1/ I spent a few years at Uber Eats watching us sometimes struggle to grow new businesses on top of rides. After a while I noticed a similar pattern at other big tech co's ($FB, $GOOG, $AMZN, $MSFT, etc). Below are my thoughts on why this happens and how it's related to marketing

2/ First, if you look at most big tech, they were all primarily started by engineers or "technophiles" and their core product grew virally with very little traditional marketing. Instead, there was a focus on "growth hacks" and improving the CX

3/ The consequence of this is that as the co grew, power, budget, and attention accrued to the engineering and product teams. Most importantly, the success of the original core biz created a dogmatic belief that "the best product wins" and "if you build it they will come"

4/ Second is what I call the "platform curse"; an over dependence on leveraging your existing customer base to build new products stunts or atrophies the co's "muscle" to acquire net new customers. In other words, the co never learns traditional brand and perf marketing

5/ As a result of the above, growing new bizs is framed as a product issue to be solved by eng solutions. More pop-ups, surfacing of referral codes, emails, bigger CTAs (Hangouts?), etc. $0 CAC and explosive growth is like crack. Co's hire top marketers but they aren't supported

6/ But this creates two issues. First, I think most successful products need to start small and target a sub-segment of the mkt. If you skip this step, you don't really thoroughly understand who your core users are. Worse yet, you may completely miss an entire segment of the mkt

7/ For ex, I'm convinced one of the reasons DoorDash won the suburbs and Uber Eats missed it was because we aggressively cross-sold our existing rider base which was predominately young professionals in urban cores. We didn't think about anything else for the first 1-2 years

8/ The second issue is that eventually you saturate your existing customer base and the growth stalls. And because you never took time to understand the needs of other customer segments and develop marketing capabilities, TAM is confined to your existing customer base

9/ There are a ton of examples of this, some will only become more obvious once the HBS case is written. Zoom vs. Hangouts, DoorDash vs. Uber Eats, etc. It always plays out the same way, partly because adding a new competencies (ie marketing) once a company is big is quite hard

10/ So I think there's two takeaways. If you're a small co and the product doesn't have any organic viral loops, it might be better to build a differentiated product that is "good enough" and focus on marketing capabilities

11/ Second, if you're at a big co, you might be better off building a business from scratch in a silo. Only once they figure out how to grow independently do you let them cross sell into your existing base to super charge growth

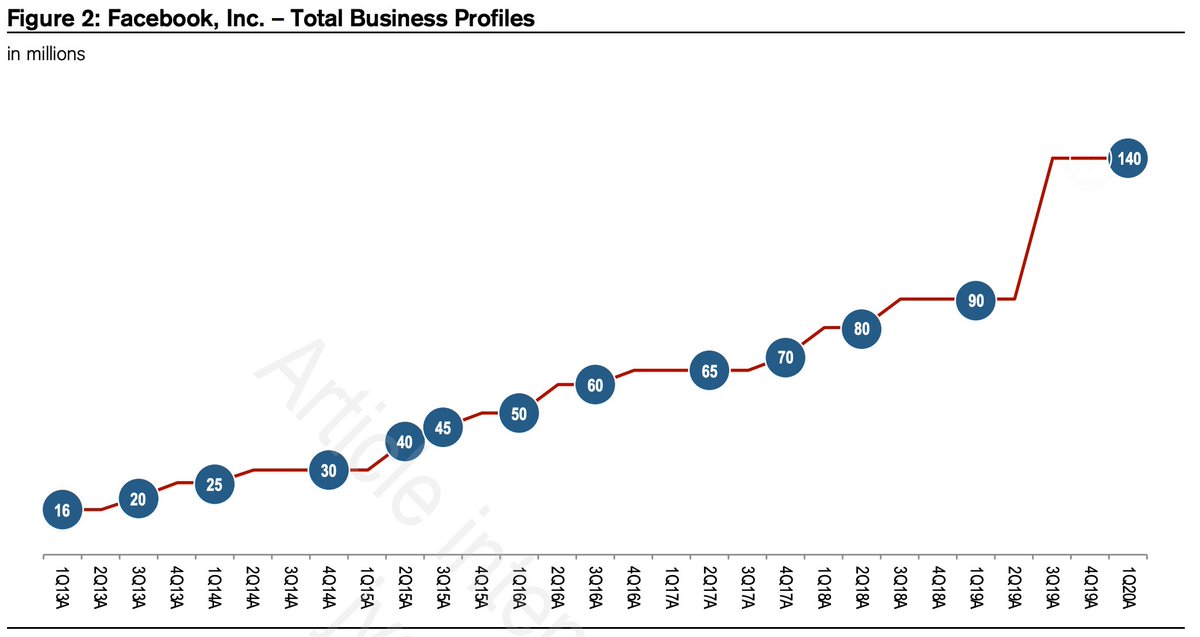

Speak of the devil..😬

• • •

Missing some Tweet in this thread? You can try to

force a refresh