#nipponlifeindia #Q3marketupdates

Business Highlights • Dec'20

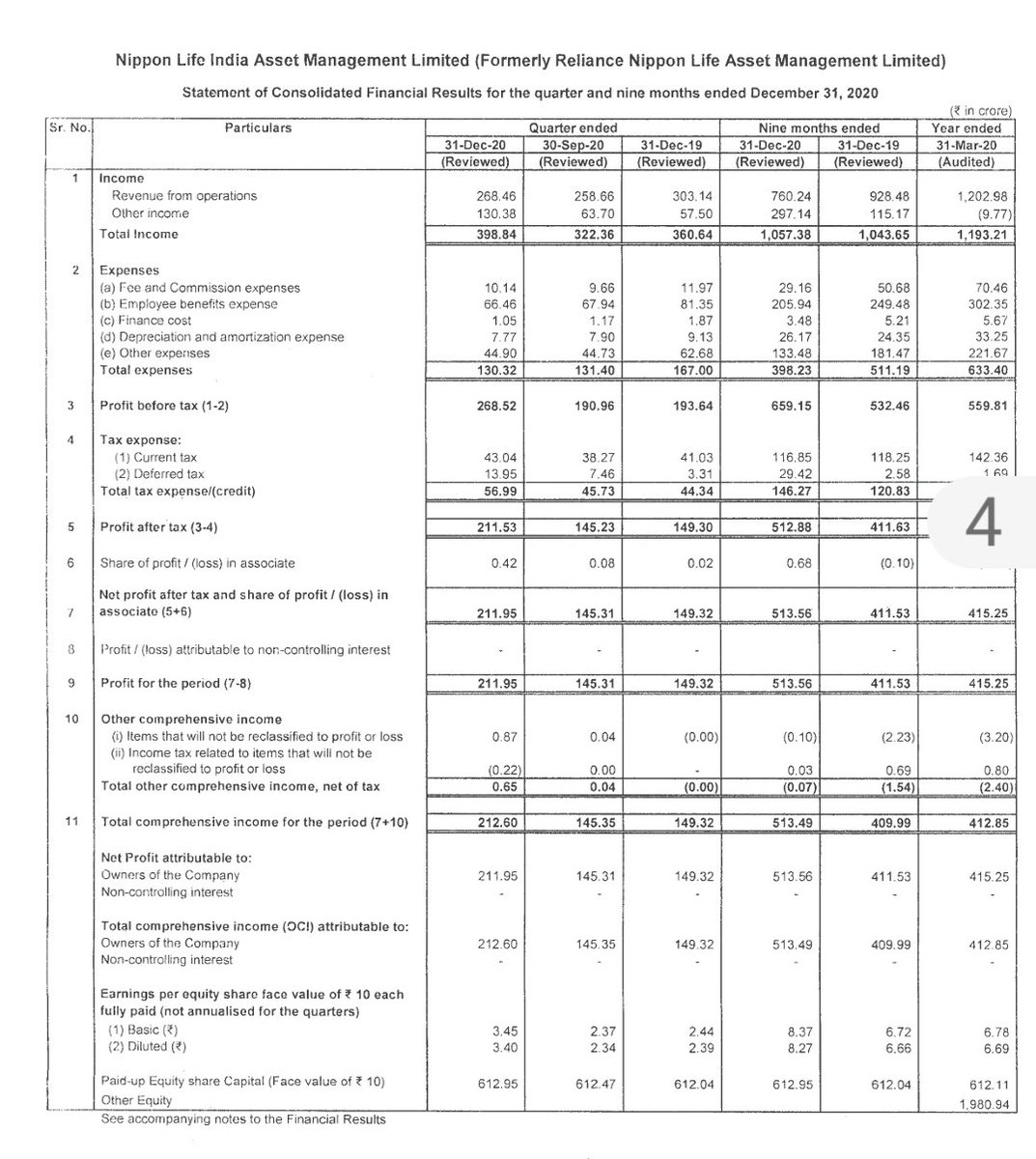

AUM 3,52,360 crore ($ 47bn)

Q3fy21 avg AUM 2,13,033 cr($ 28.4 bn), share of Equity Assets rose to 39.1% of AUM vs 38.9% Q3fy20

Dec 20, NIMF has one of the largest retail assets in the Industry, at 58642cr ($7.8 bn)

Business Highlights • Dec'20

AUM 3,52,360 crore ($ 47bn)

Q3fy21 avg AUM 2,13,033 cr($ 28.4 bn), share of Equity Assets rose to 39.1% of AUM vs 38.9% Q3fy20

Dec 20, NIMF has one of the largest retail assets in the Industry, at 58642cr ($7.8 bn)

Retail assets 26% to NIMF's AUM

Dec 20, NIMF garnered AUM 38,753 cr ($ 5.2 bn) from 'Beyond the Top 30 cities' category ,forms 17.5% of NIMF's AUM vis-a-vis 16.0% for the Industry

As on Dec 20, Individual AUM was Rs. 108,182 cr ($ 14.4 bn) contributed 49% to NIMF's AUM

Dec 20, NIMF garnered AUM 38,753 cr ($ 5.2 bn) from 'Beyond the Top 30 cities' category ,forms 17.5% of NIMF's AUM vis-a-vis 16.0% for the Industry

As on Dec 20, Individual AUM was Rs. 108,182 cr ($ 14.4 bn) contributed 49% to NIMF's AUM

As of Q3fy21 NIMF is one of the largest ETF players with AUM of 33,939 cr ($ 4.5 bn) & mkt share 13%

Q3fy21 launched 2 NFOs in the passive category

As of Q3fy21 has 92 lakh investor folios, with annualised Systematic book of approx 8,000 cr ($ 1.1 bn)

Q3fy21 launched 2 NFOs in the passive category

As of Q3fy21 has 92 lakh investor folios, with annualised Systematic book of approx 8,000 cr ($ 1.1 bn)

As of Q3fy21 offers Category II & Category Ill Alternative Investment Funds & total commitment of approx 3,500 cr ($ 466 mn)

Geographical presence 290 location pan India

Q3 fy21 digital transactions upto over 4 lakh ,up 39% vs Q3fy20

Digital channel part 52% to new transactions

Geographical presence 290 location pan India

Q3 fy21 digital transactions upto over 4 lakh ,up 39% vs Q3fy20

Digital channel part 52% to new transactions

• • •

Missing some Tweet in this thread? You can try to

force a refresh