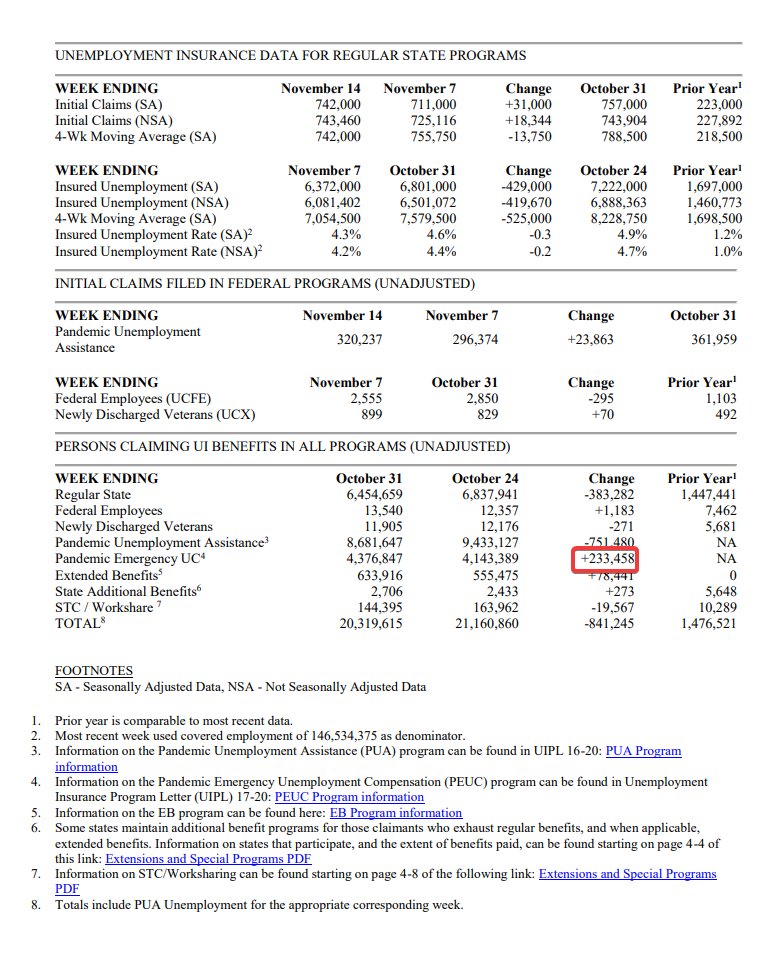

Initial claims rise modestly week over week, were ~1.1 million last week.

The recent declines in regular UI recipients, properly including the extended PEUC and EB programs, may be slowing.

And to punctuate that point: ~230,000 workers looked like they left regular state UI at the end of October, but actually just exhausted their regular benefits and transferred to the federal extended PEUC program.

Read this excellent piece from @pelhamprog and @ENPancotti to learn more about what it means if these extended programs expire as scheduled at the end of December. tcf.org/content/report…

• • •

Missing some Tweet in this thread? You can try to

force a refresh