@LaurusLabs #lauruslabs #Q3marketupdates #Q3investorpresentations

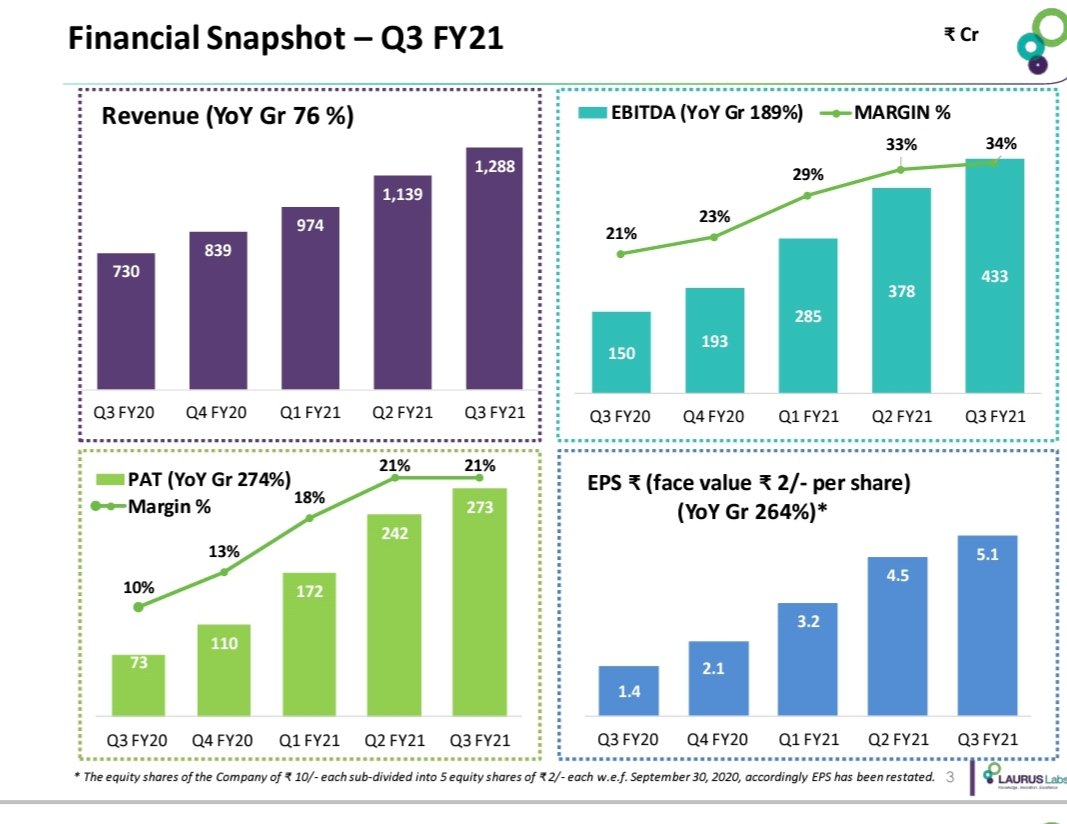

Q3fy21/20 in crs

Rev 1288/730 ,up 76%

Ebidta 433/150

PAT 273/73 ,up 274%

EPS 5.1/1.4

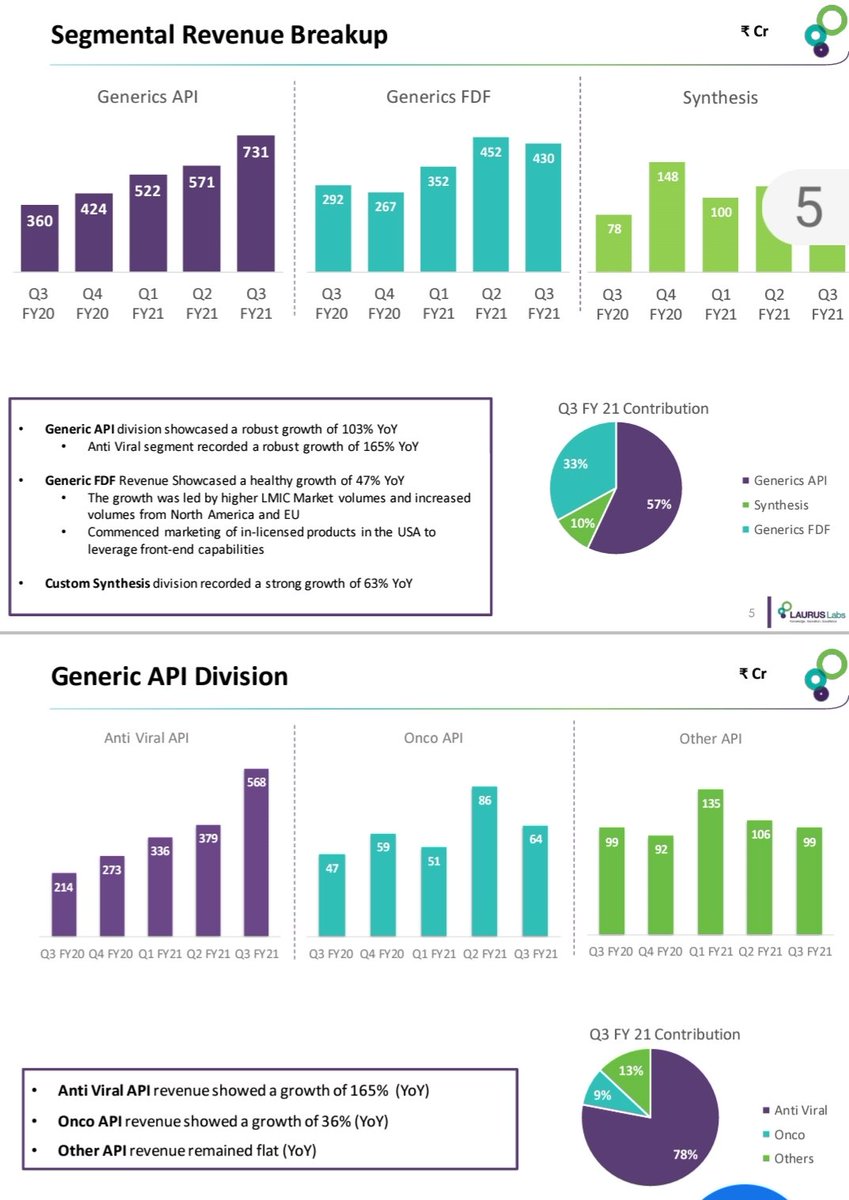

Generic API growth 103% yoy

ARVs up 175% yoy

Generic FDF up 47%

Custom synthesis up 63% yoy

Onco API growth 36%

Q3fy21/20 in crs

Rev 1288/730 ,up 76%

Ebidta 433/150

PAT 273/73 ,up 274%

EPS 5.1/1.4

Generic API growth 103% yoy

ARVs up 175% yoy

Generic FDF up 47%

Custom synthesis up 63% yoy

Onco API growth 36%

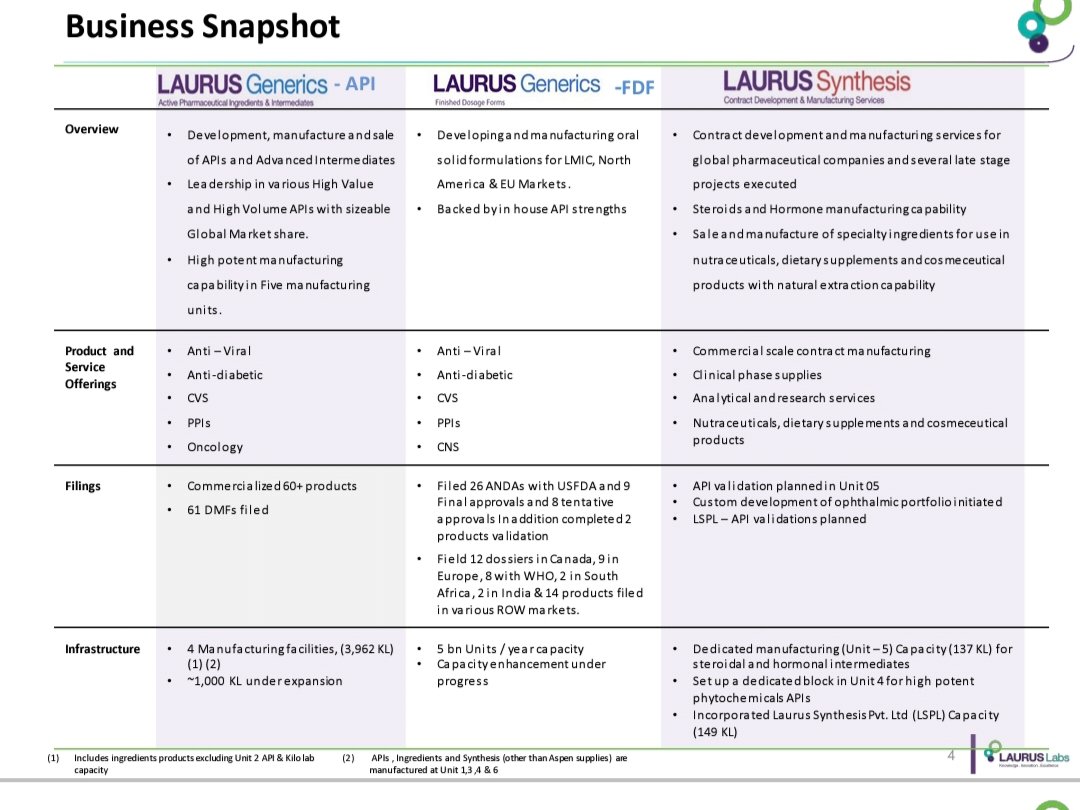

Generic APIs

ARV,Anti-DM,CVS,PPIs,Onco

Commercialized 60+ products

61 DMFs filed

Generic FDF

ARV,Anti-DM,CVS,PPIs,Onco

Filed 26 ANDAs with USFDA

9 final & 8 tentative approvals

Filed 12 dossiers in Canada, 9 in EU ,8 with WHO,2 in S.Africa, 2 in India

ARV,Anti-DM,CVS,PPIs,Onco

Commercialized 60+ products

61 DMFs filed

Generic FDF

ARV,Anti-DM,CVS,PPIs,Onco

Filed 26 ANDAs with USFDA

9 final & 8 tentative approvals

Filed 12 dossiers in Canada, 9 in EU ,8 with WHO,2 in S.Africa, 2 in India

Laurus Synthesis

CDMO services for Global pharma

Steroids,hormone mftg

Speciality ingredients in Nutraceuticals,dietary,cosmetics

Commercial scale mfg,clinical phase supplies,Analytics & research

API validation plannd in Unit 5

Optalmic initiated

LSPL-API validatn planned

CDMO services for Global pharma

Steroids,hormone mftg

Speciality ingredients in Nutraceuticals,dietary,cosmetics

Commercial scale mfg,clinical phase supplies,Analytics & research

API validation plannd in Unit 5

Optalmic initiated

LSPL-API validatn planned

Revenue breakup in crs

Q3fy21/20

Generic API 731/360

Generic FDF 430/292

Synthesis 127/78

Generic API

ARV 568/214

Onco 64/47

Other 99/99

Generic FDF 430/292

Entered in longterm partnership with leading generic player in EU for contract mfg

Synthesis CDMO 127/78 crs

Q3fy21/20

Generic API 731/360

Generic FDF 430/292

Synthesis 127/78

Generic API

ARV 568/214

Onco 64/47

Other 99/99

Generic FDF 430/292

Entered in longterm partnership with leading generic player in EU for contract mfg

Synthesis CDMO 127/78 crs

Synthesis CDMO

Revenue from custom synthesis, strong growth 63% yoy

Total active projects in CDMO stood at 49 in Q3

Partnered Large global pharma & mid ,small biotech companies

Commercial supplies ongoing for 4 products

Revenue from custom synthesis, strong growth 63% yoy

Total active projects in CDMO stood at 49 in Q3

Partnered Large global pharma & mid ,small biotech companies

Commercial supplies ongoing for 4 products

Revenue contribution

Fy20/fy16

Antiviral 82 /39

Onco API 8/7

Other API 3/ 11

Custom synthesis 7 /14

Generic FDF 0 / 29

9mnth fy21 / 20

ARV 39/38

ONCO 7/6

Other API 11/10

Custom synthesis 14/10

Generic FDF 29 /36

Fy20/fy16

Antiviral 82 /39

Onco API 8/7

Other API 3/ 11

Custom synthesis 7 /14

Generic FDF 0 / 29

9mnth fy21 / 20

ARV 39/38

ONCO 7/6

Other API 11/10

Custom synthesis 14/10

Generic FDF 29 /36

Completed acquisition of majority stake(72.55%) in Richcore Lifesciences Pvt ltd valued at 340 crs & 72.55% stake at 246.67 crs

Richcore Lifesciences to be renamed Laurus Bio Pvt Ltd

2 mfg facilities

1st has Fermentation capacity 10750 Lts while 2nd 1.8lk lts,available Mar21

Richcore Lifesciences to be renamed Laurus Bio Pvt Ltd

2 mfg facilities

1st has Fermentation capacity 10750 Lts while 2nd 1.8lk lts,available Mar21

Laurus Bio

Fast Growing Research Driven Bio-Mfg Company

Recombinant products - Animal origin free products for safer,viral free bio mfg

Precision Fermentation capabilities -scaleup expertise & large scale mfg capabilities

Strategic global partnerships for commercializn of product

Fast Growing Research Driven Bio-Mfg Company

Recombinant products - Animal origin free products for safer,viral free bio mfg

Precision Fermentation capabilities -scaleup expertise & large scale mfg capabilities

Strategic global partnerships for commercializn of product

Cumulative fillings

DMFs - 61

Patents filed 282

Patents approved 141

R&D spend

2016 - 85 cr (4.8%)

2020 - 134 (3.9%)

Outlook 2021 & beyond highlights :

Healthy order book for FY 21 & beyond in FDF CMO business with strategic partner in EU

DMFs - 61

Patents filed 282

Patents approved 141

R&D spend

2016 - 85 cr (4.8%)

2020 - 134 (3.9%)

Outlook 2021 & beyond highlights :

Healthy order book for FY 21 & beyond in FDF CMO business with strategic partner in EU

Several new customers added with progs in various clinical phases

Generic FDF segment contributed ~36% in 9M FY 21 vs 2% FY19

Synthesis business to show gains with new customer additions in CDMO

Acq Aspen’s S.African Subsidiary, foothold in worlds' largest Generic ARV Mkt

Generic FDF segment contributed ~36% in 9M FY 21 vs 2% FY19

Synthesis business to show gains with new customer additions in CDMO

Acq Aspen’s S.African Subsidiary, foothold in worlds' largest Generic ARV Mkt

Richcore acquisition to help enter high growth segments of AOF products, Enzymes & Biologics

Among top 5 in India in terms of Reactor capacities

All green field expansion turned Cash positive in FY20, near max utilization

Doubling our FDF capacity by FY22

Among top 5 in India in terms of Reactor capacities

All green field expansion turned Cash positive in FY20, near max utilization

Doubling our FDF capacity by FY22

Brown Field capex in existing sites to have shorter payback period and ROCE accretive

Acqd assets of an API Unit in Vizag to be used for backward integration ,pre clinical chemistry

Initiating green field expansion for all the divisions (API, FDF and Synthesis)

Acqd assets of an API Unit in Vizag to be used for backward integration ,pre clinical chemistry

Initiating green field expansion for all the divisions (API, FDF and Synthesis)

Unroll

@threadreaderapp

Compile

@threader_app

@tycoonmindset05 @thescorpionphil @nid_rockz

#pharma #cdmo #API #Nifty

@threadreaderapp

Compile

@threader_app

@tycoonmindset05 @thescorpionphil @nid_rockz

#pharma #cdmo #API #Nifty

• • •

Missing some Tweet in this thread? You can try to

force a refresh