GDP for Q4 is coming out tomorrow. It won't tell us much about how the economy is doing very recently but will be a great moment to look back at 2020 as a whole and will provide some glimpses of 2021. A preview thread.

We only get GDP numbers for quarters not for months. If we got them for months GDP would likely have fallen in November and December. But the way the quarterly arithmetic works, GDP will likely be up around 4% at an annual rate in Q4. Not a good measure of now.

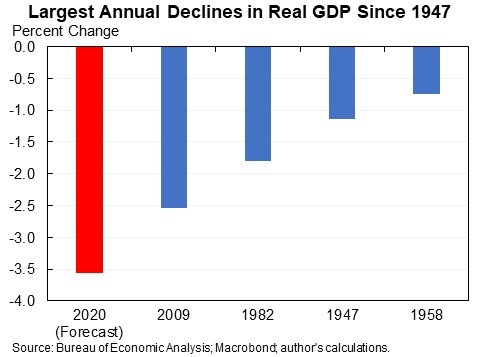

GDP will be down about 3-1/2 percent for 2020 relative to 2019. This is the largest decline in GDP since the demobilization from World War II in 1946, worse even than the 2.5 percent decline in 2009.

This is because Q2 GDP was very low and then it only partly recovered in Q3&Q4.

This is because Q2 GDP was very low and then it only partly recovered in Q3&Q4.

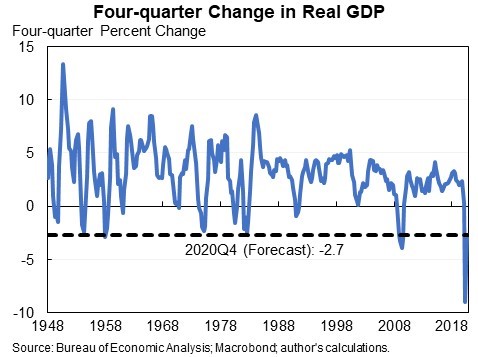

It is often more useful to do four-quarter changes, comparing GDP in 2019-Q4 to 2020-Q4. This is likely to be down about 2-1/2 percent. It should have been up about 2 percent.

So this means overall the economy was about 5 percent below trend at the end of 2020.

So this means overall the economy was about 5 percent below trend at the end of 2020.

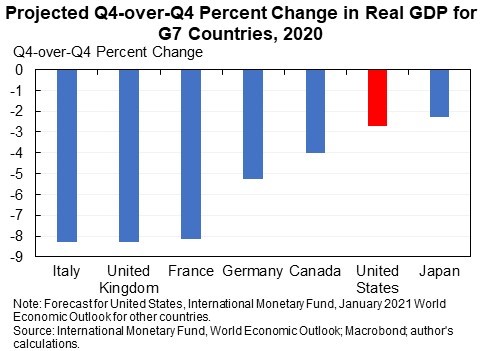

Notably, the US decline in GDP will be the smallest or second smallest of the G7 economies. It will also be much smaller than what was expected earlier this year.

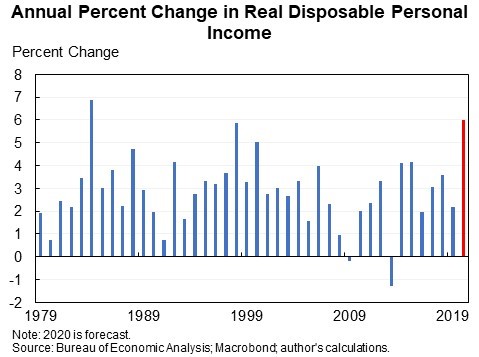

One of the remarkable facts about 2020: real disposable personal income was up around 6 percent. This is the largest increase since 1984 or 1998 (will need to see the exact number to know).

UI, checks, PPP created a wedge btwn GDP and what households actually got.

UI, checks, PPP created a wedge btwn GDP and what households actually got.

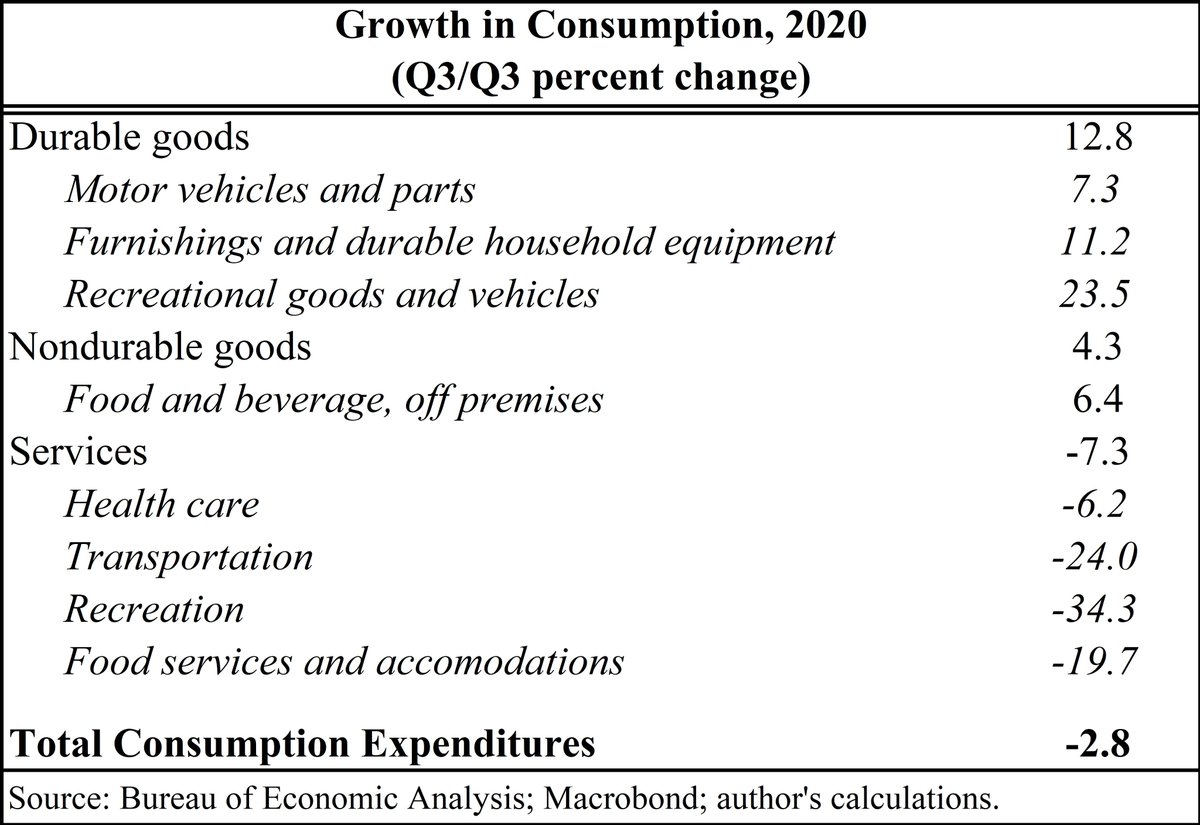

This increase in disposable income plus all the saving on reduced spending on services like restaurants and travel enabled households to increase their spending on goods like motor vehicles. On net consumer spending was down. Pattern evident already for 2020-Q3 vs. 2019-Q3.

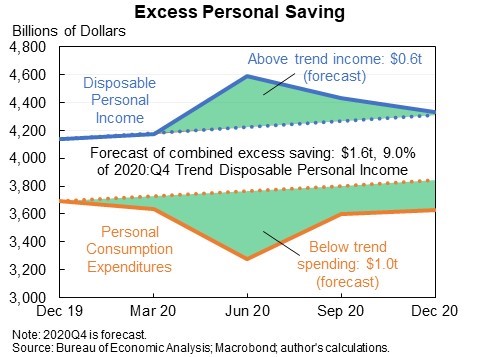

In sum, disposable income was ~$600b above trend in 2020 and spending was ~$1.0T below trend. That leaves ~$1.6T in “excess savings” available for spending in 2021 (plus more from capital gains). More coming this yr from Dec legislation / new legislation.

• • •

Missing some Tweet in this thread? You can try to

force a refresh