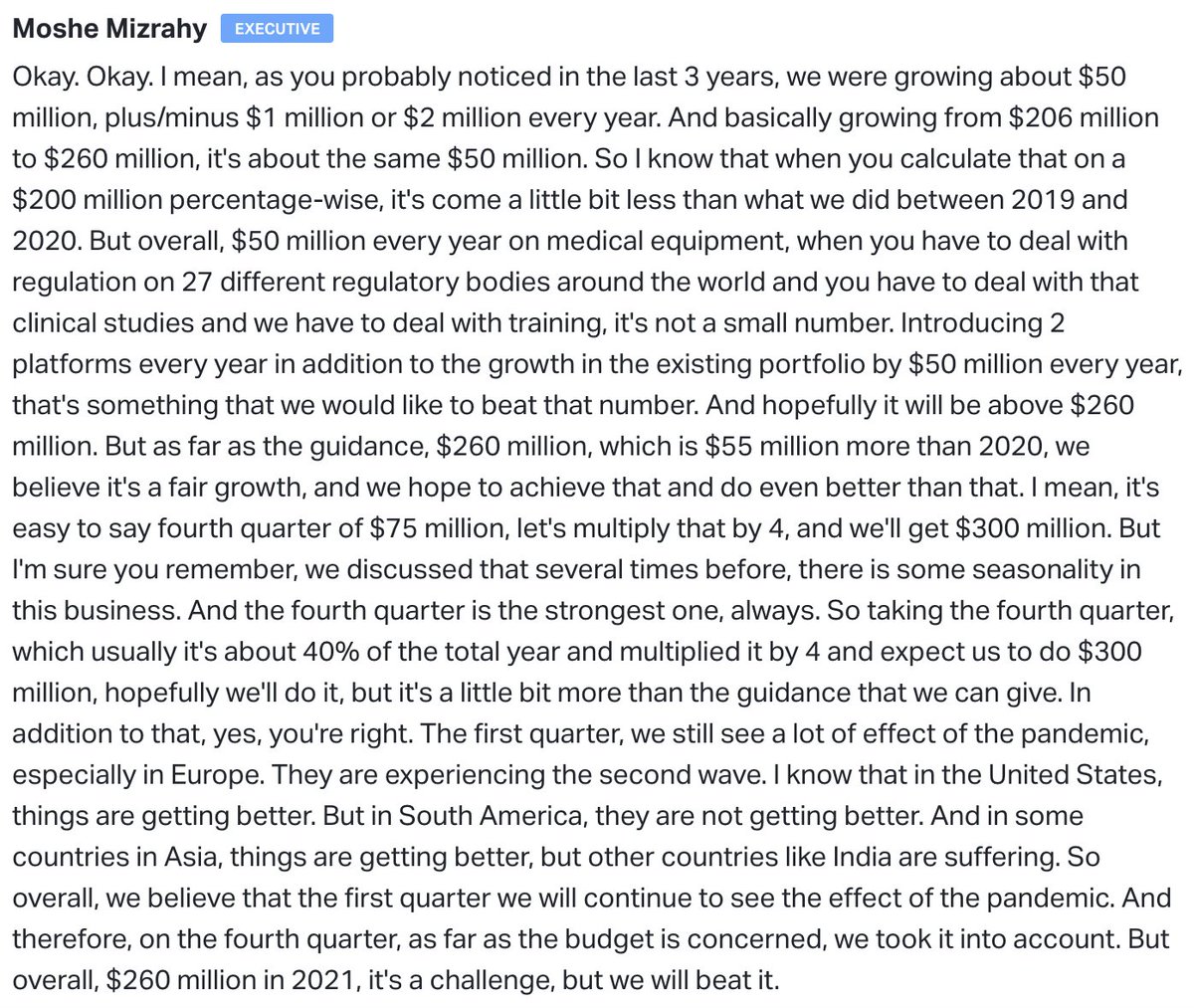

$BJ Reported a double small beat in Q4

Revenues beat by <1%

EPS beat by 4.4%

MFI up 11% YoY

Gross margins up 50 bps

No 2021 guidance

Comparable club sales ex. gas up 15.9% YoY

Leverage ratio down to 1.2x Adj. EBITDA from 1.3x in Q3 and 2.8x YoY

Revenues beat by <1%

EPS beat by 4.4%

MFI up 11% YoY

Gross margins up 50 bps

No 2021 guidance

Comparable club sales ex. gas up 15.9% YoY

Leverage ratio down to 1.2x Adj. EBITDA from 1.3x in Q3 and 2.8x YoY

All time high renewal-rate of 88%

Guides # of members to be flat or better in 2021

Guides MFI growth to be 4-5%

Plan to open 6 clubs in 2021 and 10+ in 2022

Mgmt. expects 2021 membership, sales, and profitability to be well ahead of historical averages

Guides # of members to be flat or better in 2021

Guides MFI growth to be 4-5%

Plan to open 6 clubs in 2021 and 10+ in 2022

Mgmt. expects 2021 membership, sales, and profitability to be well ahead of historical averages

Digitally enabled sales up 168% YoY

Long-term growth will be well above guidance given at 2018 IPO

"We expect dramatically higher unit growth rates as we push towards 10-plus units per year allowing us to tap into considerably expanded addressable markets and grow share"

Long-term growth will be well above guidance given at 2018 IPO

"We expect dramatically higher unit growth rates as we push towards 10-plus units per year allowing us to tap into considerably expanded addressable markets and grow share"

Easy renewal enrollment steady at 70%

Higher tier penetration up to 31% from 28% YoY

Membership per club for new clubs is 20% higher than average

Expect construction costs to be flat as lower real estate costs offsets higher lumber + steel costs

Higher tier penetration up to 31% from 28% YoY

Membership per club for new clubs is 20% higher than average

Expect construction costs to be flat as lower real estate costs offsets higher lumber + steel costs

New member basket size up 19%, same-day delivery usage 6x the normal member usage, app usage 2x the rate of normal members

Meaningful pickup in Capex in 2021 related to acquiring land and buildings

------

Meaningful pickup in Capex in 2021 related to acquiring land and buildings

------

The good: flat - LSD membership guide is well above consensus, gross margin expansion in the face of input inflation, taking share in a ton of areas, 10+ store openings in 2022 and onward provide a clear long-term guide

The bad: No EPS, EBITDA or sales guidance

The bad: No EPS, EBITDA or sales guidance

Like several COVID-winners, 2021 is going to be a hard year for comps and mgmt. clearly wants to compare 2 year growth to 2019 numbers vs. YoY growth from 2020 numbers

The short-term downside here is relatively limited by what will still be $2.5 - $2.8 in EPS in 2021

The short-term downside here is relatively limited by what will still be $2.5 - $2.8 in EPS in 2021

Moving to 2022 (maybe 2023)-2025, ~3-5% store count growth + 3-5% comps + ~5-6% MFI growth (includes potential fee increase in '22-'23) gets you 6-10% sales growth pretty easily

EPS will grow faster as cost controls are maintained + BJ's enters higher margin services areas

EPS will grow faster as cost controls are maintained + BJ's enters higher margin services areas

So without margin expansion, there's a pretty clear path to >10% EPS growth for the foreseeable future post-2021

I think the EPS multiple rerates to near 20x in 2022 if this happens, but again, shares will likely be range-bound by the multiple in 2021 given the hard comps

I think the EPS multiple rerates to near 20x in 2022 if this happens, but again, shares will likely be range-bound by the multiple in 2021 given the hard comps

Mgmt. did mention that there will have to be additions to distribution as they head further west, but this doesn't come into play till likely 2023

Shares are basically flat which is a fair reaction IMO. Analyst revisions are likely slightly downward given lack of visibility.

Shares are basically flat which is a fair reaction IMO. Analyst revisions are likely slightly downward given lack of visibility.

There's a lot to like long-term for a company trading at 14x NTM EPS

Given what will be a lumpy 2021, I may trim to adjust my position size in the coming weeks (currently 8%) and reallocate into what I believe are better opportunities, but no actions today.

Given what will be a lumpy 2021, I may trim to adjust my position size in the coming weeks (currently 8%) and reallocate into what I believe are better opportunities, but no actions today.

• • •

Missing some Tweet in this thread? You can try to

force a refresh