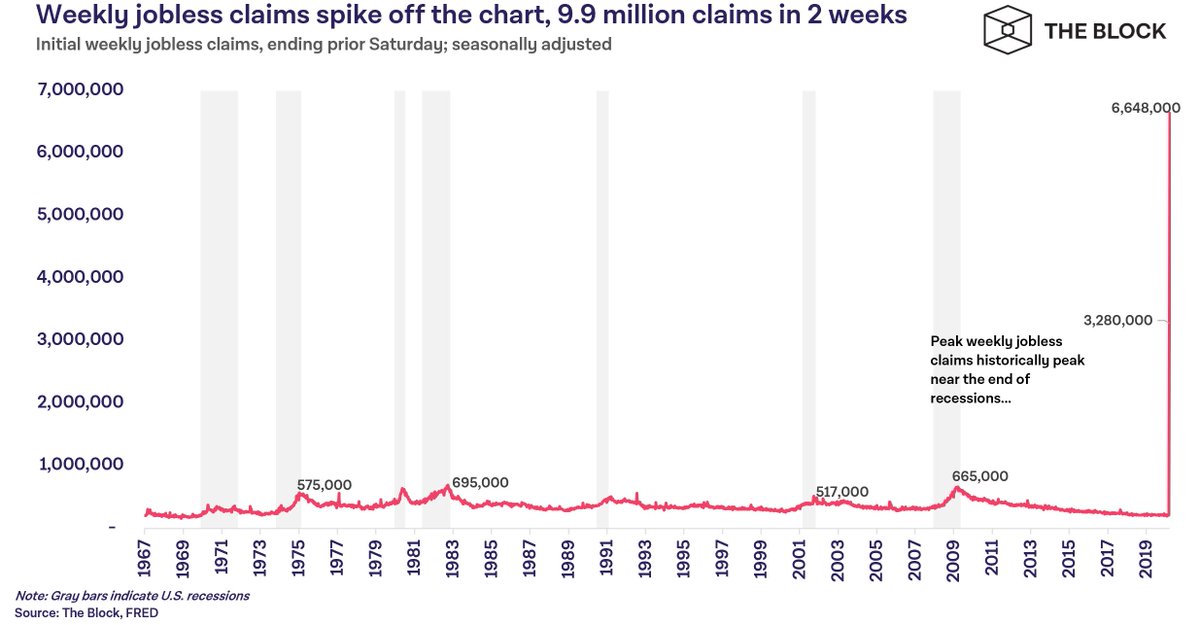

The major factor is unemployment. This excellent graph from @TheBlock__ shows the speed and magnitude of what #COVID19's slowdown is doing. 10 million unemployed in 2 weeks means a lot of folks will be stressed when it comes time to pay rent/mortgage.

It's unprecedented.

It's unprecedented.

To understand what's going on now I need to take you back a little first. Let's explore the past year.

In short, lenders have been stressed due to high demand, and lag times are hurting those waiting for their refinancing loans to close.

In short, lenders have been stressed due to high demand, and lag times are hurting those waiting for their refinancing loans to close.

As many of you know, refinancing often takes a while, typically ~60 days in the industry. My previous employer is famous for having a 30 day turn around (I bet you can guess who). But as of last summer processing departments have been slammed due to mortgage rates coming down.

This forced even faster lenders to adjust their closing times to 45 or 60 days. Bigger banks didn't stand a chance.

I remember hearing that Bank of American and Wells Fargo had mandatory 120 rate locks just because they couldn't keep up with demand.

It was a refi boom...

I remember hearing that Bank of American and Wells Fargo had mandatory 120 rate locks just because they couldn't keep up with demand.

It was a refi boom...

But what happens to all those people waiting to close their loans that just lost a job? With no income you can no longer qualify. The rug gets pulled out just when you need help the most.

My heart goes out to anyone in this scenario.

My heart goes out to anyone in this scenario.

This is a phenomena that will continue as layoffs ripple through the economy. If you refinance today, you cross your fingers that you can get to closing without losing your job.

Say it with me: Low rates mean nothing if you can't qualify for them!

Say it with me: Low rates mean nothing if you can't qualify for them!

As cash gets tight individuals' Debt to Income ratios (DTI) will soar and make them further ineligible for loans.

On FHA loans (least strict requirements) max DTI is between 40-50%.

Even if you managed to keep your job, if you go over 50% your loan is in trouble!

On FHA loans (least strict requirements) max DTI is between 40-50%.

Even if you managed to keep your job, if you go over 50% your loan is in trouble!

Cash is getting tight for a lot of folks now. $1200 in stimulus at the end of April is too little too late when rent was due 3 days ago. Do we have enough savings? The answer is emphatically no. 23% of us have no emergency savings at all.

So what do they do? They don't pay

So what do they do? They don't pay

Lenders are bracing for a spike in delinquencies, with some saying 15 million households could stop paying if lockdown extends through the summer.

Servicing companies need that liquidity to pay MBS investors. It could all come crashing down.

bloomberg.com/news/articles/…

Servicing companies need that liquidity to pay MBS investors. It could all come crashing down.

bloomberg.com/news/articles/…

So what are the options? Either people get pushed into foreclosure or they receive forbearance.

At this scale, foreclosures will tank the housing market, evaporating people's equity and making refinancing a nightmare for some time. The reason for that is due to LTV. More below

At this scale, foreclosures will tank the housing market, evaporating people's equity and making refinancing a nightmare for some time. The reason for that is due to LTV. More below

LTV, or Loan To Value is how much you owe vs the value of the home. Federal guidelines set limits for lenders based on different products.

For an FHA cash out refi you'll need at least 80% LTV, so if your home depreciates significantly you may no longer be access your equity.

For an FHA cash out refi you'll need at least 80% LTV, so if your home depreciates significantly you may no longer be access your equity.

Apply that across the whole housing market and you end up with some homeowners underwater (loan is worth more than the house), some who can't refi bc of LTV guidelines, and those who can't qualify because of DTI and revolving debt.

We know that mass foreclosures would grind the housing market down, so many federally backed loans are offering forbearance instead.

Borrowers with Gov backed loans can ask to skip payments for up to 180 days. Helps in a pinch, but it's kicking the can down the road.

Borrowers with Gov backed loans can ask to skip payments for up to 180 days. Helps in a pinch, but it's kicking the can down the road.

The question then remains, what happens if this #coronavirus slowdown has implications beyond 180 days? It strikes me that 10 million now unemployed and dislocated workers won't just jump back into a job when this is over.

The effects will be lasting, and thats worrying

The effects will be lasting, and thats worrying

My expectation given #Trump's administration's actions are that we see a liquidity injection to servicers and mortgage lenders to try and backstop the pain that will come from borrowers defaulting. We have already seen @federalreserve purchase MBS. That will likely continue

With stimulus and #UBI being en vogue we may also see direct loan forgiveness at the consumer level.

The trend toward universal government intervention in all markets continues.

The trend toward universal government intervention in all markets continues.

In sum, this massive spike in unemployment is seriously hampering homeowner's ability to refinance at low rates. Let's not forget, these are real people who are struggling and now can't access the cash in their homes. We should be sensitive to that.

Low rates aren't enough.

Low rates aren't enough.

Moving forward I think this will get very ugly for the #housingmarket. It remains to be seen what actions will be taken but I predict that the government will either directly or through the Fed bailout lenders or give consumers stimulus to help out. Stay safe.

End thread

End thread