Aarti Drugs conducted their earnings con-call today at 4:00 PM

"Target of 4500+ cr topiline till 2025"

@unseenvalue @darshanvmehta1 @sonalbhutra @Milind4profits

Here are the key highlights 😀👇

"Target of 4500+ cr topiline till 2025"

@unseenvalue @darshanvmehta1 @sonalbhutra @Milind4profits

Here are the key highlights 😀👇

Business Updates:

• 66.87% of revenue came from Export Market.

• Around 66% of the growth is driven by volume.

• Formulation segment grow at 5%.

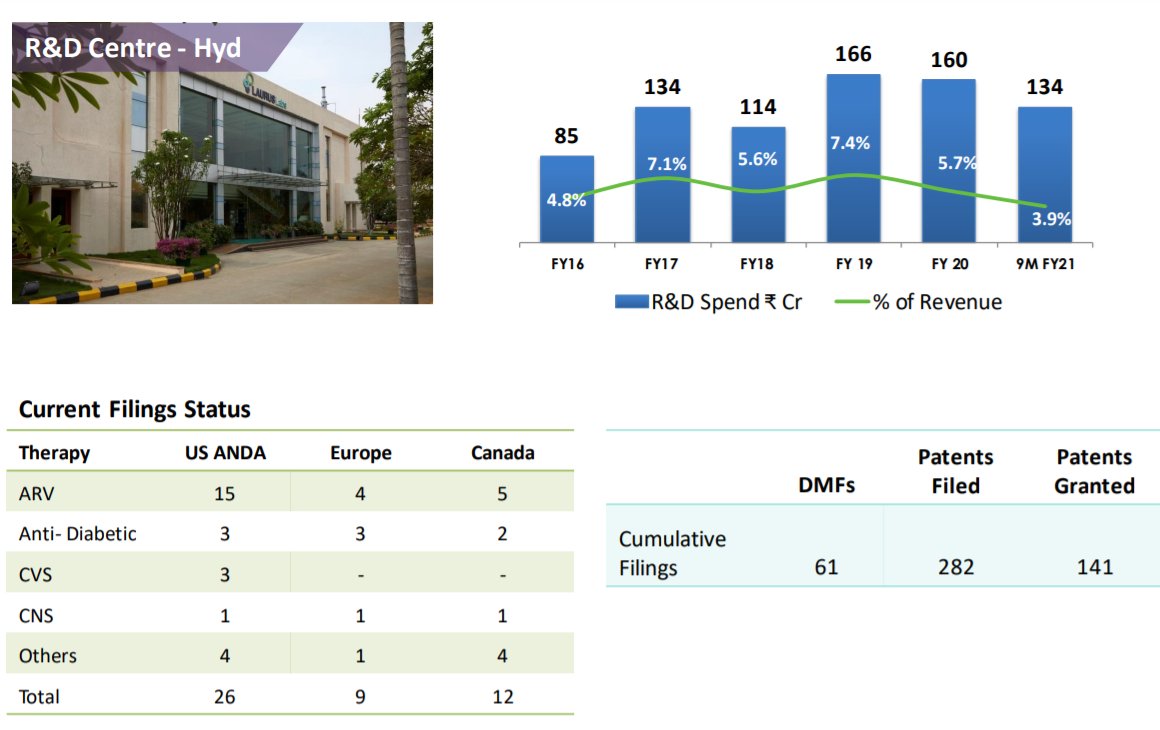

• Ramping up R&D facility both for API and formulation.

• CAPEX previously planned has been in inline.

• 66.87% of revenue came from Export Market.

• Around 66% of the growth is driven by volume.

• Formulation segment grow at 5%.

• Ramping up R&D facility both for API and formulation.

• CAPEX previously planned has been in inline.

Price in API:

• In September price has gone and has stabilize and after that the price is stable.

• As per current market scenario, mgmt expects 19-20% is doable, but its still not a new normal.

• In September price has gone and has stabilize and after that the price is stable.

• As per current market scenario, mgmt expects 19-20% is doable, but its still not a new normal.

CAPEX:

• Current API capacity revenue of additional 25%.

• Brown Facility and new green facility will be the main growth driver for the next 3-5 years, in order to achieve revenue target of 4,500+ cr in next 4-5 year.

• 40cr will go in this Q.

• Green field start in next year

• Current API capacity revenue of additional 25%.

• Brown Facility and new green facility will be the main growth driver for the next 3-5 years, in order to achieve revenue target of 4,500+ cr in next 4-5 year.

• 40cr will go in this Q.

• Green field start in next year

PLI:

• Company have applied for few products, and company expects one molecule to get but this will be announced in April. This product is for capital consumption (of around 60-65 cr), and 60-65 cr will external sales.

• This will have CAPEX of 120 crores.

• Company have applied for few products, and company expects one molecule to get but this will be announced in April. This product is for capital consumption (of around 60-65 cr), and 60-65 cr will external sales.

• This will have CAPEX of 120 crores.

• Government has also add export which again helps the business.

Post PLI scenario:

• In the absence of PLI scheme company has already able to grab 70% of the market share from China.

• Hence PLI will be just a supportive add on for the business.

Post PLI scenario:

• In the absence of PLI scheme company has already able to grab 70% of the market share from China.

• Hence PLI will be just a supportive add on for the business.

Company is planning for 7 products

2 for intermediates, 2 would be PLI product,1 would be Chloro Sulphur for internal consumption, another will be skin care

• Chloro sulphur will have good margin.

• Metformin will have similar margins and export approval will also add margin

2 for intermediates, 2 would be PLI product,1 would be Chloro Sulphur for internal consumption, another will be skin care

• Chloro sulphur will have good margin.

• Metformin will have similar margins and export approval will also add margin

Metformine capacity is 1100Mt per month.

China+ Policy:

• This will definitely help the business as Aarti has good business diversification and diversified customer will help the business well.

China+ Policy:

• This will definitely help the business as Aarti has good business diversification and diversified customer will help the business well.

Anti Dumping:

• There are other local player in the market, hence they can also raise price.

• This will help stabilizing the margins.

• It was started in September and now it will be 4-5 year

• There are other local player in the market, hence they can also raise price.

• This will help stabilizing the margins.

• It was started in September and now it will be 4-5 year

Geographical Revenue:

• Almost 90% of the business from America and then from Europe.

• This benefit is not big as company as import too.

• Almost 90% of the business from America and then from Europe.

• This benefit is not big as company as import too.

Capital Raising:

• With lower D/E and with D/E target of 0.7 (which is favorable for the business), company is planning for Term Debt (at 6-7%) and internal accruals for the CAPEX.

• Current Debt is 334 cr, out of which 186 is Term Loan.

• 9M CFO of business is around 140 cr

• With lower D/E and with D/E target of 0.7 (which is favorable for the business), company is planning for Term Debt (at 6-7%) and internal accruals for the CAPEX.

• Current Debt is 334 cr, out of which 186 is Term Loan.

• 9M CFO of business is around 140 cr

Specialty Sales (From CAPEX of 600cr):

• Specialty Sales has revenue potential for 1500cr . After captive consumption, external sales will be 1170-1200cr.

• Brown field expansion will decrease cost , and this will help compete with competitor which will further work on margin.

• Specialty Sales has revenue potential for 1500cr . After captive consumption, external sales will be 1170-1200cr.

• Brown field expansion will decrease cost , and this will help compete with competitor which will further work on margin.

Next Growth target.

• Next year company expects more on the volume growth (around +10%) than on the price growth.

• Company seems margin sustainable.

• Next year company expects more on the volume growth (around +10%) than on the price growth.

• Company seems margin sustainable.

• • •

Missing some Tweet in this thread? You can try to

force a refresh