1/ As 2020 is coming to a close, I wanted to share some of my favorite graphs / pictures I collected throughout the year.

2/ March was one of the fastest sell-offs in history.

3/ The world came to a stop.

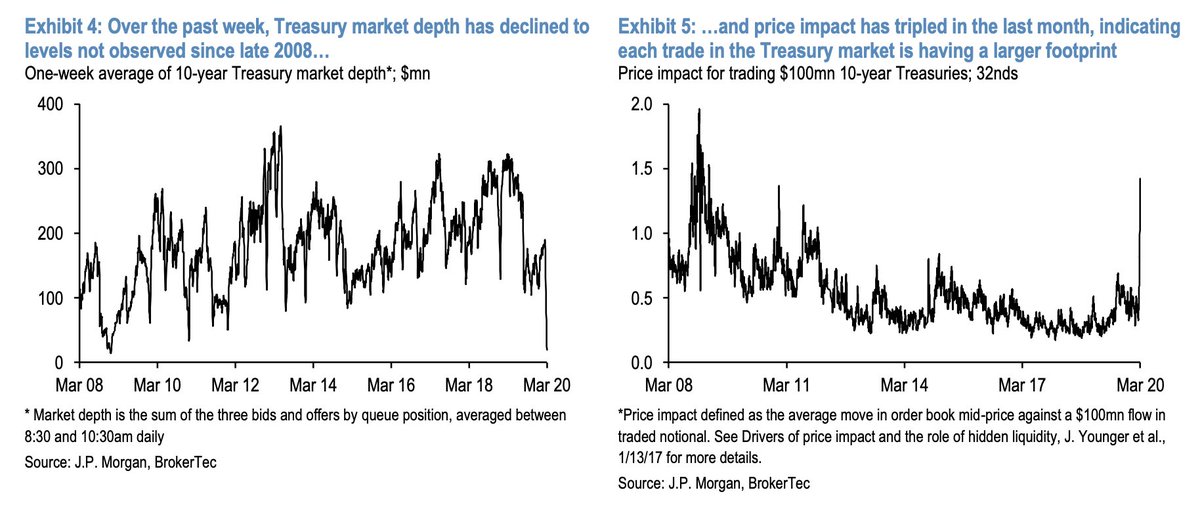

4/ Treasury market depth plunged.

5/ Treasury volatility hit extremes.

6/ Stock/bond correlations broke down

7/ "Gallows humor" by yours truly

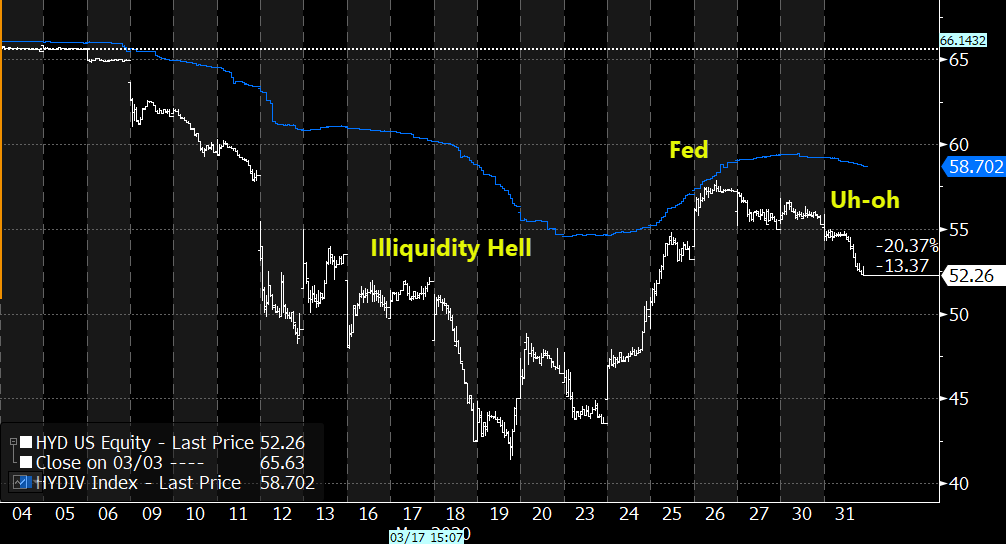

8/ Corporate bond ETFs ($LQD) fell 20% in 2 weeks while IG saw some of the largest outflows ever.

9/ Bond ETF prices meaningfully diverged from NAV.

10/ So much so that there might be some interesting optionality embedded in holding bond mutual funds?

(h/t @EconomPic)

(h/t @EconomPic)

11/ People mistook $ZOOM for $ZM.

12/ The SEC had something to say about it.

13/ Variance Swaps blew up.

14/ The intraday / overnight conundrum continues.

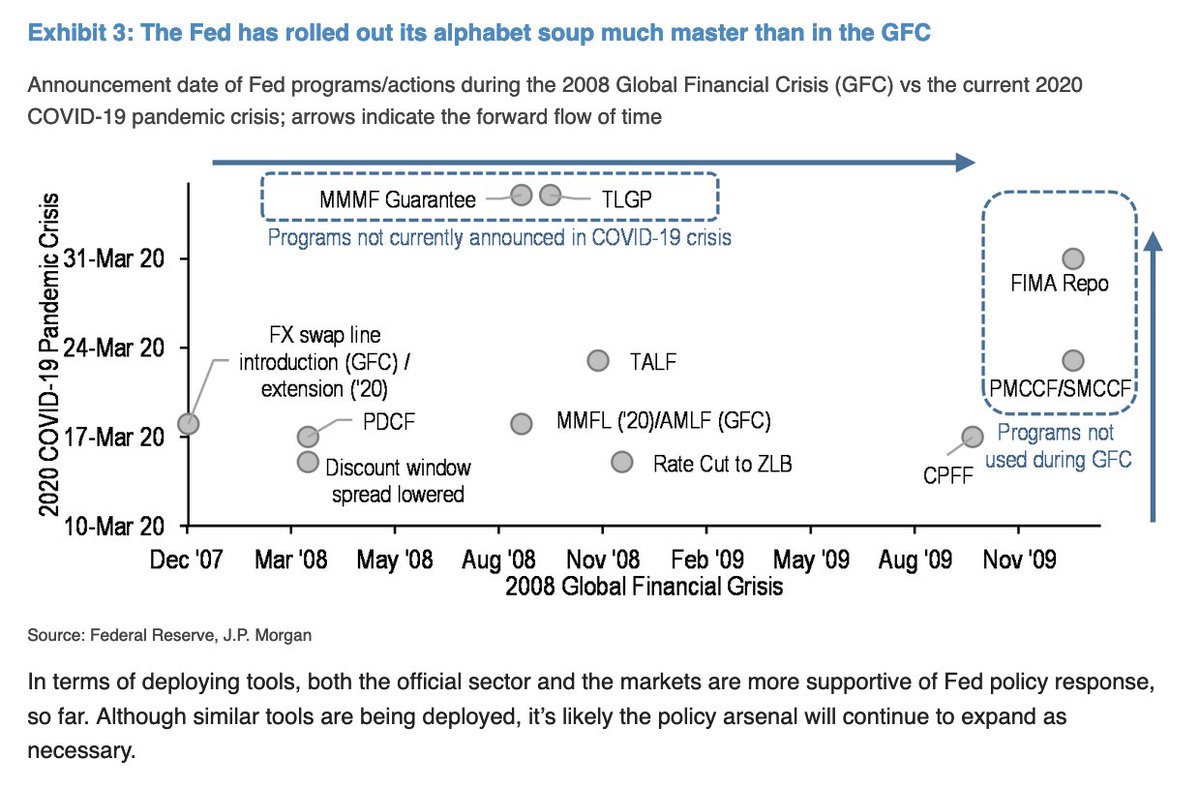

15/ The Fed unrolls the entire 2007-2009 playbook in just a few weeks.

16/ And they start buying bond ETFs.

(Okay, not technically, but whatever.)

(Okay, not technically, but whatever.)

17/ IG and HY issuance 🚀

19/ Factor vol starts getting extreme

20/ Momentum had a -16.4σ move

(Yes, yes, I know, fat tails, yada yada)

(Yes, yes, I know, fat tails, yada yada)

22/ The "call option casino"

23/ Okay, folks, what did I miss? Add below! 👇

24/ Can’t believe I missed this one...

25/ HODLers rejoice!

26/ Can’t not mention $TSLA’s meteoric rise here!

(Equity issuance suggests Elon’s not one to look a gift horse in the mouth)

(Equity issuance suggests Elon’s not one to look a gift horse in the mouth)

• • •

Missing some Tweet in this thread? You can try to

force a refresh