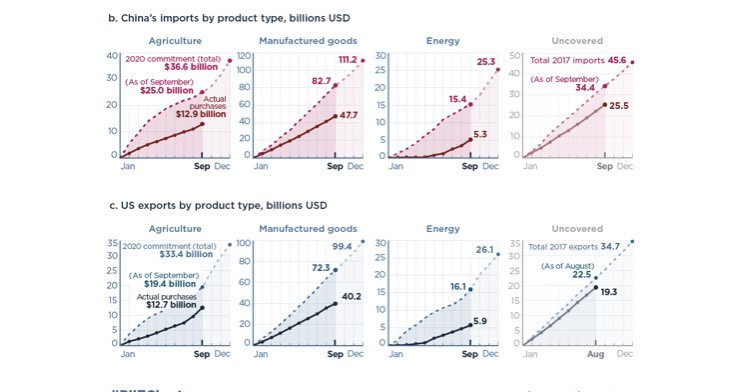

I am impressed @ChadBown

Seasonal adjustments are actually kind of important here (ag is the most important category ... and it is, umm, classically seasonal)

And, well, the interesting story in the September data is in the ag numbers

1/x

Seasonal adjustments are actually kind of important here (ag is the most important category ... and it is, umm, classically seasonal)

And, well, the interesting story in the September data is in the ag numbers

1/x

https://twitter.com/ChadBown/status/1320880364559212544

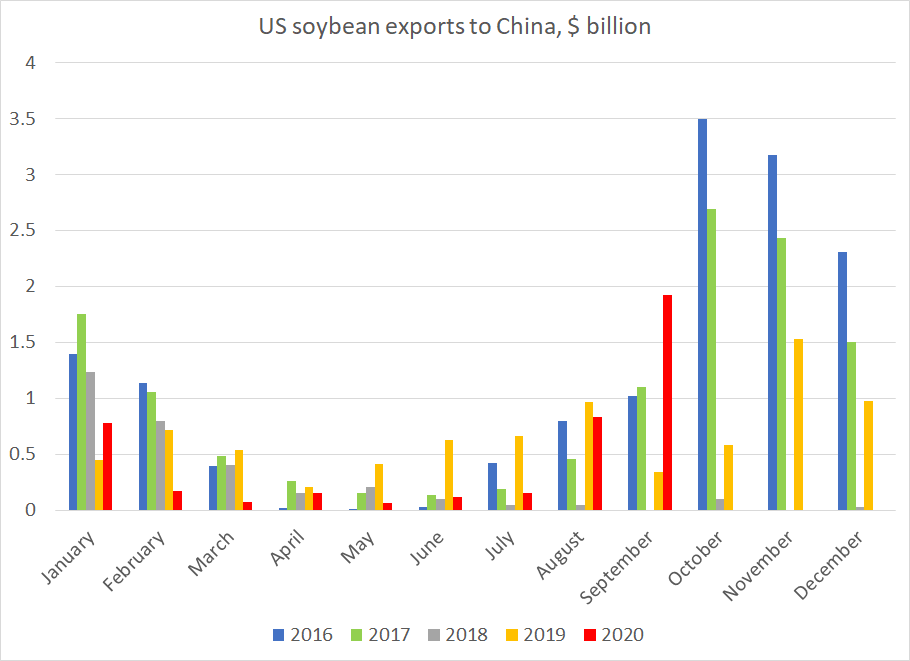

My (more modest) seasonal adjustment looks at the monthly data. The 'beans numbers were (as expected) solid. September basically made up for a weak start of the year. I hear the 'bean harvest came in early, and supplies in Brazil are by all accounts tight

2/x

2/x

Bean exports should top the 2017 base given the orders data USTR highlighted and current bean prices. Topping 2016 may be harder ...

(But don't forget 2018 -- the empty bar there isn't an accident; China showed that its state import companies control the market)

3/x

(But don't forget 2018 -- the empty bar there isn't an accident; China showed that its state import companies control the market)

3/x

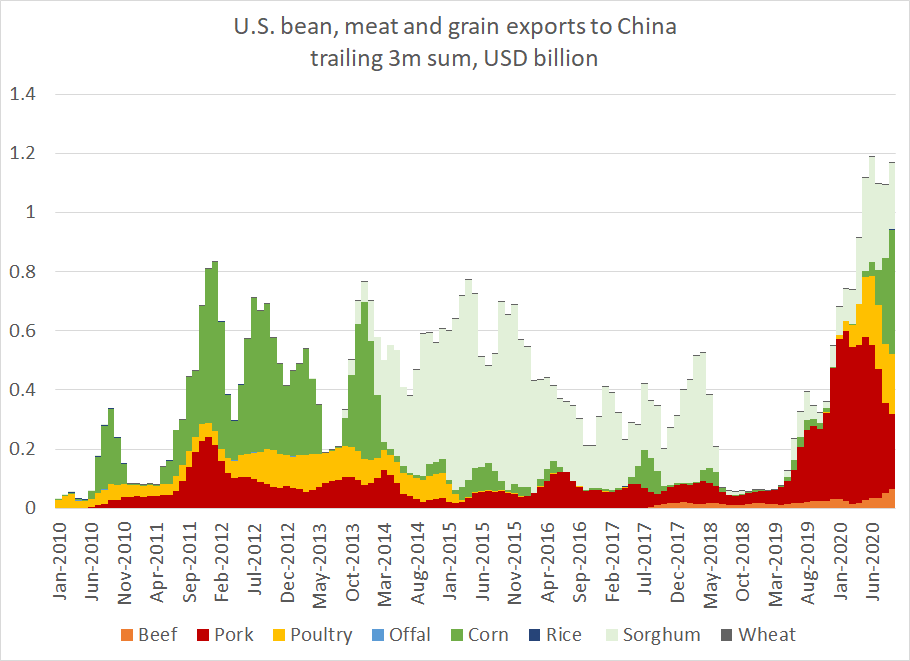

Pork tho is almost equally interesting. US exports are back at their 2019 levels --

And it is sort of obvious if you look as the data that the surge in pork exports actually preceded the phase one deal (it has everything to do with swine fever)

4/x

And it is sort of obvious if you look as the data that the surge in pork exports actually preceded the phase one deal (it has everything to do with swine fever)

4/x

And don't forget that in a deep sense US pork and soybean exports to China will tend to trade off (Chinese pigs are fed imported 'beans)

5/x

5/x

2020 ag exports to China are actually following a fairly standard seasonal pattern (Monthly soybean exports usually pick up in Sept, peak in October and then start to trail off -- the trailing 3m sum peaks in December).

Notable tho b/c neither 2018 or 2019 was normal

6/x

Notable tho b/c neither 2018 or 2019 was normal

6/x

The previous chart captures the sheer scale of US bean exports to China -- nothing really compares.

Here is a closeup of the smaller line items. Pork is trailing off, chicken paws are back, corn and sorghum are doing well but nothing wildly out of the pre trade war norm

7/x

Here is a closeup of the smaller line items. Pork is trailing off, chicken paws are back, corn and sorghum are doing well but nothing wildly out of the pre trade war norm

7/x

Full disclosure: my extended family farms corn and beans. That's me, on a grain bin

(and I obviously support Biden, though the charts should be politically neutral)

(and I obviously support Biden, though the charts should be politically neutral)

• • •

Missing some Tweet in this thread? You can try to

force a refresh