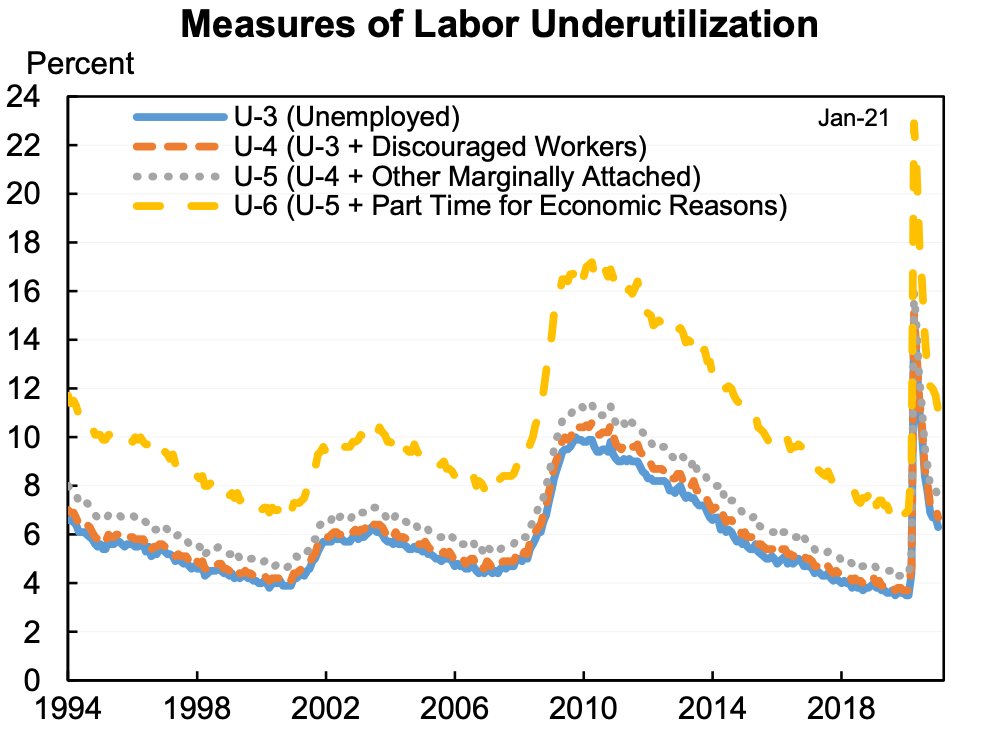

I've gotten questions about whether to emphasize U-6 as the "true unemployment rate". It is currently 11.1%.

I don't because I think the concept doesn't add much, it misses how unusually bad the labor market is now, is analytically flawed, and can be misleading.

Thread:

I don't because I think the concept doesn't add much, it misses how unusually bad the labor market is now, is analytically flawed, and can be misleading.

Thread:

The official unemployment rate is 6.3%. It is unemployed (people looking for work) divided by the labor force (working or looking for work).

U-6 is 11.1%, it adds in "marginally attached" (discouraged workers & would take a job if it came along) and involuntary part-time.

U-6 is 11.1%, it adds in "marginally attached" (discouraged workers & would take a job if it came along) and involuntary part-time.

DOESN'T ADD MUCH. U-6 is one of several alternative unemployment concepts produced monthly by the BLS. They are all useful to look at. But they also all pretty much up and down together so they rarely tell much of a different story.

MISSES HOW UNUSUALLY BAD THE LABOR MARKET IS NOW. The last time U-6 was around 11.1% the unemployment rate was 5.7%. If anything based on historic relationships U-6 makes the labor market seem bad (like in 2015) but not terrible (like in 2012).

The reason is that a large part of U-6 is part time for economic reasons (aka involuntary part time). This is up but actually not up an unusually large amount given the increase in unemployment. We've seen a lot of jobs lost but people with jobs, on average, working longer.

ANALYTICALLY FLAWED. U-6 puts equal weight on someone who cannot find a job and someone who can only find a 20 hr/week job but wants 40 hours. Both are problems but the former is worse. I sometimes use my own construct of U-5.5 which places half weight on involuntary unemployed.

MISLEADING. If we always used U-6 then we would get used the units and their historical comparisons. Many compare current U-6 to what the official rate used to be.

Also shift based on convenience (e.g., Trump shifted from Obama economy bad using U-6 to his good with U-3).

Also shift based on convenience (e.g., Trump shifted from Obama economy bad using U-6 to his good with U-3).

The best is to thoughtfully look at a range of indicators: official unemployment, participation, employment-population rate, U-6, hours, etc. But not everyone would look at all and I wouldn't replace that with a single-minded focus on U-6.

If you can only look at 1 number, then maybe Jay Powell's 10% or Willie Powell (no relation that he has admitted to me) & my 8.3% realistic UR. Both show the labor market is even worse than what you would think from the 6.3% headline unemployment rate.

https://twitter.com/jasonfurman/status/1359612185253617666?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh