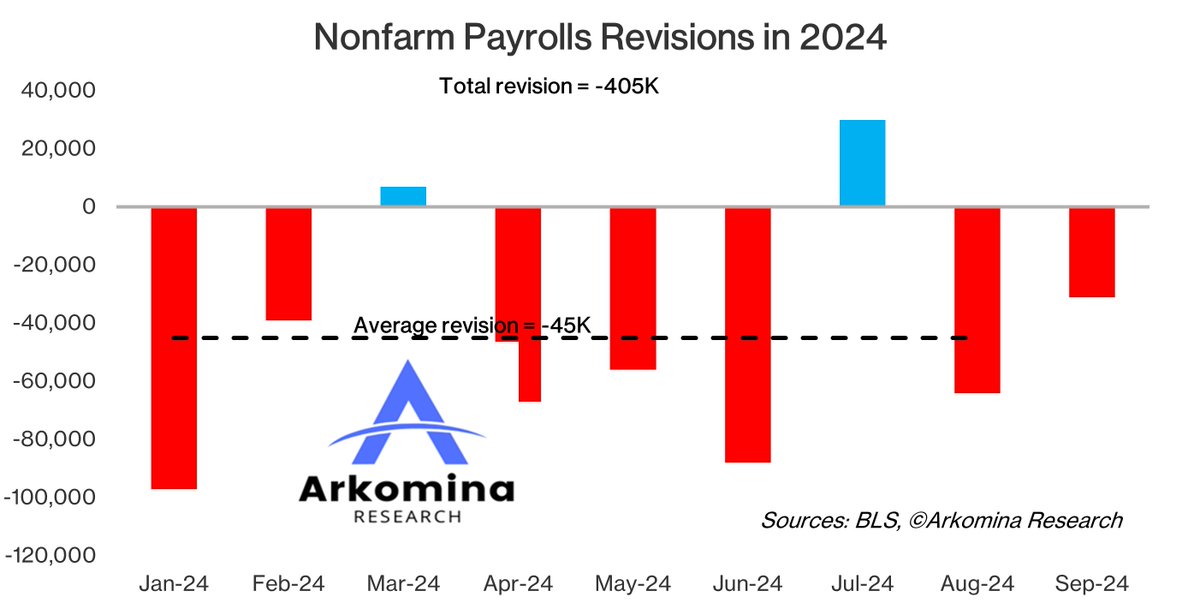

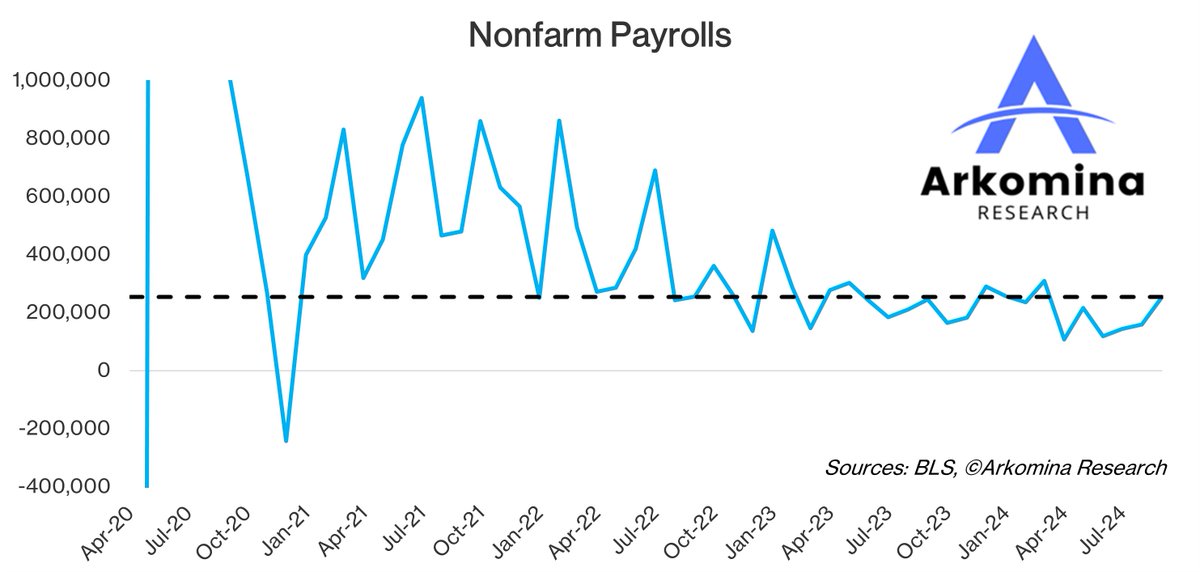

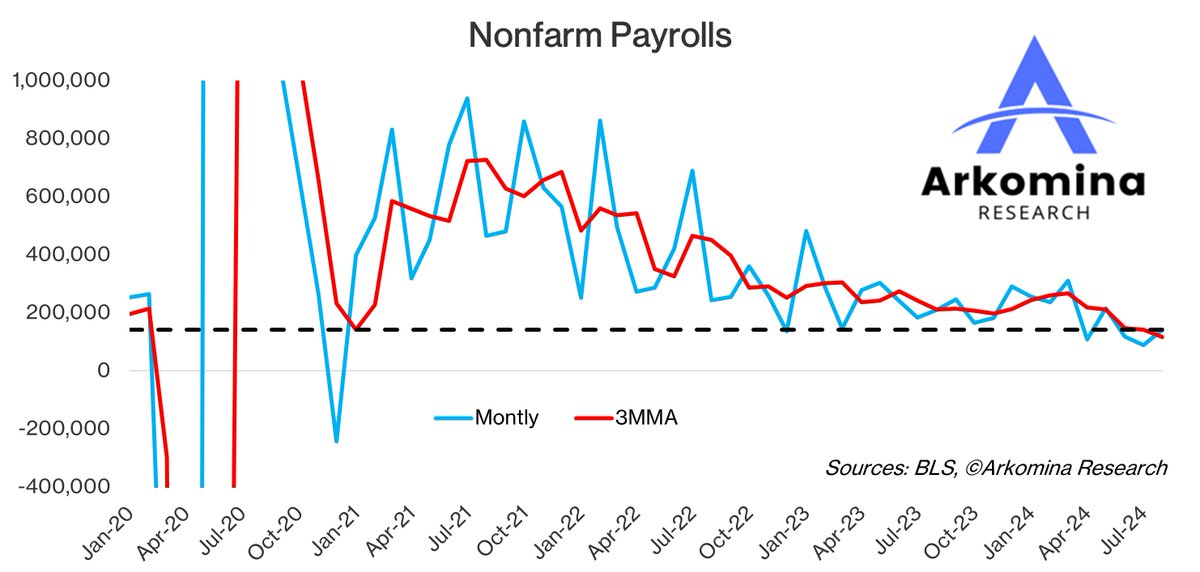

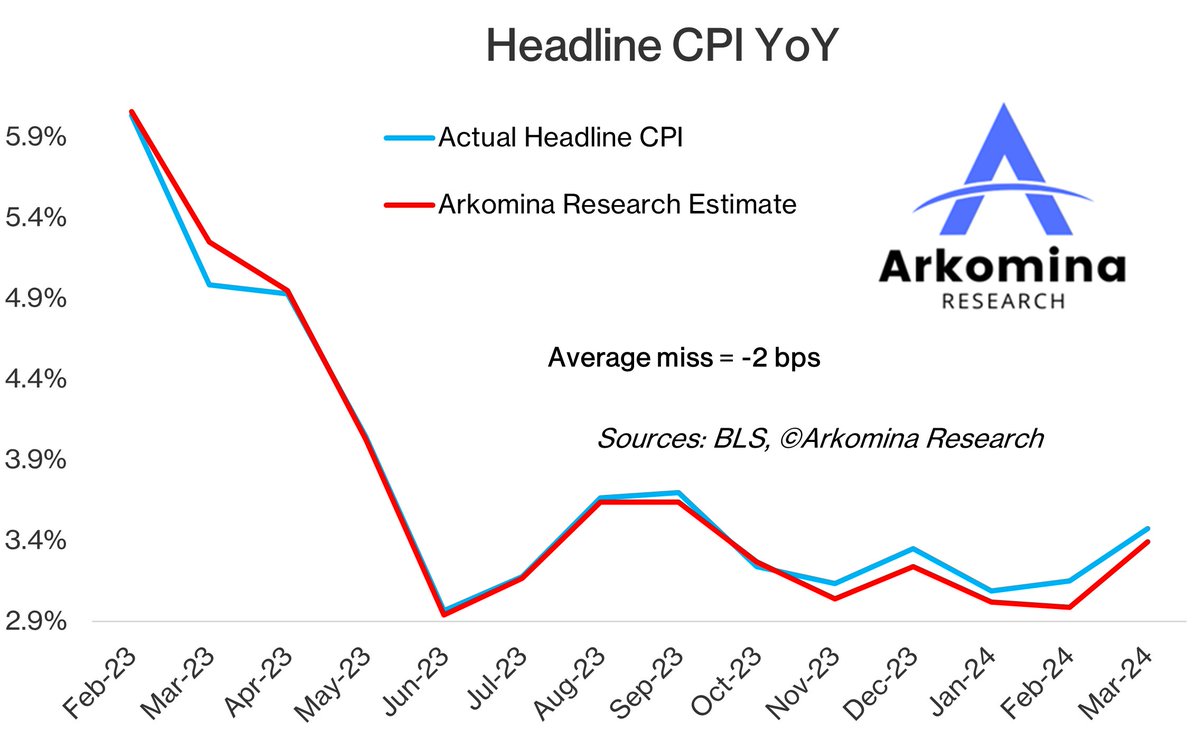

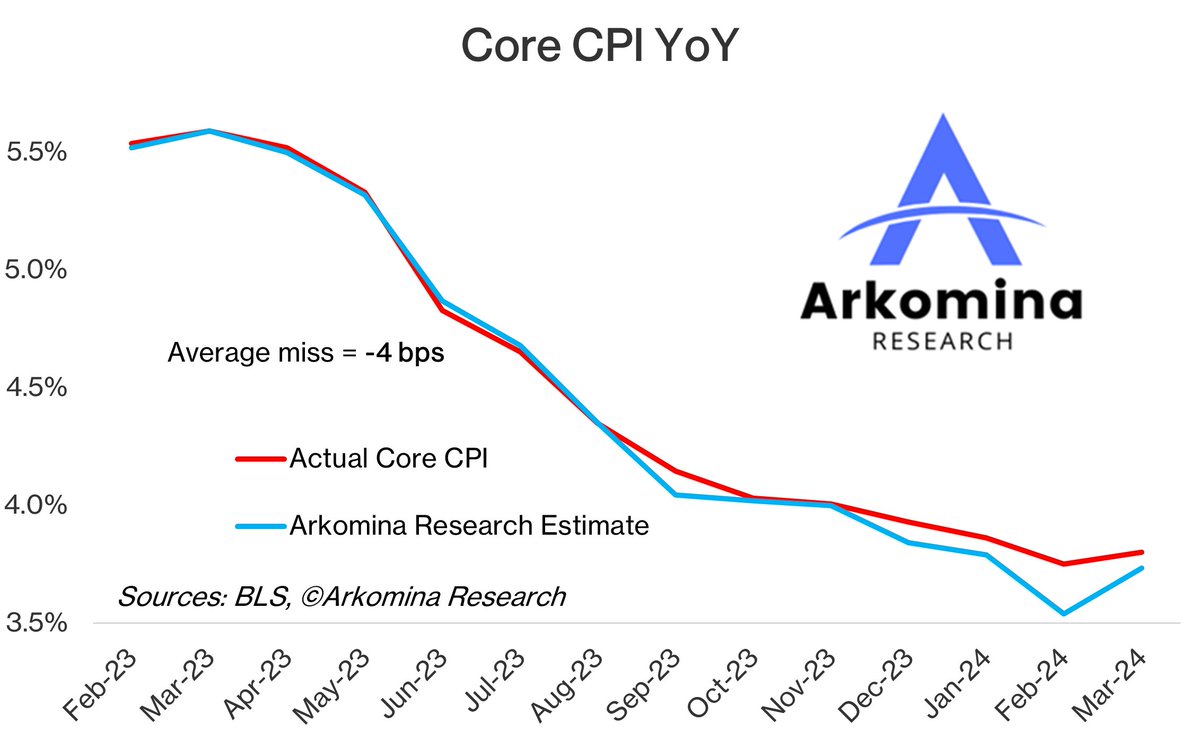

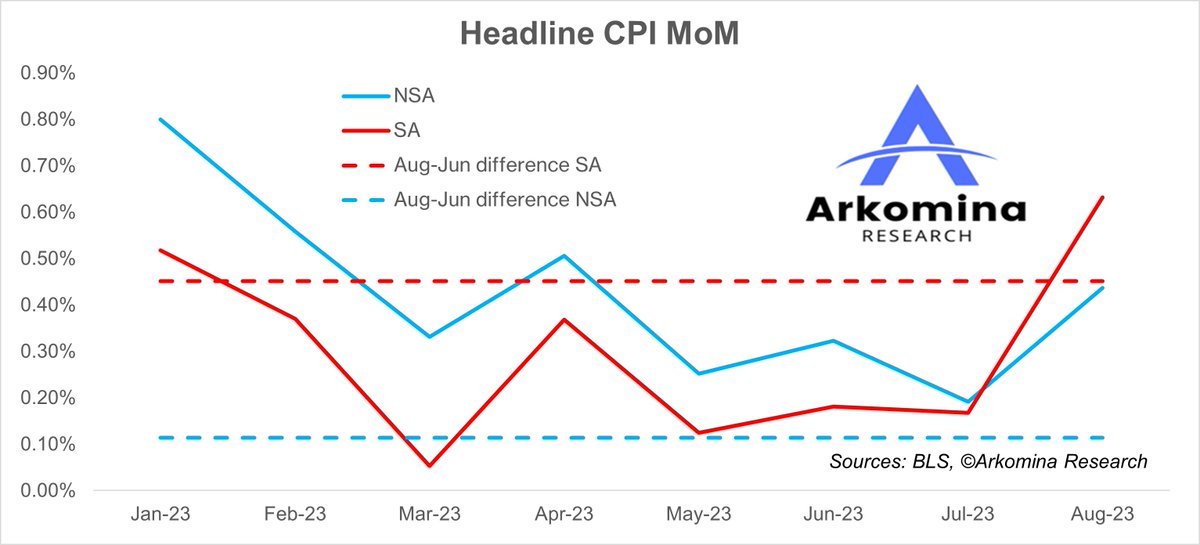

When the #Fed gets misled by inaccurate numbers like #JOLTS or lagging numbers like #CPI/#PCE one thing is certain - they will overdo it, no matter which direction they go.

When the #Fed gets misled by inaccurate numbers like #JOLTS or lagging numbers like #CPI/#PCE one thing is certain - they will overdo it, no matter which direction they go.