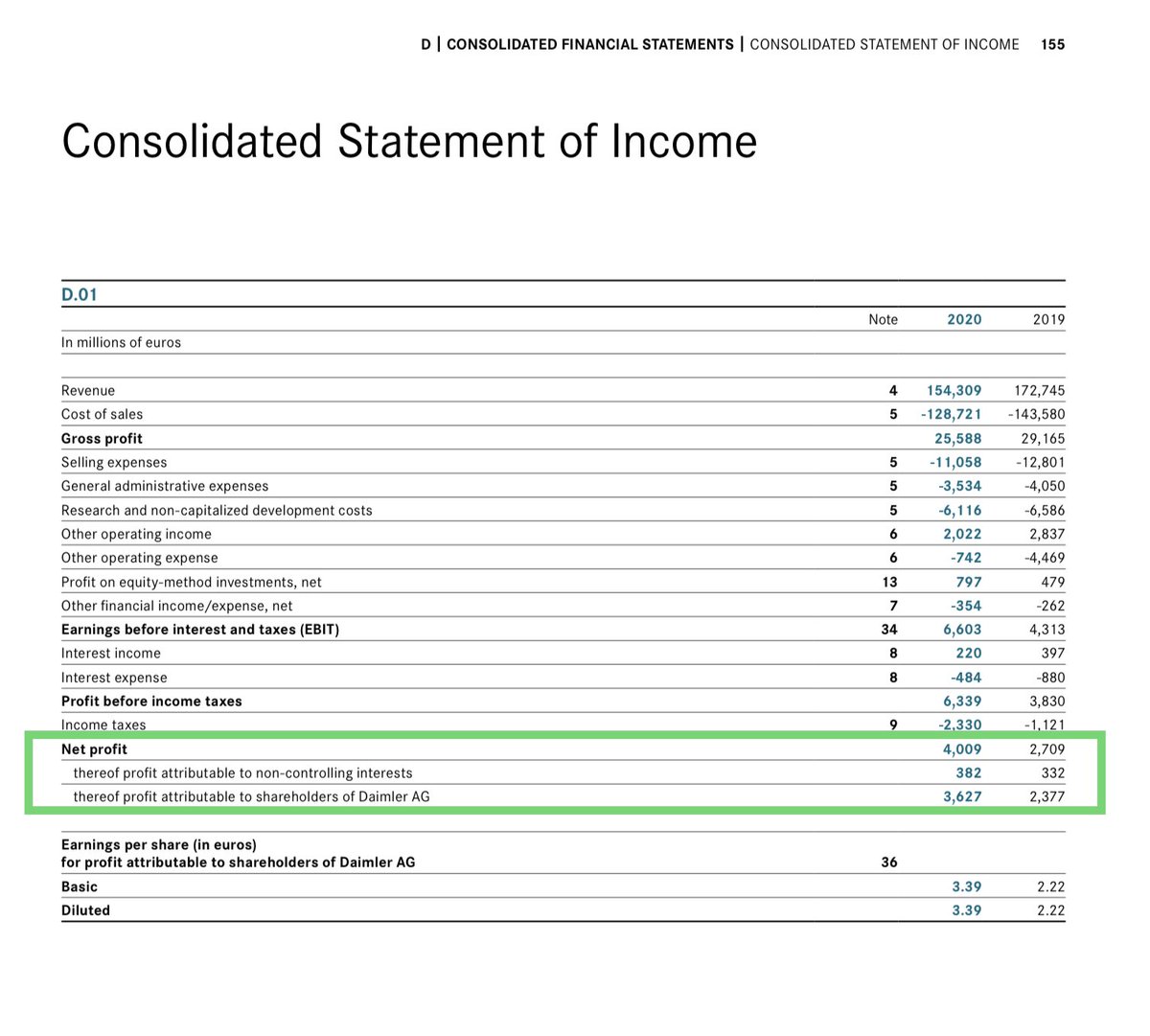

AN ANALYSIS OF SQUARE'S FINANCIAL REPORTS

We have reviewed SQ's 2020 Annual Report and find the current valuation very challenging

Especially given the two significant adjustments that we have to make when analyzing the reported results

We have reviewed SQ's 2020 Annual Report and find the current valuation very challenging

Especially given the two significant adjustments that we have to make when analyzing the reported results

https://twitter.com/jpr007/status/1364580067691536385

1. In both 2019 and 2020 there are one-off adjustments below the Operating Profit line that do not represent regular earnings

- in 2019 there was a gain from the sale of an asset group

- in 2020 there was a revaluation of their shares in DoorDash following its IPO

- in 2019 there was a gain from the sale of an asset group

- in 2020 there was a revaluation of their shares in DoorDash following its IPO

2. Secondly, their Bitcoin Revenues and Costs should really be reported on a Net basis otherwise they massively distort the apparent Revenue growth and Cost structure

- SQ earns very little money on those Bitcoin Revenues

- SQ earns very little money on those Bitcoin Revenues

This is the Revenue breakdown with Bitcoin reported Gross

- which gives the impression of high growth . . .

- which gives the impression of high growth . . .

. . . but with collapsing Gross Margins

A more realistic representation of the business is that they are actually seeing lower Revenue growth . . .

. . . at a declining rate from the past . . .

. . . but with increasing Gross Margins

- which unfortunately must have some upper limit

- which unfortunately must have some upper limit

Adjusting the Income Statement for Bitcoin on a Net basis has this effect in 2019 . . .

. . . and this result in 2020

- note the rapid escalation of the Operating Costs

- and the lack of Operating Profits and Net Income

- even as the growth rate falls

- note the rapid escalation of the Operating Costs

- and the lack of Operating Profits and Net Income

- even as the growth rate falls

We cannot find a way to support the current high stock price with future earnings when we attempt to project out the current operating parameters

• • •

Missing some Tweet in this thread? You can try to

force a refresh