Precious metals are a disappointment to the investment community.

Cryptocurrencies have stolen the attention, gold's centuries of history all but forgotten & the business news anchors laugh at metals.

For contrarians, it's probably a good time to start paying attention.

Cryptocurrencies have stolen the attention, gold's centuries of history all but forgotten & the business news anchors laugh at metals.

For contrarians, it's probably a good time to start paying attention.

Everyone has their own view on this asset class.

There is a die-hard Goldbugs camp, there is also a lot of hate towards Gold, plus everything in between.

Gold has become very much disliked in the West, while countries like China & India have a strong tradition towards it.

There is a die-hard Goldbugs camp, there is also a lot of hate towards Gold, plus everything in between.

Gold has become very much disliked in the West, while countries like China & India have a strong tradition towards it.

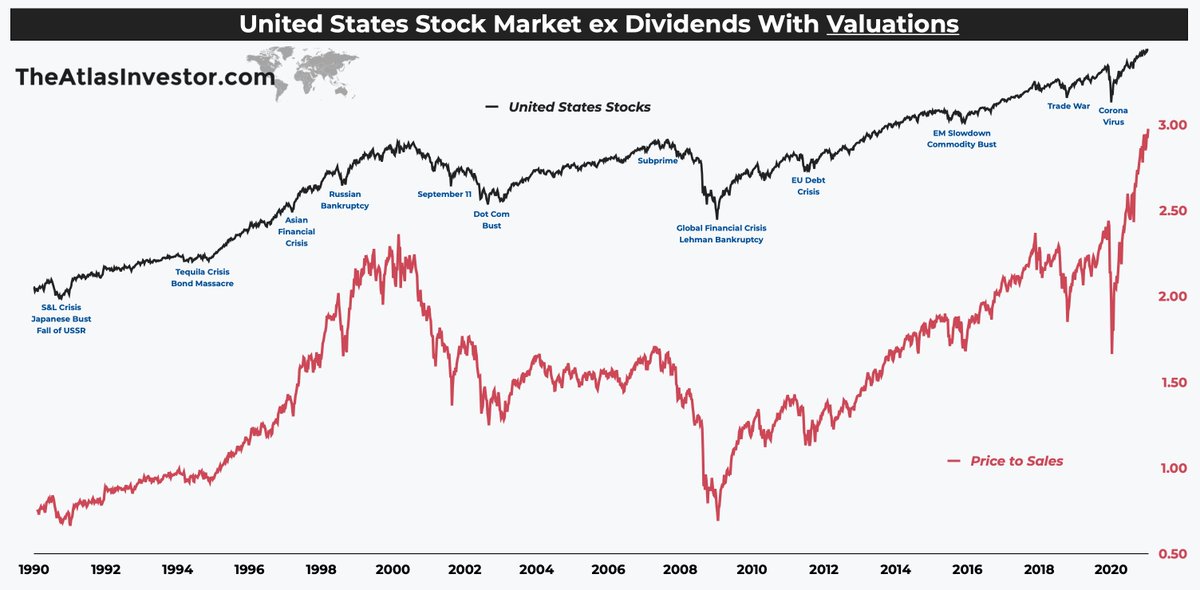

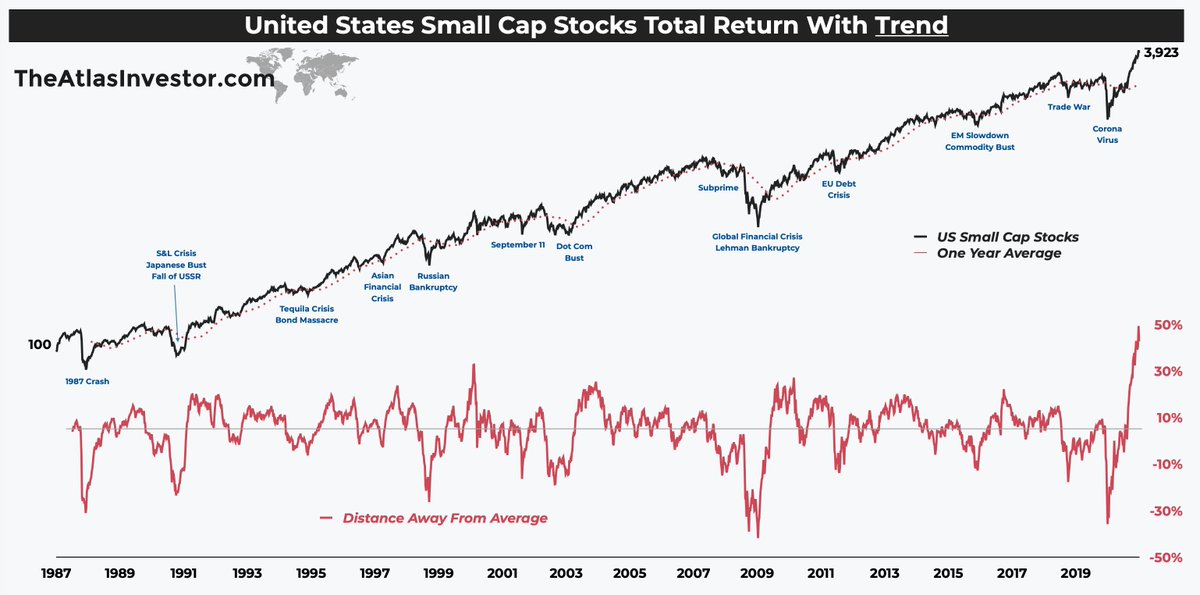

Gold floated in the early 1970s, but my chart starts in 1988 — cutting out the 70s is maybe not a fair way to measure its performance.

Regardless, it should be clear that Gold has had periods of very strong returns (25% CAGR over a decade) as well as disappointing periods.

Regardless, it should be clear that Gold has had periods of very strong returns (25% CAGR over a decade) as well as disappointing periods.

Our own opinion on precious metals are:

• as a non-income producing asset, Gold isn't really an attractive buy&hold strategy

• every portfolio should carry some Gold, not as an investment, but as an insurance policy with a proven 5,000-year historical track record

• as a non-income producing asset, Gold isn't really an attractive buy&hold strategy

• every portfolio should carry some Gold, not as an investment, but as an insurance policy with a proven 5,000-year historical track record

• for those with the ability to time things better than others, Gold can offer incredible returns over 5 or even 10 year periods

• Gold is very much uncorrelated to other classic & traditional asset classes such as stocks, government bonds, credit & a great hedge vs cash

• Gold is very much uncorrelated to other classic & traditional asset classes such as stocks, government bonds, credit & a great hedge vs cash

• as a family office, we are very much disconnected from Wall Street's non-sense advice and caution against holding only West-centric views

• instead, we focus on global investing & sympathize (to a degree) with traditions of owning Gold as a proven insurance policy

• instead, we focus on global investing & sympathize (to a degree) with traditions of owning Gold as a proven insurance policy

Is Gold and the precious metals sector an easy asset class to invest in?

No, definitely not.

One can easily observe that the Gold Mining index, popular with Gold bugs, has not made any progress over the last 4 decades.

No, definitely not.

One can easily observe that the Gold Mining index, popular with Gold bugs, has not made any progress over the last 4 decades.

But one should also observe Gold Miners recorded one of the best 5-year returns — compounding at 30% CAGR.

Miners outperformed the S&P, Small Caps, Emerging Markets, Dow Jones, any real estate GP & any mezzanine debt deal.

And even the mighty Nasdaq 100!

#buylowsellhigh

Miners outperformed the S&P, Small Caps, Emerging Markets, Dow Jones, any real estate GP & any mezzanine debt deal.

And even the mighty Nasdaq 100!

#buylowsellhigh

• • •

Missing some Tweet in this thread? You can try to

force a refresh