To avoid this, do a monte carlo analysis and find out the probabilities of range of drawdowns and work with leverage on your system accordingly.

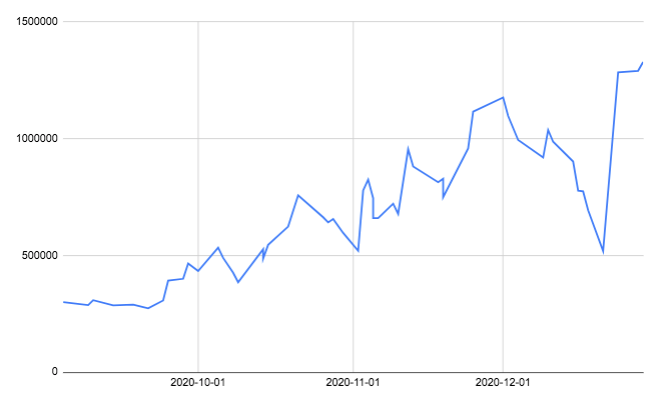

For ex: a system I trade currently, has a historical maxDD of 4.76% and recently it hit a maxDD of about 5.5%.

For ex: a system I trade currently, has a historical maxDD of 4.76% and recently it hit a maxDD of about 5.5%.

https://twitter.com/TarunNayak2905/status/1332256659159224320

On conducting monte carlo analysis of the system, I understood that the probability of maxDD to be below 5% is only ~3%.

There was about 61% probability of the maxDD to be between 5-10%

and ~2% probability that it could be around 20-40%.

You need to be aware of these.

There was about 61% probability of the maxDD to be between 5-10%

and ~2% probability that it could be around 20-40%.

You need to be aware of these.

Once you know the odds of a certain range of maxDD happening, then you can confidently deploy your strategy.

You'd also face drawdowns that lie within your comfortable range instead of being misled by just the historical maxDD as it happened in the series of trades historically.

You'd also face drawdowns that lie within your comfortable range instead of being misled by just the historical maxDD as it happened in the series of trades historically.

Check the thread with the attached tweet. I have written briefly about monte carlo analysis here.

https://twitter.com/theBuoyantMan/status/1346038756961255425?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh