President Biden's #AmericanJobsPlan looks to increase the federal corporate tax rate to 28%, which would raise the U.S. federal-state combined tax rate to 32.34%, higher than every country in the OECD, the G7, and all our major trade partners and competitors including China.

While President Biden’s #AmericanJobsPlan emphasizes making goods in America, the tax increases will raise the cost of production in the U.S, erode American competitiveness, and slow our economic recovery.

taxfoundation.org/biden-infrastr… #StateOfTheUnion

taxfoundation.org/biden-infrastr… #StateOfTheUnion

According to Congressional Budget Office and Tax Foundation modeling, tax increases on corporations are among the most harmful options to pay for the increased spending.

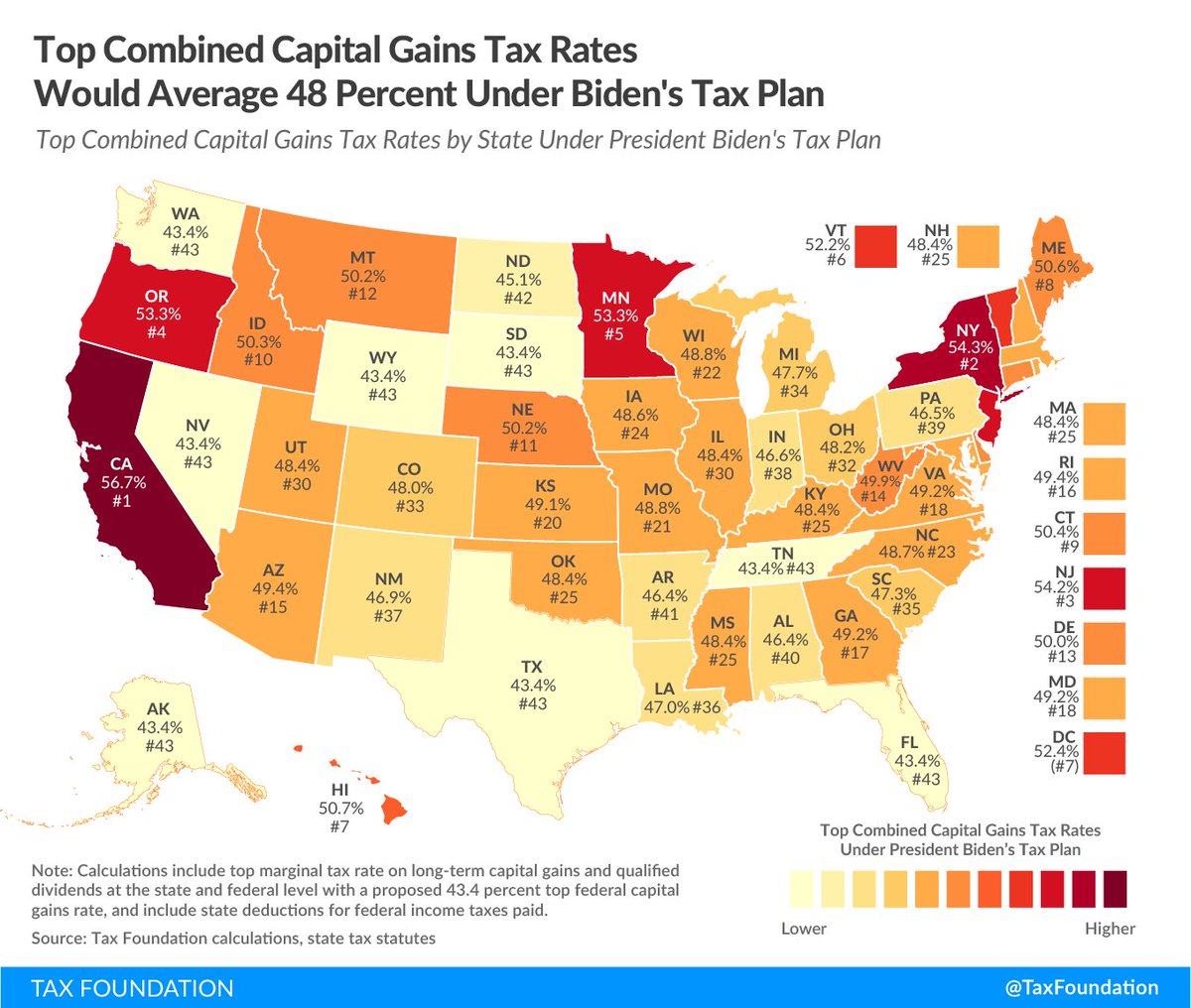

bit.ly/3uqbTSs #StateOfTheUnion #JointAddress

bit.ly/3uqbTSs #StateOfTheUnion #JointAddress

Raising corporate income taxes would put the U.S. at a competitive disadvantage, whether one looks at statutory tax rates or effective corporate tax rates.

taxfoundation.org/us-effective-c…

taxfoundation.org/us-effective-c…

While the focus has been on the proposed 28 percent federal corporate tax rate, it's important to include state tax rates when thinking about the total tax burden on corporate income: taxfoundation.org/combined-corpo…

Corporate income taxes are one of the most harmful ways to raise revenue.

They place a higher burden on investment, reduce economic output, and reduce after-tax incomes across the income spectrum—negative economic effects that compound over time: taxfoundation.org/increase-corpo…

They place a higher burden on investment, reduce economic output, and reduce after-tax incomes across the income spectrum—negative economic effects that compound over time: taxfoundation.org/increase-corpo…

• • •

Missing some Tweet in this thread? You can try to

force a refresh