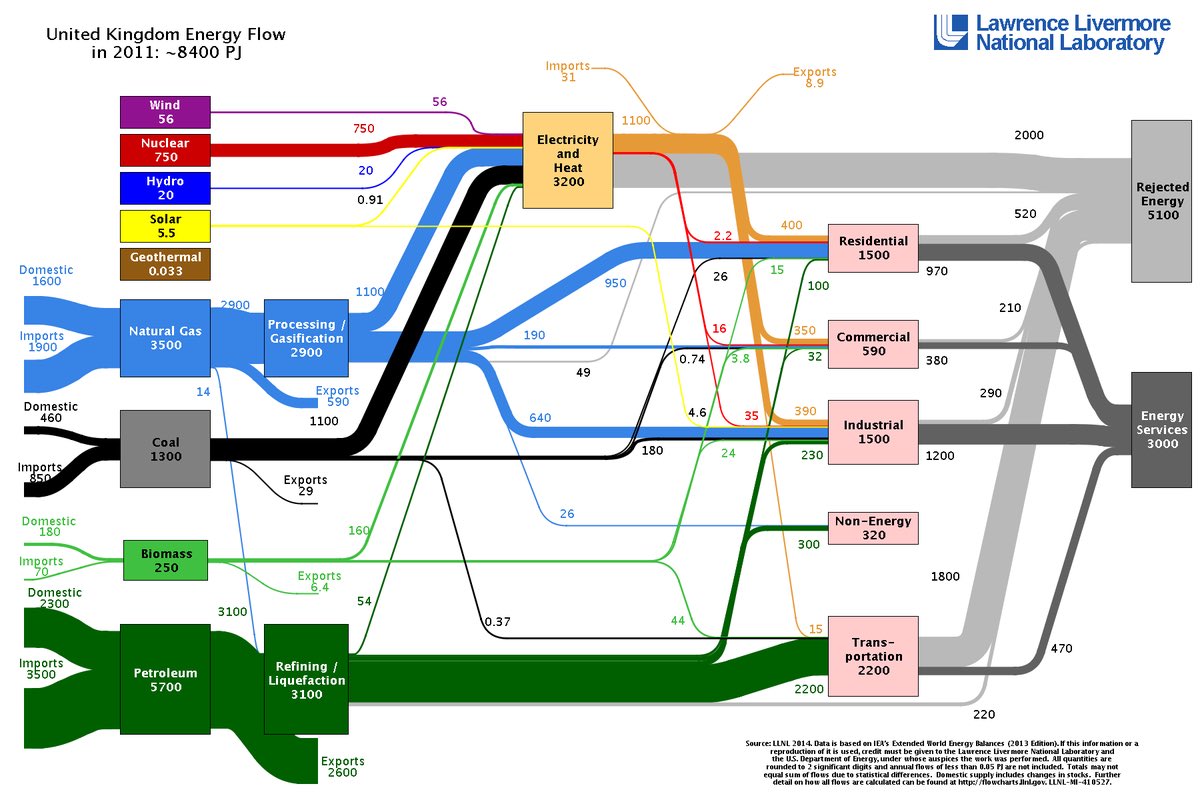

A RECENT VIEW ON ENERGY STORAGE

In the renewable electricity future, the UK will need an estimated 65 GWh of intra-day storage and 16 TWh of inter-seasonal storage

Both will have to be supplied at powers in the range 5-8 GW

csrf.ac.uk/2020/11/electr…

In the renewable electricity future, the UK will need an estimated 65 GWh of intra-day storage and 16 TWh of inter-seasonal storage

Both will have to be supplied at powers in the range 5-8 GW

csrf.ac.uk/2020/11/electr…

The economics of electricity storage "arbitrage" are dominated by the ’round-trip’ efficiency of the energy storage system

Pumped-hydro, Liquid Air and Compressed Air storage can have round-trip efficiencies up to 70%

Green Hydrogen has a round-trip efficiency of around 30-35%

Pumped-hydro, Liquid Air and Compressed Air storage can have round-trip efficiencies up to 70%

Green Hydrogen has a round-trip efficiency of around 30-35%

Lithium-ion batteries may offer round-trip efficiencies as high as 95%

Pumped Hydro has historically been the primary choice for Electricity Energy Storage worldwide

- Lithium ion batteries are now the major growth area, with the significant positives of fast response, excellent frequency management, increasing scale, and declining costs

- Lithium ion batteries are now the major growth area, with the significant positives of fast response, excellent frequency management, increasing scale, and declining costs

The 65 GWh of estimated intra-day storage needs for the UK gives us a sense of future scale for the battery energy storage industry

This compares with the UK's annual energy use of ~8,400 PJ to suggest a rate of 65 / 8,400 = 7.74 GWh per 1,000 PJ

- as a first approximation

This compares with the UK's annual energy use of ~8,400 PJ to suggest a rate of 65 / 8,400 = 7.74 GWh per 1,000 PJ

- as a first approximation

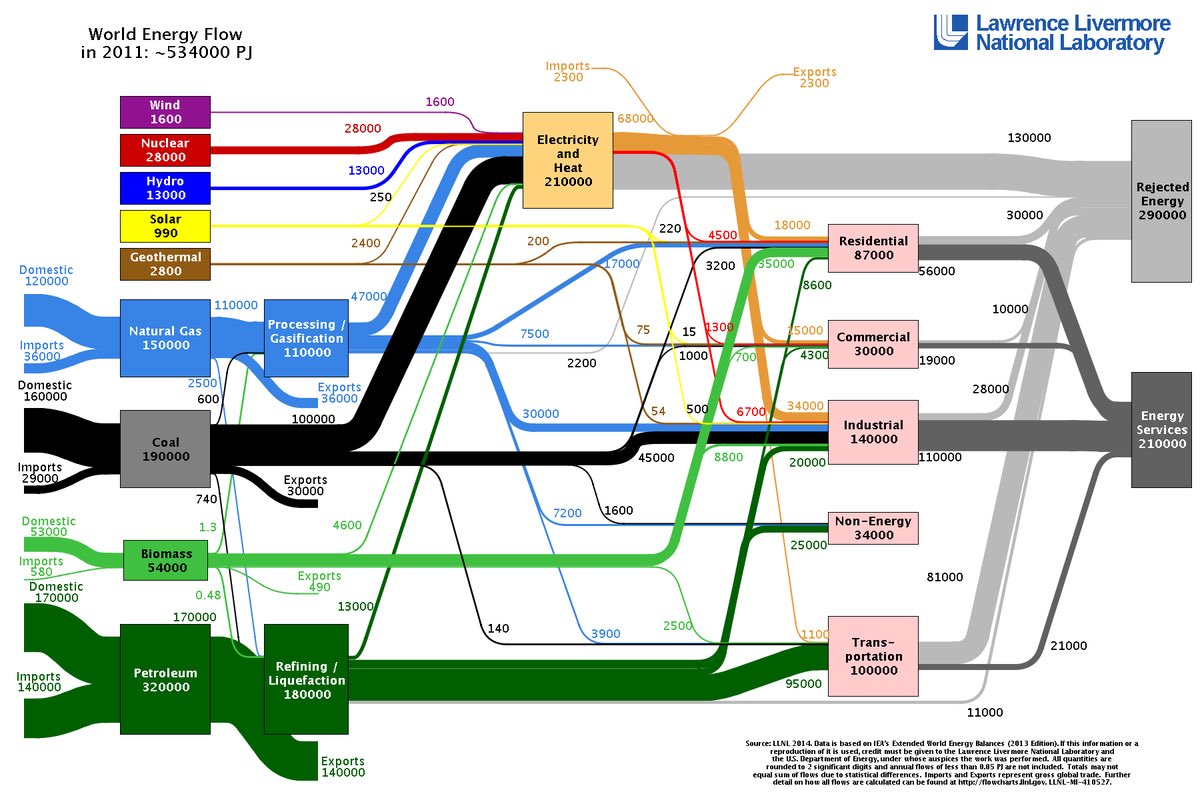

Applying this to the World's annual energy use of 534,000 PJs would give us :

534,000 PJ x 7.74 / 1,000 = 4,132 GWh = 4.1 TWh

534,000 PJ x 7.74 / 1,000 = 4,132 GWh = 4.1 TWh

This kind of scale is no longer out of reach as Battery GigaFactories start to proliferate in our World 4.0

• • •

Missing some Tweet in this thread? You can try to

force a refresh