Personal Finance 101 – My learning’s about investing

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - youtube.com/c/KirtanAShah

And you can also join our Telegram channel for regular updates – t.me/kirtanshahcfp (2/n)

And you can also join our Telegram channel for regular updates – t.me/kirtanshahcfp (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

Return of premium means, if nothing happens to you in the 39 years term, the premiums you paid (minus of taxes) will be paid back to you. If something happens, both the policies (regular term & return of premium) pay you the same, 1 cr. (6/n)

Lets do some basic calculation,

(i) Without GST premium = 42670/118% = 36161

(ii) Premium returned at policy end if nothing happens = 36161*39 = 14,10,280 (7/n)

(i) Without GST premium = 42670/118% = 36161

(ii) Premium returned at policy end if nothing happens = 36161*39 = 14,10,280 (7/n)

(iii) vs that, if u invest the difference in premium 20,513 every yr for 39 years @ 6% post tax, future value will b 23,54,112 vs 14,10,280 paid by the policy

(iv) In other terms, the policy is only paying u 2.77% on the additional premium u r paying over the regular premium(8/n)

(iv) In other terms, the policy is only paying u 2.77% on the additional premium u r paying over the regular premium(8/n)

(B) Term insurance with limited pay is another trick.

They will advertise it saying instead of paying 22,157 for 39 years (total 8,64,123), pay 48,830 for 10 years (Total 4,88,300 and save 43% premium, but, the trick here is time value of money. (9/n)

They will advertise it saying instead of paying 22,157 for 39 years (total 8,64,123), pay 48,830 for 10 years (Total 4,88,300 and save 43% premium, but, the trick here is time value of money. (9/n)

Lets do some basic calculation,

(i) If u calculate the present value of both stream of cash flows @ same rate of 6%, Present Value of regular pay (39 years) is 3,51,100 & 4 limited pay (10 years) is 3,80,957. In today’s term, u r paying 29,857 more in limited premium plans(10/n)

(i) If u calculate the present value of both stream of cash flows @ same rate of 6%, Present Value of regular pay (39 years) is 3,51,100 & 4 limited pay (10 years) is 3,80,957. In today’s term, u r paying 29,857 more in limited premium plans(10/n)

(ii) One more big difference is recovery of premium. In first 10 years, in limited pay, insurance company has recovered 10 out of 10 premiums vs. 10 out of 39 premiums in regular pay. So, in case the claim gets triggered in 11th year, limited pay option is at disadvantage. (11/n)

(iii) In limited pay option, insurance companies offer options from single pay to 5 years to 10 years. The lesser the payment term, the bigger will be the set back. (12/n)

(C) Third variant is Term Insurance with life cover upto 99 years, which is also a similar story. Read our blog for the data points - fpa.edu.in/blog/personal-… (13/n)

(D) Mixing insurance & investment, is the biggest mistake. Insurance should be used for risk management & not investment management (14/n)

(i) Buying traditional Life Insurance (Endowment, Money Back, whole life etc) does nt give u adequate insurance cover. Insurance is generally 10 times of the premium. So if u r contributing 3L a year as premium, you are covered for roughly 30Lakhs, which may not be enough (15/n)

Avoid most traditional plans as neither do they cover u 4 insurance & nor r the returns worth investing 4. Don’t get carried away by the maturity figure & tax-free status. If u ever calculate the actual return in % terms, you will know the return is half of your inflation (16/n)

(ii) ULIP in most cases is an avoid. There are a few ULIPs with Zero premium allocation charge, Zero Policy admin charge which can be consider, specially for the tax free status upto 2,50,000 annual premium, But a big draw back is you compulsorily need to buy insurance. (17/n)

- Imagine paying 2,50,000 as premium but the entire amount not getting invested. If you are 30 years of age without any term insurance, this is okay. Out of 2,50,000, some premium will be allocated to term insurance giving you 25L cover and the remaining will be invested (18/n)

- But if you are 50 years old, a high mortality charge (term insurance premium) will be deducted towards insurance and hence the net investment will be much lower. (19/n)

- Or you already have insurance; this might not make sense because you will pay towards your term insurance in the ULIP when you might not need it, reducing your returns

Which is why, in most cases you can ignore ULIP’s as well. (20/n)

Which is why, in most cases you can ignore ULIP’s as well. (20/n)

(2) Lets discuss, Health Insurance now. A must to have!

- Make sure you mention all the necessary information while applying for the cover and not hide any material fact. Smoking, Alcohol, Pre-existing deceases etc. This is a major reason why most claims get rejected. (21/n)

- Make sure you mention all the necessary information while applying for the cover and not hide any material fact. Smoking, Alcohol, Pre-existing deceases etc. This is a major reason why most claims get rejected. (21/n)

- Don’t only rely on the employer 4 cover, u might need more

- In case of a claim, Mediclaim will nt settle 100% of the bill amount; there may be items, which the insurance is nt covering, & the same needs 2b paid by u. Have some medical fund in place 4 such contingencies (22/n)

- In case of a claim, Mediclaim will nt settle 100% of the bill amount; there may be items, which the insurance is nt covering, & the same needs 2b paid by u. Have some medical fund in place 4 such contingencies (22/n)

(3) Contingency Planning

- Make sure you have atleast 6-12 months of your monthly expenses, including you EMIs, kept aside in an liquid fund for any unforeseen eventuality (23/n)

- Make sure you have atleast 6-12 months of your monthly expenses, including you EMIs, kept aside in an liquid fund for any unforeseen eventuality (23/n)

(4) Goals

- Always have a goal in mind and define it in money terms, only then you can plan for it. Ex. Buying a house worth 2cr. in March 2030.

- Having a goal also brings in discipline in your investing (24/n)

- Always have a goal in mind and define it in money terms, only then you can plan for it. Ex. Buying a house worth 2cr. in March 2030.

- Having a goal also brings in discipline in your investing (24/n)

- While planning for the goal, keep in mind inflation. The value you may require for your goal may be much higher than the value of the same goal today.

- Keep you goals realistic (25/n)

- Keep you goals realistic (25/n)

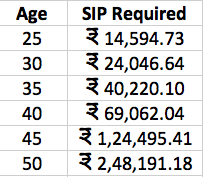

(5) Start investing as early as possible

-If u want to accumulate 5 cr. at retirement at 60, below is the SIP u will have 2do depending on when u start, assuming 10% returns

-Starting 10 years later will require u to do 40,000 instead of 14,500 to reach the same goal (26/n)

-If u want to accumulate 5 cr. at retirement at 60, below is the SIP u will have 2do depending on when u start, assuming 10% returns

-Starting 10 years later will require u to do 40,000 instead of 14,500 to reach the same goal (26/n)

(6) Investing thoughts

-Investing golden rule 30:30:30:10. Maximum 30% of ur income as EMI, 30% household expense, 30% Savings & 10% liquid

-Always maintain an Asset Allocation. Don’t invest most of what u have in 1 asset (27/n)

-Investing golden rule 30:30:30:10. Maximum 30% of ur income as EMI, 30% household expense, 30% Savings & 10% liquid

-Always maintain an Asset Allocation. Don’t invest most of what u have in 1 asset (27/n)

-Avoid investing in instruments you don’t understand and/or are complex.

-There is no get rich over night investing strategy. You will have to give it time

-Avoid looking at your portfolio value daily

-Save more (28/n)

-There is no get rich over night investing strategy. You will have to give it time

-Avoid looking at your portfolio value daily

-Save more (28/n)

(7) Equity Investing

- If you don’t understand stock picking, stick to MFs

- Equity is a long-term asset, invest for long term

- Avoid F&O if you don’t understand it

- Investing creates wealth not trading (29/n)

- If you don’t understand stock picking, stick to MFs

- Equity is a long-term asset, invest for long term

- Avoid F&O if you don’t understand it

- Investing creates wealth not trading (29/n)

(8) Fixed Income Investing

-Debt mutual funds are better over FD’s if you can avoid looking at the daily NAV and give it the 3-5 years you normally give your FDs

-Higher the interest rate offered, higher is the risk

-Fixed income is risk free is a misconception (30/n)

-Debt mutual funds are better over FD’s if you can avoid looking at the daily NAV and give it the 3-5 years you normally give your FDs

-Higher the interest rate offered, higher is the risk

-Fixed income is risk free is a misconception (30/n)

-Detailed insight on Fixed Income investing -

https://twitter.com/KirtanShahCFP/status/1329613707878432768?s=20(31/n)

(9) Real Estate

-Don’t consider the real estate u stay in as a portfolio investment, u will rarely b able 2 use it 2 convert 2 cash when u want it

-RE investments r extremely illiquid

-Rent you receive on housing RE investment is 2% vs 6-7% on commercial real estate (32/n)

-Don’t consider the real estate u stay in as a portfolio investment, u will rarely b able 2 use it 2 convert 2 cash when u want it

-RE investments r extremely illiquid

-Rent you receive on housing RE investment is 2% vs 6-7% on commercial real estate (32/n)

-Therotically, renting is a better option over buying a residential RE

-Interesting way to invest in RE -

-Interesting way to invest in RE -

https://twitter.com/KirtanShahCFP/status/1337588109484015617?s=20(33/n)

(10) Gold

-Don’t consider the Gold jewellery at home as investment if you are not going to sell it when the price increases. Its your emergency fund

-Investments in gold should be in bars and not jewellery. Why spend on making charges? (34/n)

-Don’t consider the Gold jewellery at home as investment if you are not going to sell it when the price increases. Its your emergency fund

-Investments in gold should be in bars and not jewellery. Why spend on making charges? (34/n)

-Best case, avoid physical gold and save yourself from GST, Fraud & Theft.

-Best way to invest in Gold is through Gold ETFs & SGB

-More about gold investing -

-Best way to invest in Gold is through Gold ETFs & SGB

-More about gold investing -

https://twitter.com/KirtanShahCFP/status/1327106086080417792?s=20(35/n)

(11) Tax Planning –

- Always try and utilize your 80C limits to the fullest. If you are in the 30% tax bracket, you directly save 1,50,000 * 30% = 45,000 of tax.

- 80C is no reason to invest in Insurance & 5 years bank FDs.

PPF, ELSS are much better options (36/n)

- Always try and utilize your 80C limits to the fullest. If you are in the 30% tax bracket, you directly save 1,50,000 * 30% = 45,000 of tax.

- 80C is no reason to invest in Insurance & 5 years bank FDs.

PPF, ELSS are much better options (36/n)

- Do tax planning & nt tax avoidance

- Cash that u generate by avoiding tax gets spent & does nt help u grow ur wealth. Its better 2 pay tax & invest the rest. Calculations show that in 3 years of investing, u recover the tax u paid & the investment can then keep growing(37/n)

- Cash that u generate by avoiding tax gets spent & does nt help u grow ur wealth. Its better 2 pay tax & invest the rest. Calculations show that in 3 years of investing, u recover the tax u paid & the investment can then keep growing(37/n)

- You can surely consider NPS. Have written about it in the past -

https://twitter.com/KirtanShahCFP/status/1331428570636247042?s=20(38/n)

(12) Debt Management

- It’s a blessing to be debt free

- Home loan, working capital loan kind of loans are okay but strictly avoid personal & credit card loans

- Don’t take loans & invest

& finally, have a will! (39/n)

- It’s a blessing to be debt free

- Home loan, working capital loan kind of loans are okay but strictly avoid personal & credit card loans

- Don’t take loans & invest

& finally, have a will! (39/n)

Read our detailed blog by @stepbystep888 on this topic for some very insightful learnings.

Link - fpa.edu.in/blog/personal-… (40/n)

Link - fpa.edu.in/blog/personal-… (40/n)

We have written multiple threads earlier on

- Sector Analysis

- Macro Economics

- Debt Markets

- Real Estate

- Equity Markets etc.

You can find them all in the link below. Do hit the re-tweet & help us reach a larger audience

- Sector Analysis

- Macro Economics

- Debt Markets

- Real Estate

- Equity Markets etc.

You can find them all in the link below. Do hit the re-tweet & help us reach a larger audience

https://twitter.com/KirtanShahCFP/status/1337953717274832896?s=20(**END**)

• • •

Missing some Tweet in this thread? You can try to

force a refresh