The New York Times (@petersgoodman) highlights how the global financial response to the pandemic, to date, has fallen short of providing the financial support low income countries need to cope effectively with the shock

1/x

nytimes.com/2020/11/01/bus…

1/x

nytimes.com/2020/11/01/bus…

Deferring debts owed to bilateral creditors was always going to only be a small part of the solution, but especially if China deemed key institutions like the CDB to be "private."

It was thus a mistake to make the DSSI the central mechanism for providing pandemic support

2/x

It was thus a mistake to make the DSSI the central mechanism for providing pandemic support

2/x

Only about $5b of the $30b in non-MDB debt coming due in 2020 will be rescheduled; the initiative has failed even on its own terms.

And since debt burdens aren't uniformly distributed, even a broad DSSI limited to bilateral creditors would not have provided enough to most

3/x

And since debt burdens aren't uniformly distributed, even a broad DSSI limited to bilateral creditors would not have provided enough to most

3/x

That is one of the points @AGelpern and I tried to make in the Group of Thirty report --

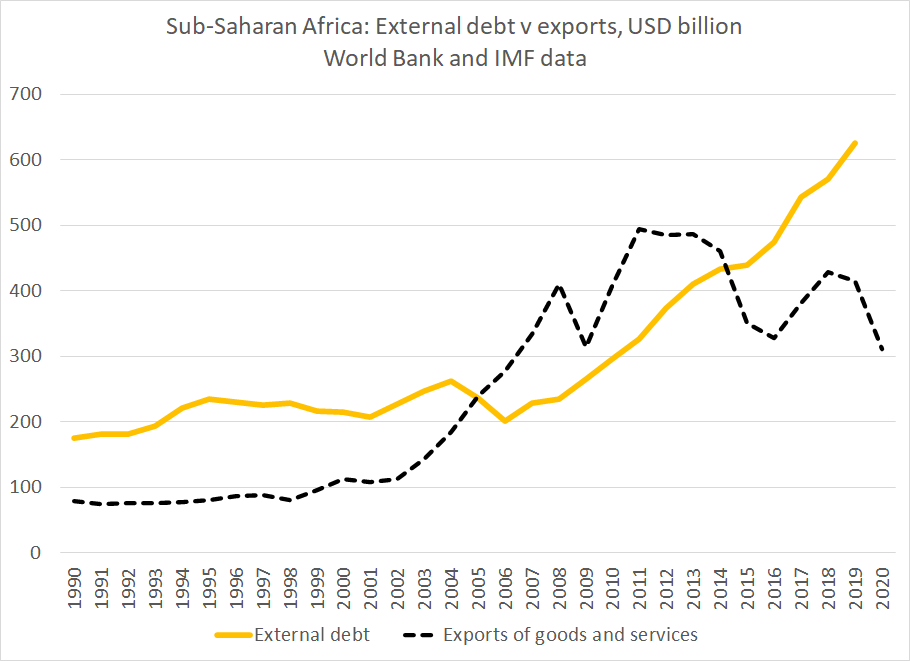

Debt burdens aren't uniform, and in many of the cases where the debt burden is high (Zambia, Angola, Laos etc) much of the debt isn't public debt owned to official bilateral creditors

4/x

Debt burdens aren't uniform, and in many of the cases where the debt burden is high (Zambia, Angola, Laos etc) much of the debt isn't public debt owned to official bilateral creditors

4/x

As Peter Goodman notes, the World Bank didn't combine its (welcome) emphasis on scaling back debt service (even if relief was always needed for more than a couple of years) with a push to use its own balance sheet aggressively to support its members

5/x

5/x

The IMF in a sense did better -- it did get a lot of concessional loans (RCFs) out the door, but that pool of funds is limited. It you measure the IMF's response by actual disbursements rather than commitments, it is still modest relative to the shock

6/x

6/x

The $100b number Goodman cites includes commitments and the large (undisbursed) flexible credit lines provided to Peru and Chile. Actual disbursements are still more like $40b (they should rise with Colombia's decision to tap its FCL)

7/x

7/x

And the US blocked a broad SDR allocation to increase global reserves. As the Group of Thirty report notes, the world's existing tools have been used as aggressively as they could have been to help low income countries, amid a massive shock

8/8

prweb.com/releases/g30_c…

8/8

prweb.com/releases/g30_c…

• • •

Missing some Tweet in this thread? You can try to

force a refresh