1/8 What does almost two centuries of data tell us about #ukhousing affordability? Here’s a chart-thread of my research which @martinwolf_ covered in his latest @FT piece.

Full article here: schroders.com/en/uk/private-…

#houseprices #property

Full article here: schroders.com/en/uk/private-…

#houseprices #property

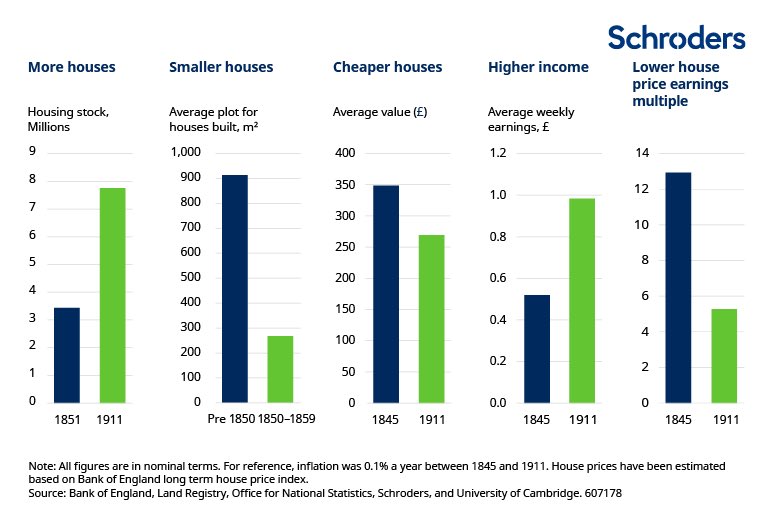

2/8 UK homes have only been this expensive vs earnings twice in the past 120 years.

Things were even more expensive between the year 1845 and early 20th century.

What happened to change things? More houses, smaller houses, higher incomes.

Things were even more expensive between the year 1845 and early 20th century.

What happened to change things? More houses, smaller houses, higher incomes.

3/8 most people didn’t really benefit though, as over 75% rented at that time. Home ownership didn’t take off until 2nd half of 20th century.

Note the reversal post-2001. Back down near 64% now. Home ownership becoming less attainable

Note the reversal post-2001. Back down near 64% now. Home ownership becoming less attainable

4/8 housebuilding peaked in 1950-70s, although also peak time for slum clearance.

@Conservatives manifesto pledge for 300,000 new homes per year has not been seen since 1970s.

@Conservatives manifesto pledge for 300,000 new homes per year has not been seen since 1970s.

5/8 Big shifts in who has built houses. Private sector post-WW1, public sector post-WW2, private sector last 40yrs.

@martinwolf_ argues we need a bigger role for public sector going forwards. A return to council housing?

#SocialHousing

@martinwolf_ argues we need a bigger role for public sector going forwards. A return to council housing?

#SocialHousing

6/8 Massive regional variation.

Average London house costs over 11x average wage, midlands~6.5x, North of England~6x, Scotland 4.7x.

Regional divergence a relatively recent phenomenon. Didn’t exist to much extent pre-2000

Average London house costs over 11x average wage, midlands~6.5x, North of England~6x, Scotland 4.7x.

Regional divergence a relatively recent phenomenon. Didn’t exist to much extent pre-2000

7/8 #genderpaygap results in gender housing affordability gap.

Average London house costs over 13x average woman’s income.

#genderequality

Average London house costs over 13x average woman’s income.

#genderequality

• • •

Missing some Tweet in this thread? You can try to

force a refresh