We saw a modest 0.1% gain in headline #CPI this morning, a slightly firmer 0.2% gain in core CPI, yet already this report is a story of “that was then, and this is now,” since the #coronavirus and #oil price shock are altering the #economic landscape.

Fascinatingly, the decline in inflation #breakevens implies a world that simply doesn’t believe #inflation is rising, and based on market pricing, instead believes it is falling quickly toward not only short-term, but even longer-term, #disinflation.

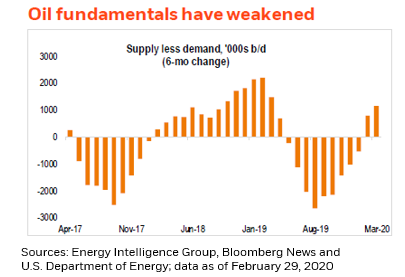

We think the disinflationary story told by #TIPS markets is probably overdone and note that even before the Saudi/Russian #oil production dispute, and before the coronavirus’ #economic impact, the fundamentals in the oil market were already displaying signs of deterioration.

As a result of all this, we think that the #Fed will probably cut #policy rates close to, if not to, zero over the next couple of meetings, yet this will have a limited influence on real #economic activity in a world where well-planned #FiscalPolicy is required.

• • •

Missing some Tweet in this thread? You can try to

force a refresh