Many sanguine about the Fed’s ability to clean up any undesirable inflation.

Maybe.

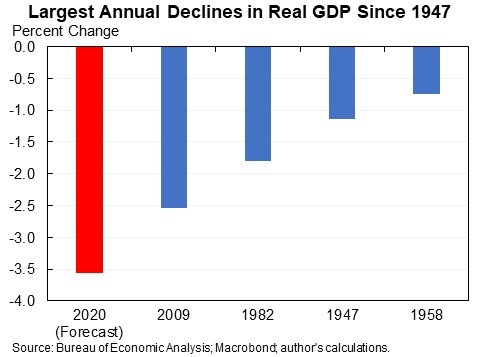

But in the past the Fed has mostly done this by causing recessions.

And the inverse of the flat Phillips curve may be a high sacrifice ratio—a lot of UR needed to reduce 1pp of inflation.

Maybe.

But in the past the Fed has mostly done this by causing recessions.

And the inverse of the flat Phillips curve may be a high sacrifice ratio—a lot of UR needed to reduce 1pp of inflation.

We have overworried about inflation for decades. As I tweeted earlier markets still expect below target inflation (and presumably markets are factoring in a large rescue plan).

But still, worth thinking hard about how to balance all the risks, not an easy/obvious issue.

But still, worth thinking hard about how to balance all the risks, not an easy/obvious issue.

https://twitter.com/jasonfurman/status/1357715984845471745

And let me preregistration my view: if we get inflation of 3% I would argue for resetting that as our new target. And that would give us more space to deal with future recessions.

Some support a 4% target, I worry that would make inflation too noticeable to people so not worth it.

And pushing for a higher target when we could not even get up to 2 seemed a bit feckless, locking in 3 less so.

And pushing for a higher target when we could not even get up to 2 seemed a bit feckless, locking in 3 less so.

• • •

Missing some Tweet in this thread? You can try to

force a refresh