On Valuing Banks

Approximate MCAP/Deposits (adj. for subs):

AUBANK: 98%

Kotak: 90%

HDFC: 58%

ICICI: 30%

IndusInd: 28%

IDFCFIRST: 28%

Axis: 25%

RBL: 19%

Federal: 7%

SBI: 6%

1/

Approximate MCAP/Deposits (adj. for subs):

AUBANK: 98%

Kotak: 90%

HDFC: 58%

ICICI: 30%

IndusInd: 28%

IDFCFIRST: 28%

Axis: 25%

RBL: 19%

Federal: 7%

SBI: 6%

1/

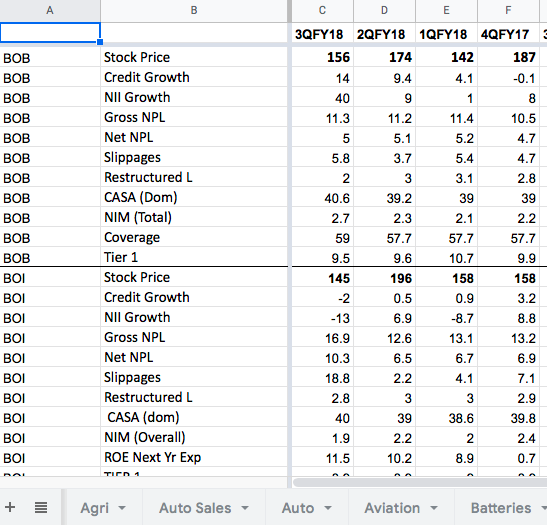

For banks first assess the strength of the liability franchise. Not just CASA ratio but total deposits to total liabilities.

A bank can have a low deposit share in liabilities and a high CASA.

Wholesale funding is not good.

Granular deposits are good.

2/

A bank can have a low deposit share in liabilities and a high CASA.

Wholesale funding is not good.

Granular deposits are good.

2/

Liability side determines the cost of funds. Lower your cost of fund the lower risk you need to take in lending for the same NIMs (profitability).

Some banks can’t even compete in prime Housing Loans (one of the safest segments) due to high cost of funds.

3/

Some banks can’t even compete in prime Housing Loans (one of the safest segments) due to high cost of funds.

3/

For most businesses growth is an output of your strategy and quality of service/product.

In lending growth is an input. You decide it (after all you are giving money).

The output is credit cost. That is quality of your underwriting.

4/

In lending growth is an input. You decide it (after all you are giving money).

The output is credit cost. That is quality of your underwriting.

4/

In general be wary of anything showing very high credit growth. That’s the easy part.

Historical underwriting performance is only indicative. Look at what segments the banks is lending to.

Secured/MSME/Salaried/BB & below etc.

5/

Historical underwriting performance is only indicative. Look at what segments the banks is lending to.

Secured/MSME/Salaried/BB & below etc.

5/

Loan customers who are also have a liability relationship are usually better.

Asses how frequently the bank will to dilute.

There is reflexivity here. A bank that can dilute at 4X will increase BV per share. One that has to do it at 0.3 will impair it.

6/

Asses how frequently the bank will to dilute.

There is reflexivity here. A bank that can dilute at 4X will increase BV per share. One that has to do it at 0.3 will impair it.

6/

Also what according to you are the strongest franchises today?

Would your view have been different 10 years ago?

How many BFSI names have beaten these over that period?

How much capital could you have allocated to these few vs the established franchises?

Think.

7/

Would your view have been different 10 years ago?

How many BFSI names have beaten these over that period?

How much capital could you have allocated to these few vs the established franchises?

Think.

7/

I don’t hunt for the next X. I buy the damn X.

8/

8/

Now people will say this bank will be able to follow a certain template (because of new CEO, new strategy etc) and the X valuation will become Y. Hence just buy it.

Don’t.

Businesses & Valuations are more nuanced.

Compare to existing ideas. Assess the opportunity cost.

9/

Don’t.

Businesses & Valuations are more nuanced.

Compare to existing ideas. Assess the opportunity cost.

9/

If you ever have to resort to high growth argument in BFSI you are probably heading for a trap.

Dis: Inv/Biased

10/10

Dis: Inv/Biased

10/10

• • •

Missing some Tweet in this thread? You can try to

force a refresh