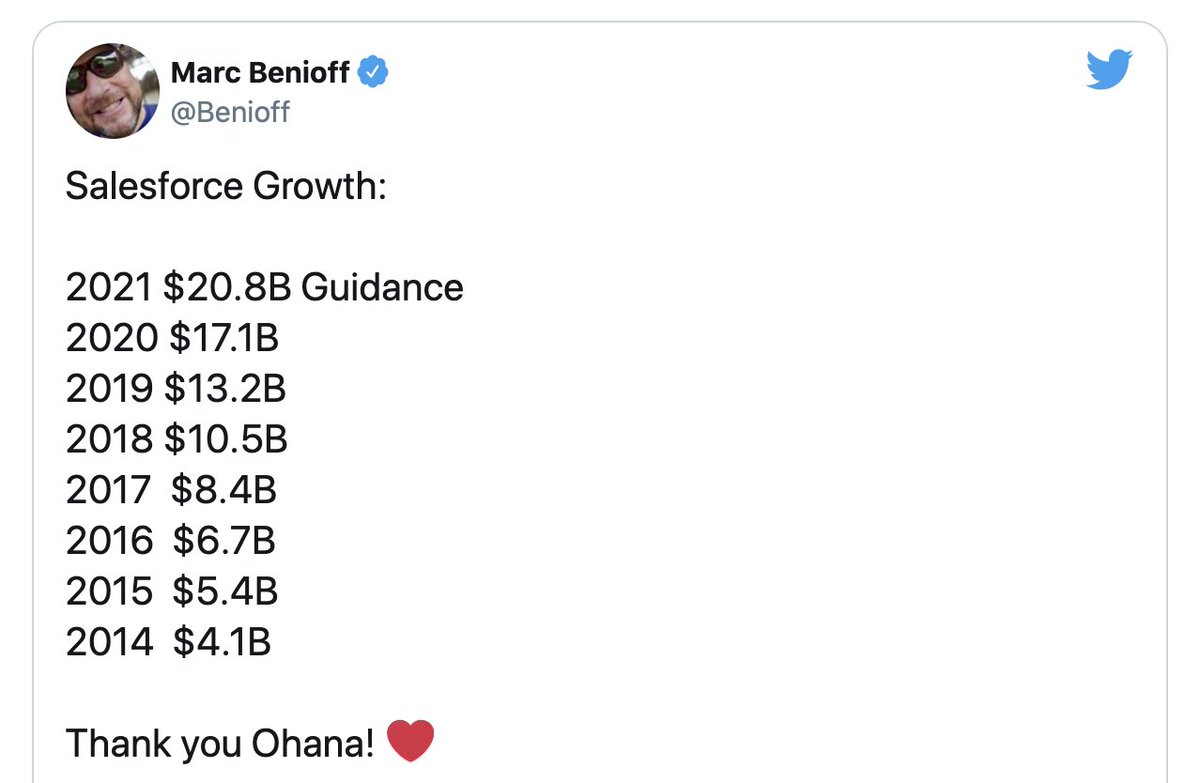

So Salesforce is the grandperson of SaaS software

The first to hit $100B in market cap

The first to do $10B+ in ARR (and only so far)

And yet, in many ways we know >less< about Salesforce that we used to

It's not just a CRM anymore

5 Interesting Learnings:

The first to hit $100B in market cap

The first to do $10B+ in ARR (and only so far)

And yet, in many ways we know >less< about Salesforce that we used to

It's not just a CRM anymore

5 Interesting Learnings:

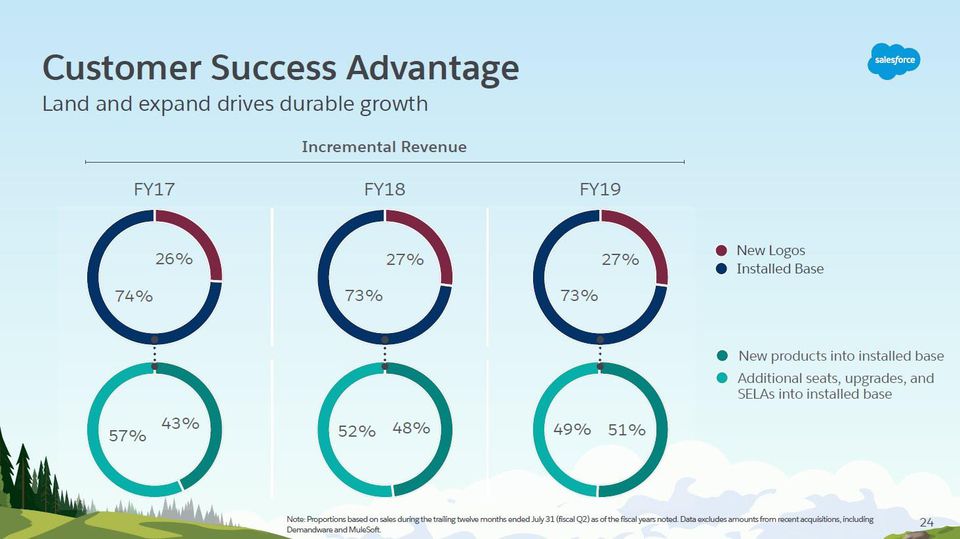

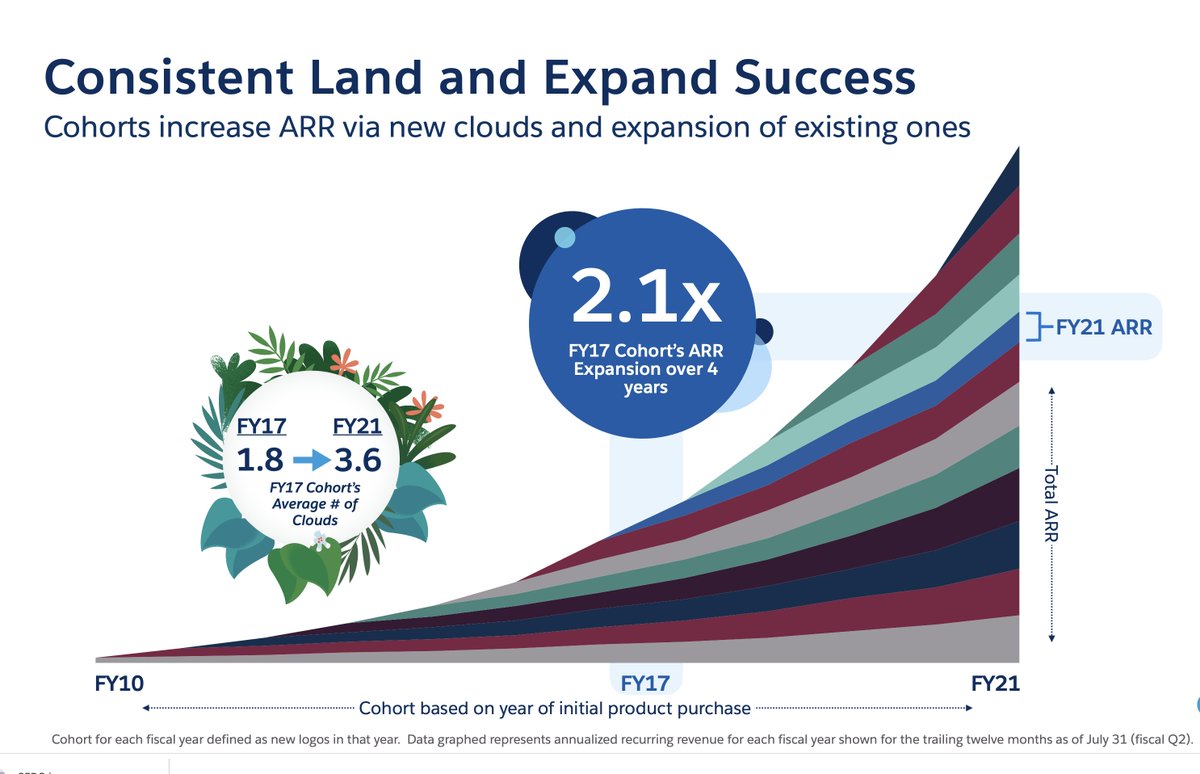

#1. 73% of Salesforce’s customers come from the installed base. Let that sink in.

This is why in the end, Net Revenue Retention is the #1 most important metric in SaaS.

This also means that Salesforce could basically still hit 73% of its plan with 0 new customers.

This is why in the end, Net Revenue Retention is the #1 most important metric in SaaS.

This also means that Salesforce could basically still hit 73% of its plan with 0 new customers.

Put differently, their 2017 customers have, as a cohort, grown 2.1x

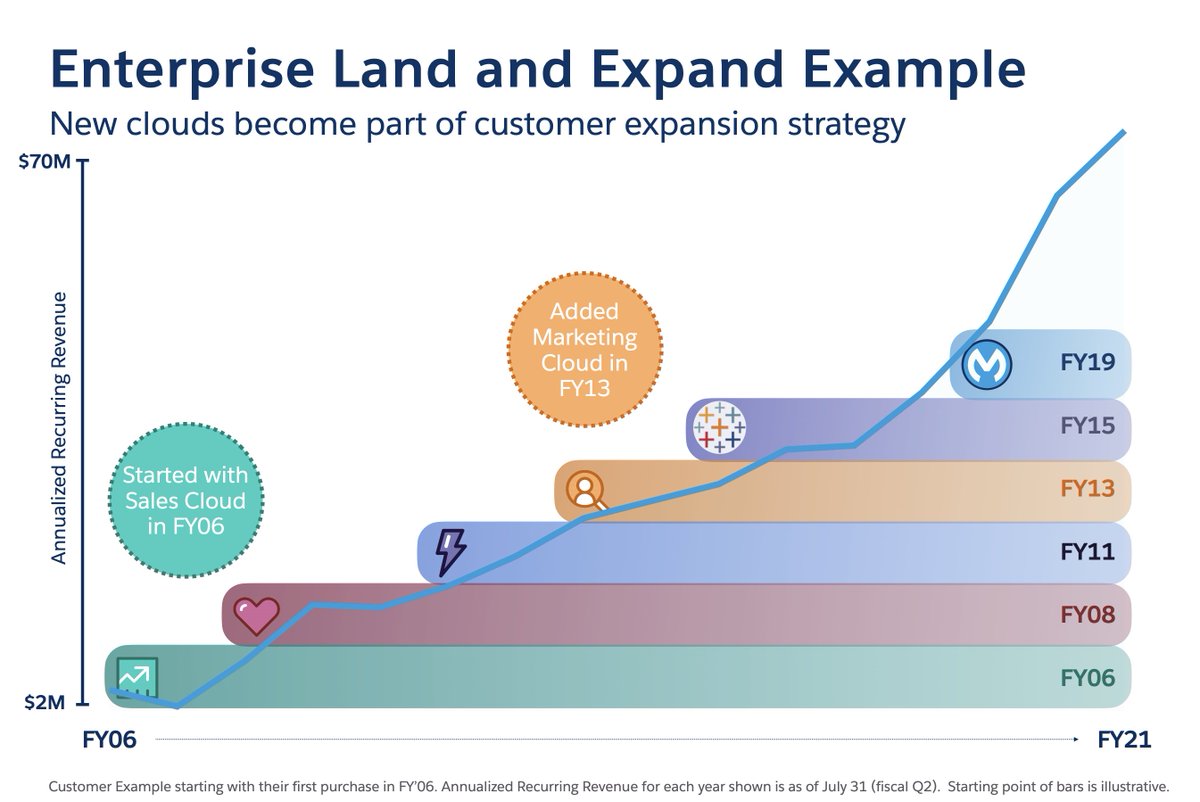

#2. Salesforce’s upsell is split about 50/50 between new seats and new products.

In the early days, you’ll probably only have new seats to sell.

But eventually, you’ll probably need a second or third product to sell. We talked about this re: Veeva, Twilio and more here:

In the early days, you’ll probably only have new seats to sell.

But eventually, you’ll probably need a second or third product to sell. We talked about this re: Veeva, Twilio and more here:

#3. The more products you sell, really, the more problems you solve — the more you make.

This is something a bit non-obvious. Salesforce’s customers that buy > 1 product overall, spend a stunning 10x more.

This is something a bit non-obvious. Salesforce’s customers that buy > 1 product overall, spend a stunning 10x more.

This skews a lot b/c the customers that buy more “Clouds” from Salesforce are bigger companies. Still, the more big problems you solve, the much more you make.

We also saw this Box, where NRR was >profoundly< higher when customers bought 2-3+ products beyond core Box product

We also saw this Box, where NRR was >profoundly< higher when customers bought 2-3+ products beyond core Box product

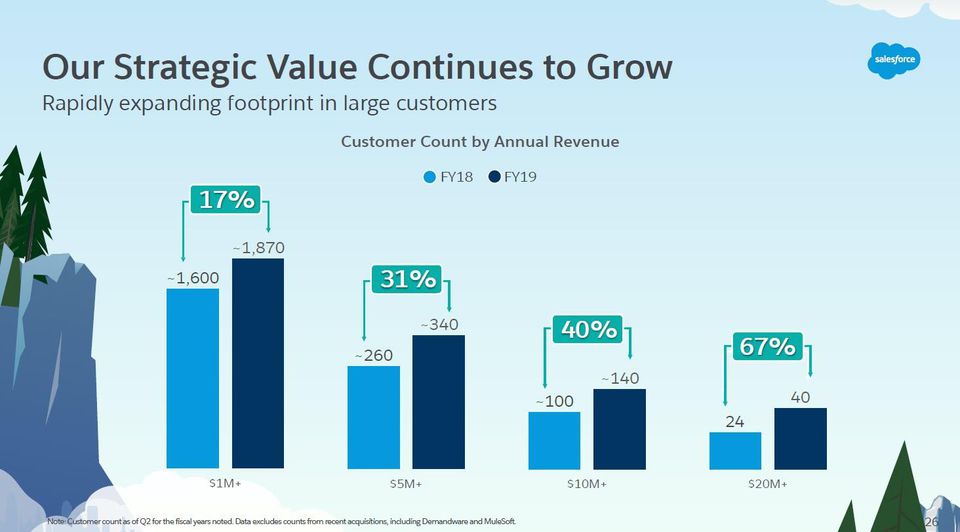

#4. Salesforce has >2,000+ customers that spend $1m annually.

That’s a lot more than the 500 in the “Fortune 500”. As you begin to go upmarket ... assume you have at least 2000+ mega-accounts to target.

No excuses.

That’s a lot more than the 500 in the “Fortune 500”. As you begin to go upmarket ... assume you have at least 2000+ mega-accounts to target.

No excuses.

#5. Salesforce’s largest customers are growing the fastest.

Salesforce also has 200+ Customers that spend $10m+ and ~40 spending $20m+ annually.

So when you start to go upmarket, lean in here. It can last for decades

Salesforce also has 200+ Customers that spend $10m+ and ~40 spending $20m+ annually.

So when you start to go upmarket, lean in here. It can last for decades

And finally, bonus point:

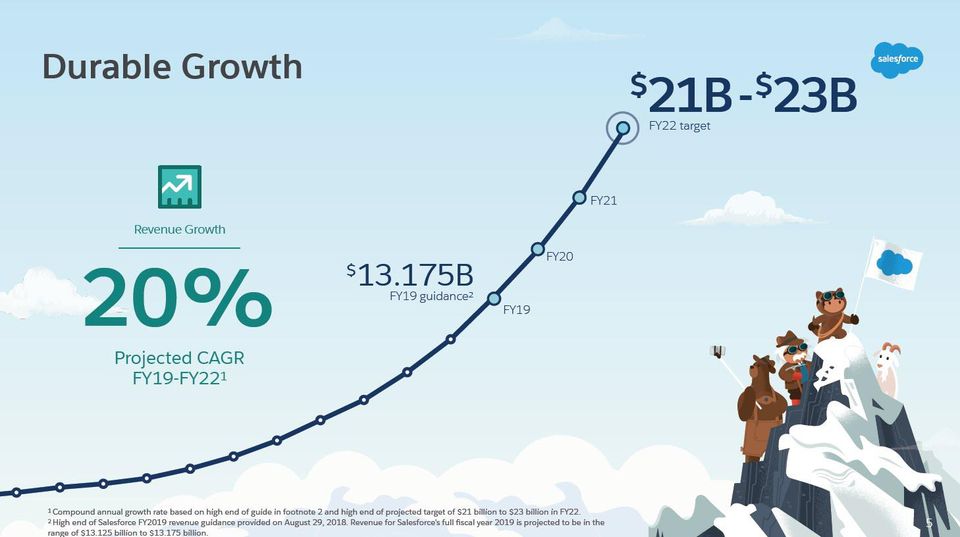

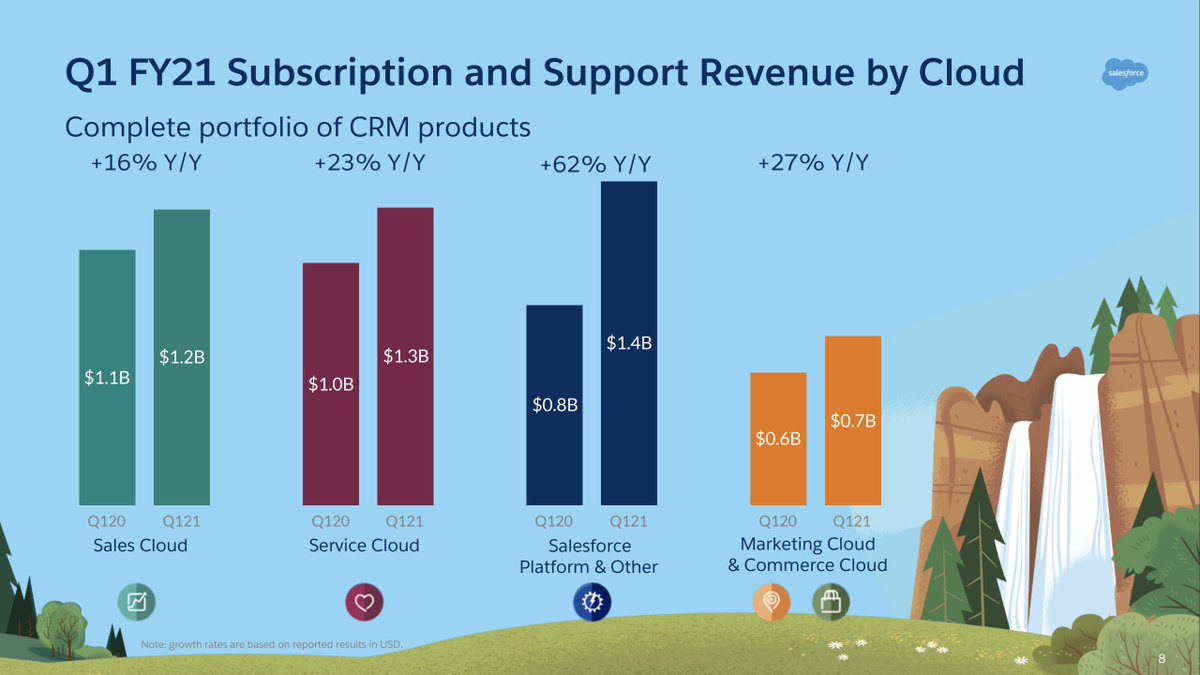

"Sales" is only Salesforce's #3 product line. And it's slowest growing at +16% YoY.

Your TAM over time is what you make of it, folks.

"Sales" is only Salesforce's #3 product line. And it's slowest growing at +16% YoY.

Your TAM over time is what you make of it, folks.

SaaS.

If you invest in it ...

It Compounds

If you invest in it ...

It Compounds

• • •

Missing some Tweet in this thread? You can try to

force a refresh