Shepherding illiquid assets by day, liquid assets by night. Personal views. 🇮🇳

Sep 15, 2021 • 14 tweets • 3 min read

1/ I want to discuss an often overlooked qualitative aspect in thesis building - which to my mind becomes significantly important if it involves crossing stages (ie small to mid cap, mid to large cap) or rapid growth situations 🧵…

2/ That aspect is CULTURE. This is not about fuzzy words on vision or values. What it means in the investing context is the first line of this tweet. (Will use CEO/promoter/mgmt interchangeably for the rest of this thread)

1/ <THREAD> Buying in a sell-off. My past mistakes in contra calls come down to 3 things (a) Believing the worst is over (b) buying too soon too quickly (c) Trying to max return while not minimizing risk. This is intended mostly for non-(professional/experienced) investors

2/ Sell-offs are complex because there are multiple things at play. There are (a) negative fundamentals, (b) short-sellers. In addition, multiple sharp negative moves indicate (c) unwinding of leverage. These sharp moves bring in the panic sellers. Will touch on all three

Nov 1, 2019 • 11 tweets • 2 min read

Given that I had publicly spoken about this, it’s only fair to disclose that I’ve closed this position this week. Some thoughts —>

1/ The initial thesis was based on a strong player emerging from a crisis. Both operators and tower cos had consolidated. Infratel had and still has the balance sheet to withstand a few challenging years

Oct 11, 2019 • 15 tweets • 5 min read

0/ A compilation of all (well most) #threads I have posted on #FinTwit in no particular order. I will keep adding new threads I post on this main thread and pin it to my profile. No reccos implied or otherwise. Share & discuss if you find it useful ...

1/ On investing mistakes, diligence findings and lessons ... this will be updated from time to time ...

Lots of optimists in this poll. It would be great if YB can get out of this mess. The key IMO would be to secure enough credible capital aka WB/GS in 2008. Both “enough” & “credible” being important /1

2/ If capital is required for provisions then the bank is already trading at a post-money valuation which means the real economic mcap is already lower by the amount required for provisions

Aug 10, 2019 • 7 tweets • 5 min read

1/ Thread on some interesting data and views from KKR’s global macro piece “Stick to the plan” available at kkr.com/global-perspec… Not comprehensive, just data points I liked shared.

2/ Globalisation is reversing, global trade is falling and being mixed with national security the world over. We are in unchartered territory. KKR expects a recession (I know it’s a topic beaten to death) in 2020

Aug 6, 2019 • 8 tweets • 3 min read

1/ So interestingly, a third of respondents don’t like real estate as a space. Though from a business model perspective I agree with the conclusion that bldg materials (BM) is the best way to play this because —>

2/ BM has renovation demand and ‘trading-up’ demand which takes away some of the cyclicality, has the ability to build distribution which if done right adds to the “moat” and lends itself to the optionality of being asset light

Jul 11, 2019 • 4 tweets • 1 min read

16/ D: I don’t use complex formulae to arrive at a discount rate. I test with a range of rates starting with co’s interest rate, always cross-checking what the implied multiples from B show.

17/ When the prevailing market multiple matches the implied multiple at disc rate=cost of cos debt, you are technically better off having a position in the cos debt rather than equity. But then markets don’t operate on formulae. It’s a signal nonetheless.

Jul 11, 2019 • 19 tweets • 4 min read

0/ I’ve had a love-hate relationships with DCFs. I swore by them, then promised I’d never use them and now use them selectively. I’ll talk about my experiences and how I use them now, in this thread —>

1/ Many years ago when valuing a thermal power plant I decided to use a 2 stage DCF. Higher discount rate for the riskier construction period and lower discount rate for the more stable operating period. Imagine my surprise when the resultant value was obnoxiously high!

Jun 12, 2019 • 11 tweets • 2 min read

1/ There has been a lot of interest of late in the #CapitalGoods space. Some observations in this thread

2/ Contrary to popular opinion that cap goods is a cyclical space there is a small subset of companies in this space which have delivered decent returns over decade plus time periods. Literally 5-10 odd cos

1/ Investors tend to think of investing as a formula (like physics) because its simpler to visualise: Good mgmt+good biz+industry tailwinds = good investment outcome. But business is like biology. There is evolution, mutation, reaction, reflexivity, etc which cannot be modeled

Apr 18, 2019 • 6 tweets • 1 min read

1/ High market share co having high valuation means you are betting more on (a) more usage per person (b) higher prices per unit (c) completely new biz to deliver for ensuing profit or cash flow growth to justify current multiple. #Colgate2/ Beyond a point getting incremental share becomes very tough. The market leader then has to develop the category to grow the market to increase usage. “Daag ache hain” campaign is probably the best example aka more usage

Apr 17, 2019 • 5 tweets • 1 min read

The Jet saga is a classic case why aviation is a bad industry for investment. Weak mgmt and bad capital allocators keep getting recapitalised. In the words of Terry Smith “It’s like being in a zombie movie. They keep coming back from the dead” /1

2/ The economics of free markets don’t seem to apply to aviation. Given its visibility, employability and historical govt ownership, they keep getting bailed out. Plus some elements of a lifestyle biz keeps bringing new entrants.

Mar 1, 2019 • 12 tweets • 2 min read

1/ THREAD — Understanding the millennial (born 1980+) and their spending patterns is going to be the toughest thing for public market investors. Simply because most investors today are either Gen X or Y

2/ I am one of the earlier millennials and while I can relate to the ‘80s cohort, it’s tough to understand the ‘90s crowd, forget the 2000s teens. I say this because as part of a teen/young adult mentoring initiative I am privy to the experiences of fellow mentors and my own exp

Feb 23, 2019 • 11 tweets • 2 min read

1/ THREAD on improving understanding of a business.

Usually the first step in fundamental investing. Over time I have found it useful to simplify the complex positioning of a biz into a few simple categories

2/ Most biz I know can be classified into one or more combinations of the following categories (pt3) Some simplified examples later in the thread to explain.

Disclaimer: This is limited to my understanding. It’s not perfect. It’s not a formula. May not work for you.

Jan 30, 2019 • 6 tweets • 1 min read

1/ A few thoughts on evaluating store / outlet based businesses. Most analysts value them on absolute earnings (ie corporate EBITDA, PAT) which mix SSSG and store expansion. Metrics like SSSG also don’t provide sufficient insight if store growth is high.

2/ I would rather value operational stores (min 65-70% value for today’s stores in market cap) + franchise value (~30% of market cap). % range will change depending on franchise quality

Nov 22, 2018 • 9 tweets • 2 min read

Promoter of decently successful SME on why we haven’t been able to realise our potential in manufacturing: “At heart most entrepreneurs in India still have a trading mentality.” He was obviously referring to peers in the SME space not large industrialists. (THREAD) /12/ Got me thinking. Connecting the dots from a recent book I read, almost all of India’s large industrial houses today started as traders, agents. Ploughing profits of trading to backward integrate in mfg.

Nov 2, 2018 • 7 tweets • 4 min read

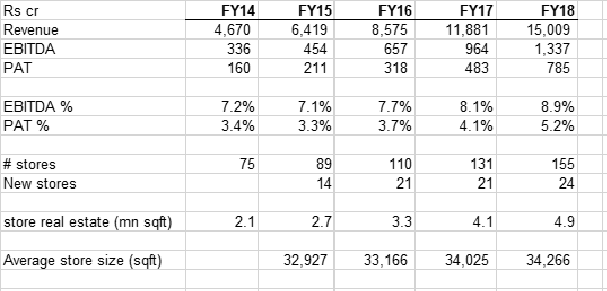

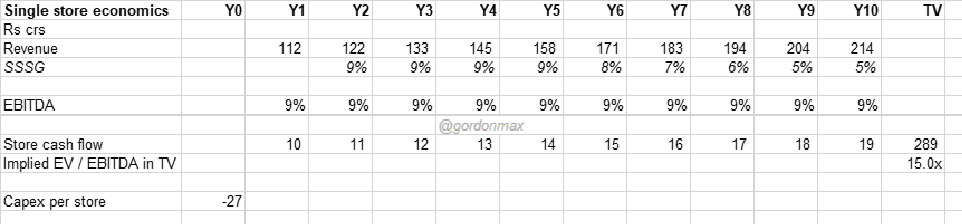

@prosperotree 1/ Let me attempt this with some rough calcs. METHOD 1: Below snapshot from company data except for avg store size which is calculated. Note that the revenue CAGR is driven by sqft growth. Why this is imp later in METHOD 2 @prosperotree 2/ With the avg store data I attempted to value a single store. Revenue is avg store sqft x Avg rev/sqft from tweet (1) – gives a FCF stream. Obviously many assumptions made

Oct 31, 2018 • 38 tweets • 5 min read

This is a thread of mistakes, diligence findings & lessons. Some personal, some professional. Will keep adding as I dig through memory. Hope it’s as useful to you as it was & is for me. No names. Context wherever possible #InvestingMistakes#DiligenceFindings#Lessons1/ What it takes to grow a company 100 cr in size is different to grow it to 500 cr is very diff for 1000 cr, v diff for 10k cr. Very few ppl have the skills to lead such cos. Hence very few small caps will make it to largecaps

Oct 27, 2018 • 7 tweets • 2 min read

Ever since Buffet has publicly made known ROE as his filter, many investors have been obsessed with finding and investing in high ROE companies. But blindly chasing high ROE may not be good for you. Here’s why... /12/ Mathematically, over a long holding period, shareholder return mirrors the ROE. This however makes foll assumptions (a) ROE is sustainable over very long periods ie 20+y (b) revenue growth >= ROE (c) business has no debt (d) surplus can be re-invested at ROE > current ROE

Oct 25, 2018 • 15 tweets • 4 min read

1/ We are in results season and there is a mad rush to attend concalls and be on top of every number published. But what value does this info provide? My views in this thread

2/ The vast majority of questions in concalls are clarifications, short term (ST) related (next Q, year end), tactical numbers (eg. what margin, growth rate, capex, etc). Some are even focused on abscure matters like depreciation!