1/

Get a cup of coffee.

In this thread, I'll share with you my thoughts on *investing* vs *speculation* -- and how to tell them apart.

Get a cup of coffee.

In this thread, I'll share with you my thoughts on *investing* vs *speculation* -- and how to tell them apart.

2/

In 1949, Ben Graham published his book -- The Intelligent Investor.

Warren Buffett, who was once Graham's student at Columbia Business School, has called this "the best book about investing ever written".

In 1949, Ben Graham published his book -- The Intelligent Investor.

Warren Buffett, who was once Graham's student at Columbia Business School, has called this "the best book about investing ever written".

3/

The very first chapter of the book is titled "Investment vs Speculation".

Clearly, Graham considered *investing* to be very different from *speculation*. And right at the outset, he wanted to educate the reader about the differences between the two.

The very first chapter of the book is titled "Investment vs Speculation".

Clearly, Graham considered *investing* to be very different from *speculation*. And right at the outset, he wanted to educate the reader about the differences between the two.

4/

Graham goes on to define investing and speculation like this:

"An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative."

Graham goes on to define investing and speculation like this:

"An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative."

5/

So Graham is saying -- if you "thoroughly analyze" a company (presumably, its financials, earnings, cash flows, etc.), and then buy the stock based on your analysis, you're "investing".

And if you buy the stock without doing such an analysis, you're "speculating".

So Graham is saying -- if you "thoroughly analyze" a company (presumably, its financials, earnings, cash flows, etc.), and then buy the stock based on your analysis, you're "investing".

And if you buy the stock without doing such an analysis, you're "speculating".

6/

Clearly, it's important to tell apart investing from speculation.

After all, when we commit thousands of dollars, we'd like to know if we're making a well reasoned, well thought out move (ie, an *investment*), or if we're just gambling with our money (ie, a *speculation*).

Clearly, it's important to tell apart investing from speculation.

After all, when we commit thousands of dollars, we'd like to know if we're making a well reasoned, well thought out move (ie, an *investment*), or if we're just gambling with our money (ie, a *speculation*).

7/

But is Graham's "thorough analysis" test a good way to distinguish between the two?

To be honest, I have mixed feelings about this.

But is Graham's "thorough analysis" test a good way to distinguish between the two?

To be honest, I have mixed feelings about this.

8/

On the plus side, Graham's test correctly identifies *some* moves as pure speculation.

For example, suppose we buy a stock just because it's been going up lately, or because a friend recommended it, or because someone on CNBC said nice things about the company.

On the plus side, Graham's test correctly identifies *some* moves as pure speculation.

For example, suppose we buy a stock just because it's been going up lately, or because a friend recommended it, or because someone on CNBC said nice things about the company.

9/

In all these cases, there's barely *any* analysis, let alone a *thorough* one.

So the test has no problem concluding (rightly so!) that we're just speculating.

In all these cases, there's barely *any* analysis, let alone a *thorough* one.

So the test has no problem concluding (rightly so!) that we're just speculating.

10/

On the other hand, suppose we diligently save 25% of our paycheck every year -- for 30 years.

At the end of each pay period, suppose we simply put our savings into a low-cost S&P 500 index fund -- dollar cost averaging into the fund irrespective of what it's trading at.

On the other hand, suppose we diligently save 25% of our paycheck every year -- for 30 years.

At the end of each pay period, suppose we simply put our savings into a low-cost S&P 500 index fund -- dollar cost averaging into the fund irrespective of what it's trading at.

11/

Should our behavior be considered investing or speculation?

We're not doing any thorough analysis. We probably don't know much about most companies in the S&P 500.

So Graham's test would label our behavior *speculation*.

But I think it's reasonable to call it *investing*.

Should our behavior be considered investing or speculation?

We're not doing any thorough analysis. We probably don't know much about most companies in the S&P 500.

So Graham's test would label our behavior *speculation*.

But I think it's reasonable to call it *investing*.

12/

Also, there's no such thing as a *risk free* investment.

Whenever we use our capital to buy an asset (a stock, a farm, a private business, a piece of real estate, etc.), there's always a chance that we'll lose money.

Also, there's no such thing as a *risk free* investment.

Whenever we use our capital to buy an asset (a stock, a farm, a private business, a piece of real estate, etc.), there's always a chance that we'll lose money.

13/

Chance events and luck play a big role in deciding what returns we get.

Investing, then, is the art of estimating probabilities and betting on favorable odds.

Odds? Betting?

Man, this sounds an awful lot like "speculation".

Chance events and luck play a big role in deciding what returns we get.

Investing, then, is the art of estimating probabilities and betting on favorable odds.

Odds? Betting?

Man, this sounds an awful lot like "speculation".

14/

It's true. Every time we buy a stock, we're *betting* on the future.

We're betting that competition won't destroy the company.

That new technology won't suddenly make the company obsolete.

That there's no accounting fraud going on.

It's true. Every time we buy a stock, we're *betting* on the future.

We're betting that competition won't destroy the company.

That new technology won't suddenly make the company obsolete.

That there's no accounting fraud going on.

15/

So, if most/all investing involves betting on the future, how do we draw a meaningful distinction between investing and speculation?

I have 3 recommendations:

1) Non-binary thinking,

2) Fundamental (rather than market) focus, and

3) Diversification.

So, if most/all investing involves betting on the future, how do we draw a meaningful distinction between investing and speculation?

I have 3 recommendations:

1) Non-binary thinking,

2) Fundamental (rather than market) focus, and

3) Diversification.

16/

First, non-binary thinking.

I believe most capital allocation decisions are neither pure investment nor pure speculation.

It's not black or white. There's a spectrum. Most decisions correspond to some shade of grey.

First, non-binary thinking.

I believe most capital allocation decisions are neither pure investment nor pure speculation.

It's not black or white. There's a spectrum. Most decisions correspond to some shade of grey.

17/

For example, if we're betting on only a few things to go right, and the odds of this are reasonably high, that's near the *investing* end of the spectrum.

But if we're betting on a chain of low-likelihood events to occur, that may be closer to the *speculation* end.

For example, if we're betting on only a few things to go right, and the odds of this are reasonably high, that's near the *investing* end of the spectrum.

But if we're betting on a chain of low-likelihood events to occur, that may be closer to the *speculation* end.

18/

Second, I recommend cultivating a *fundamental* focus rather than a market-driven one.

This means focusing our analysis on the *future cash flows* that we're likely to receive from an investment, rather than *what the market will pay* for those future cash flows.

Second, I recommend cultivating a *fundamental* focus rather than a market-driven one.

This means focusing our analysis on the *future cash flows* that we're likely to receive from an investment, rather than *what the market will pay* for those future cash flows.

19/

A good way to "think fundamentally" is to ask ourselves:

Suppose the market were to close -- and never reopen -- the day after we buy our investment.

Would we still be happy making the purchase?

(h/t @dhaval_kotecha, @KermitCapital, @StockDtective)

A good way to "think fundamentally" is to ask ourselves:

Suppose the market were to close -- and never reopen -- the day after we buy our investment.

Would we still be happy making the purchase?

(h/t @dhaval_kotecha, @KermitCapital, @StockDtective)

20/

That is, is there a reasonably high probability that the dividends we receive over time from the investment -- after taxes and adjusted for inflation -- will more than cover the price we paid for it?

If the answer is yes, then we're near the investing end of the spectrum.

That is, is there a reasonably high probability that the dividends we receive over time from the investment -- after taxes and adjusted for inflation -- will more than cover the price we paid for it?

If the answer is yes, then we're near the investing end of the spectrum.

21/

What this means is -- we're thinking like long-term owners.

We don't need *the market* to value our investment more highly tomorrow than today.

Whatever the market thinks, *we* are comfortable owning the investment -- and pocketing the dividends from it -- *forever*.

What this means is -- we're thinking like long-term owners.

We don't need *the market* to value our investment more highly tomorrow than today.

Whatever the market thinks, *we* are comfortable owning the investment -- and pocketing the dividends from it -- *forever*.

22/

When Buffett acquires a business for Berkshire -- like See's Candies or BNSF -- he pretty much commits *never* to sell.

So, it's irrelevant what the market will pay for the business in the future.

When Buffett acquires a business for Berkshire -- like See's Candies or BNSF -- he pretty much commits *never* to sell.

So, it's irrelevant what the market will pay for the business in the future.

23/

The decision to purchase the business, therefore, depends on *only* 2 factors: 1) the purchase price, and 2) the future cash flows that the business will deliver to Berkshire.

This is *fundamental thinking* at its finest -- very close to the investing end of the spectrum.

The decision to purchase the business, therefore, depends on *only* 2 factors: 1) the purchase price, and 2) the future cash flows that the business will deliver to Berkshire.

This is *fundamental thinking* at its finest -- very close to the investing end of the spectrum.

24/

In Buffett's 2013 letter, he beautifully describes this kind of fundamental thinking using 2 non-stock investing examples from his own life -- a farm in Omaha and an apartment complex in New York.

Link: berkshirehathaway.com/letters/2013lt…

Pics:

In Buffett's 2013 letter, he beautifully describes this kind of fundamental thinking using 2 non-stock investing examples from his own life -- a farm in Omaha and an apartment complex in New York.

Link: berkshirehathaway.com/letters/2013lt…

Pics:

25/

Of course, the market can be capricious. And we may take advantage.

But *counting* on this takes us near the speculation end.

Betting only on the fundamentals (earnings, cash flows, and dividends) keeps us near the investing end.

Pic (h/t @BrianFeroldi):

Of course, the market can be capricious. And we may take advantage.

But *counting* on this takes us near the speculation end.

Betting only on the fundamentals (earnings, cash flows, and dividends) keeps us near the investing end.

Pic (h/t @BrianFeroldi):

26/

Third (and last):

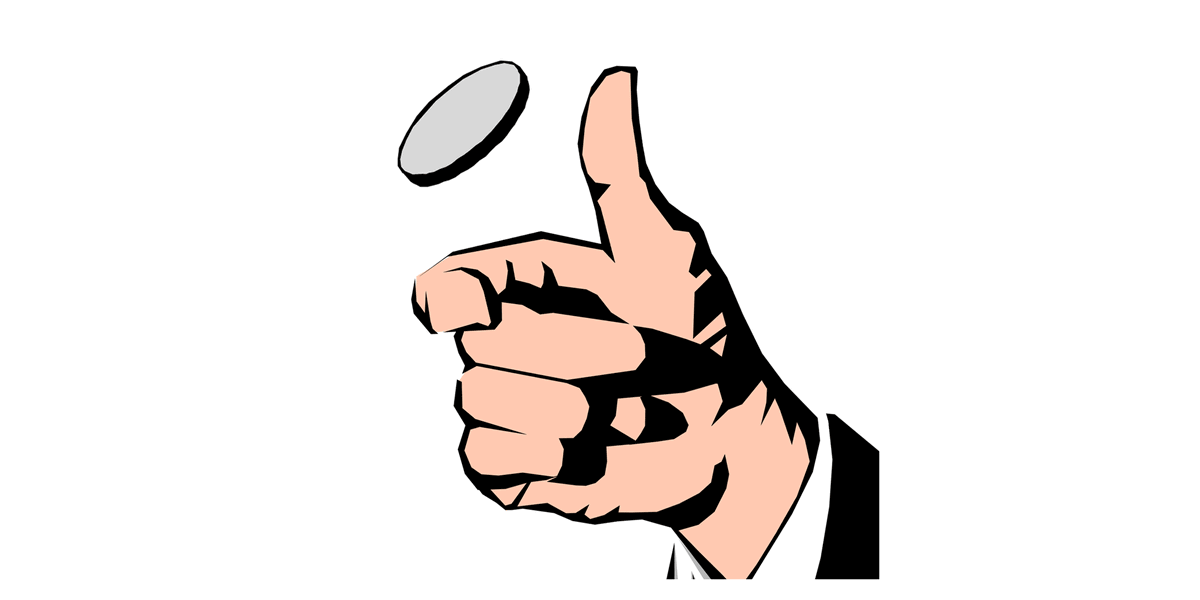

Sometimes, diversification can mark the difference between investing and speculation.

For example, suppose a coin has a 99% chance of turning up heads, and a 1% chance of tails.

Third (and last):

Sometimes, diversification can mark the difference between investing and speculation.

For example, suppose a coin has a 99% chance of turning up heads, and a 1% chance of tails.

27/

You can bet on each toss. You double your money if you're right and lose it if you're wrong.

If you bet *all* your money on heads, you're speculating.

Because imagine doing this repeatedly. Eventually, you *will* get a tails and lose everything.

You can bet on each toss. You double your money if you're right and lose it if you're wrong.

If you bet *all* your money on heads, you're speculating.

Because imagine doing this repeatedly. Eventually, you *will* get a tails and lose everything.

28/

But if you bet only 98% of your money on heads, you suddenly get close to the investing end.

Why? Because, at these odds, diversifying just a little bit between "cash" and "coin toss" increases the probability of compounding from 0 to 1.

For more:

But if you bet only 98% of your money on heads, you suddenly get close to the investing end.

Why? Because, at these odds, diversifying just a little bit between "cash" and "coin toss" increases the probability of compounding from 0 to 1.

For more:

https://twitter.com/10kdiver/status/1264622958468726785

29/

I think this is why dollar cost averaging over a long time into a diversified low-cost index fund (like the S&P 500) should count as investing and not speculation -- unless stock prices get really crazy.

I think this is why dollar cost averaging over a long time into a diversified low-cost index fund (like the S&P 500) should count as investing and not speculation -- unless stock prices get really crazy.

30/

Each individual bet may be near the *speculation* end of the spectrum.

But aggregate ~500 of them, and you may get close to the *investing* end.

Each individual bet may be near the *speculation* end of the spectrum.

But aggregate ~500 of them, and you may get close to the *investing* end.

31/

Thank you very much for reading to the end of another long thread.

I'm very curious to hear *your* thoughts on investing vs speculation -- what do these terms mean to you, and how do you tell them apart?

Please enrich this discussion with your comments!

/End

Thank you very much for reading to the end of another long thread.

I'm very curious to hear *your* thoughts on investing vs speculation -- what do these terms mean to you, and how do you tell them apart?

Please enrich this discussion with your comments!

/End

• • •

Missing some Tweet in this thread? You can try to

force a refresh