UI Path: A company on a mission to fully automate the modern enterprise and take away your jobs.

This is a thread that breaks down everything about $PATH's business.

What truly makes them unique? - I'll cover both the Bull and Bear Case and everything you need to know here:

This is a thread that breaks down everything about $PATH's business.

What truly makes them unique? - I'll cover both the Bull and Bear Case and everything you need to know here:

1/ Introduction - Problem:

In your workplace do you feel like you've got one or two mundane/repetitive tasks that bores you?

Despite digital Innovation, today’s enterprise is filled with many mundane tasks that saps productivity. Some big examples include Email, fillings etc.

In your workplace do you feel like you've got one or two mundane/repetitive tasks that bores you?

Despite digital Innovation, today’s enterprise is filled with many mundane tasks that saps productivity. Some big examples include Email, fillings etc.

2/ Welcome to RPA:

The problems highlighted above led to the rise of the RPA industry.

RPA is basically the automation layer that sits on top of other software products that allows companies or workers to automate repetitive tasks by replicating the steps a knowledge worker.

The problems highlighted above led to the rise of the RPA industry.

RPA is basically the automation layer that sits on top of other software products that allows companies or workers to automate repetitive tasks by replicating the steps a knowledge worker.

3/ $PATH Overview:

UI Path is an enterprise company that aims to use bots & robots that emulate humans to fully automate these mundane tasks in the enterprise.

Eg. They automate logging into applications, extracting information from docs, moving folders, easy finance tasks etc

UI Path is an enterprise company that aims to use bots & robots that emulate humans to fully automate these mundane tasks in the enterprise.

Eg. They automate logging into applications, extracting information from docs, moving folders, easy finance tasks etc

4/ How it works?

You install a no-code bot on your desktop thru the workday that records all your tasks. The robot uses computer vision that can see and monitor all your tasks then learns it.

Eventually when executed, this bot can click and move things like a human would do.

You install a no-code bot on your desktop thru the workday that records all your tasks. The robot uses computer vision that can see and monitor all your tasks then learns it.

Eventually when executed, this bot can click and move things like a human would do.

5/ $PATH 4-Product Types:

i) Discover: When installed, it can help discover automation opportunities within your workday.

ii) Build: Next, once a process is identified, business users can install UI Path to automate a manual process - through an unattended or attended robot

i) Discover: When installed, it can help discover automation opportunities within your workday.

ii) Build: Next, once a process is identified, business users can install UI Path to automate a manual process - through an unattended or attended robot

6/

iii) Run product: It can be executed across department and software systems

iv) Manage: Automation deployed. Users can manage & track automation activities to ensure its going according to plan.

There is a big integration across systems that UI Path utilizes and is a moat. :

iii) Run product: It can be executed across department and software systems

iv) Manage: Automation deployed. Users can manage & track automation activities to ensure its going according to plan.

There is a big integration across systems that UI Path utilizes and is a moat. :

7/ $PATH Marketplace

v) Engage: They run a marketplace. Multiple users internal or external within an industry can access & collaborate on d platform.

Eg. JPM can see a process used by Goldman and implement it internally.

This marketplace presents a network effect & data moat

v) Engage: They run a marketplace. Multiple users internal or external within an industry can access & collaborate on d platform.

Eg. JPM can see a process used by Goldman and implement it internally.

This marketplace presents a network effect & data moat

8/ Tech & Business Partners below:

Consulting firms help organizations w. business process outsourcing. This involves assessing an org. system, processes to develop strategies to optimize efficiency.

$PATH's uses tech partners for integrations and has a strong tech ecosystem.

Consulting firms help organizations w. business process outsourcing. This involves assessing an org. system, processes to develop strategies to optimize efficiency.

$PATH's uses tech partners for integrations and has a strong tech ecosystem.

9/ $PATH Clients - Let's look at Customers (a):

80% of Fortune 10

70% of Fortune 100

60% of Fortune 500.

They dominate Corporate America across multiple industries and sectors.

Just the widespread applicability across multiple verticals of their software is a major strength.

80% of Fortune 10

70% of Fortune 100

60% of Fortune 500.

They dominate Corporate America across multiple industries and sectors.

Just the widespread applicability across multiple verticals of their software is a major strength.

10/ Customers (b)

In general, they have:

+ Total Customers- 8500+

+ Customers w. ARR > 100K, at 1104!

+ Customers w. ARR > $1M, at 104!

And,

+ They have a DB-Net Retention rate at 145% !

In general, they have a highly diversified base with happy customers who keep using it.

In general, they have:

+ Total Customers- 8500+

+ Customers w. ARR > 100K, at 1104!

+ Customers w. ARR > $1M, at 104!

And,

+ They have a DB-Net Retention rate at 145% !

In general, they have a highly diversified base with happy customers who keep using it.

11/ Financials - Top-line:

+ 79% YoY CAGR In AR-Revenue (ARR is a big way they measure the business due to their contract agreements)

+ 80% YoY CAGR in Revenue Growth and recently 65% YoY.

There is a slow-down this year, but they overall, $PATH is rapidly growing!

+ 79% YoY CAGR In AR-Revenue (ARR is a big way they measure the business due to their contract agreements)

+ 80% YoY CAGR in Revenue Growth and recently 65% YoY.

There is a slow-down this year, but they overall, $PATH is rapidly growing!

12/ Financials - Bottom-line:

+ 88% Gross Margins (!!)

+ Signs of operating leverage

+ GAAP Profitable, but IPO SBC expenses changed things

+ N-GAAP Ops Margin: 9%

+ EBITDA: Improved in 2020 but going high due to S&M / R&D (which is ok IMO)

+ FCF: -11%

+ No debt

+ Cash: $1.9B

+ 88% Gross Margins (!!)

+ Signs of operating leverage

+ GAAP Profitable, but IPO SBC expenses changed things

+ N-GAAP Ops Margin: 9%

+ EBITDA: Improved in 2020 but going high due to S&M / R&D (which is ok IMO)

+ FCF: -11%

+ No debt

+ Cash: $1.9B

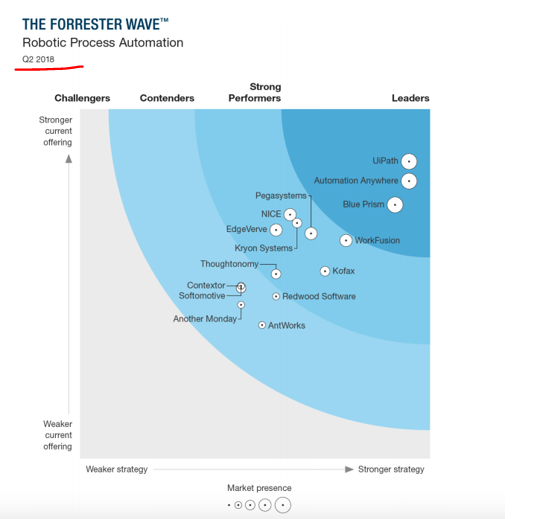

13/ Market Leader on Industry Product Reviews:

Forrester ranks UI Path as 1st:

Let's look at their journey

+ Among 14 vendors, $PATH earned the highest rank in Current Offering, Strategy, & Market Presence

+ Highest scores in product vision, performance & partner ecosystem.

Forrester ranks UI Path as 1st:

Let's look at their journey

+ Among 14 vendors, $PATH earned the highest rank in Current Offering, Strategy, & Market Presence

+ Highest scores in product vision, performance & partner ecosystem.

14/ Gartner Reviews also ranks them 1st and the leader in the space.

Another 1st on Tues. this week -> ir.uipath.com/news/detail/16…

I could continue on and on, but its clear UI Path is the leader of the RPA space and its not close yet

This point is crucial for my next point.. TAM.

Another 1st on Tues. this week -> ir.uipath.com/news/detail/16…

I could continue on and on, but its clear UI Path is the leader of the RPA space and its not close yet

This point is crucial for my next point.. TAM.

15/ TAM:

TAM can be vague, but the potential to automate a TON of manual tasks is huge!

They have expanded the TAM from $7B to $60B. They did it with their new SaaS, AI product offerings and some acquisitions.

Now consider a 60B+ TAM + Being the industry leader = POTENTIAL!

TAM can be vague, but the potential to automate a TON of manual tasks is huge!

They have expanded the TAM from $7B to $60B. They did it with their new SaaS, AI product offerings and some acquisitions.

Now consider a 60B+ TAM + Being the industry leader = POTENTIAL!

16/ Let talk Risks:

a) The big risk to UI Path is not valuation, but the transition to the cloud by corporations.

UI Path's product was built to work very well in a company with legacy systems like SAP, Oracle etc.

To mitigate it, they have expanded their SaaS offerings below:

a) The big risk to UI Path is not valuation, but the transition to the cloud by corporations.

UI Path's product was built to work very well in a company with legacy systems like SAP, Oracle etc.

To mitigate it, they have expanded their SaaS offerings below:

17/ Risks-b: Competitors:

i) Automation Anywhere(Strong)

ii) Blue Prism (Weak)

Path is differentiated on:

a) Vast marketplace data

b) Most comprehensive product suite in RPA

c) Product Tech is better as ranked by Gartner & Customer reviews

d) $PATH growth metrics > Competitors

i) Automation Anywhere(Strong)

ii) Blue Prism (Weak)

Path is differentiated on:

a) Vast marketplace data

b) Most comprehensive product suite in RPA

c) Product Tech is better as ranked by Gartner & Customer reviews

d) $PATH growth metrics > Competitors

18/ Risks:

c) Microsoft: Recently $MSFT launched some cheap RPA tools on the market. This may pose pricing pressure.

Based on product offerings, $MSFT RPA tools cover more niche automation tools. However, PATH has a more comprehensive product that covers advanced RPA areas now.

c) Microsoft: Recently $MSFT launched some cheap RPA tools on the market. This may pose pricing pressure.

Based on product offerings, $MSFT RPA tools cover more niche automation tools. However, PATH has a more comprehensive product that covers advanced RPA areas now.

19/

d) Potential Disruptors: Upcoming start-ups focused on very niche and vertical areas of the RPA market like Olive AI for healthcare.

But, $PATH is the leader on every level and based on their cash (1.9B) and access to Fortune 500, they are positioned to control the market.

d) Potential Disruptors: Upcoming start-ups focused on very niche and vertical areas of the RPA market like Olive AI for healthcare.

But, $PATH is the leader on every level and based on their cash (1.9B) and access to Fortune 500, they are positioned to control the market.

20/ Mgmt Team:

Daniel Dines, Founder. Romanian w. a great American dream story.

After watching multiple of his interviews, he is not your typical silicon valley CEO. A very interesting techie at heart.

In 2019, they had a mgmt revamp w. new execs. Culture preaches humility.

Daniel Dines, Founder. Romanian w. a great American dream story.

After watching multiple of his interviews, he is not your typical silicon valley CEO. A very interesting techie at heart.

In 2019, they had a mgmt revamp w. new execs. Culture preaches humility.

21/ Dan went thru ALOT of struggles for over 10-years since he founded DeskOver in 2005 (turned into UI Path). The big turning point came in 2015 w. Funding + Product pivot

He is a CEO who is 'results' driven and doesn't mess around. I actually like that! The results are proof!

He is a CEO who is 'results' driven and doesn't mess around. I actually like that! The results are proof!

END/

22/ My Investing Process: Many have wondered why I invested into $PATH despite on its valuation.

I started a small position & plan to DCA overtime.

But, this is a 5-star business that meets all metrics on Tech, GTM and Financials. Rare breed that will always be expensive.

22/ My Investing Process: Many have wondered why I invested into $PATH despite on its valuation.

I started a small position & plan to DCA overtime.

But, this is a 5-star business that meets all metrics on Tech, GTM and Financials. Rare breed that will always be expensive.

23/ Let me summarize this thread in conclusion:

I'll start w. risks to continue monitor:

i) Revenue vs Costs as they ramp up their Cloud & AI offerings

ii) Maybe a continued revenue deceleration?

iii) Competitive landscape to see if they can maintain leadership in new RPA areas

I'll start w. risks to continue monitor:

i) Revenue vs Costs as they ramp up their Cloud & AI offerings

ii) Maybe a continued revenue deceleration?

iii) Competitive landscape to see if they can maintain leadership in new RPA areas

24/ Summary:

i) Comprehensive product suite across d. entire RPA ecosystem

ii) Diversified & large Market share amongst Fortune 500

iii) Customers love the product, Proof is record DBNER

iv) High switching costs, best tech combined w. best ease of use leading to high stickiness

i) Comprehensive product suite across d. entire RPA ecosystem

ii) Diversified & large Market share amongst Fortune 500

iii) Customers love the product, Proof is record DBNER

iv) High switching costs, best tech combined w. best ease of use leading to high stickiness

25/

v) 1st Class Financials- Both on top & bottom line (Top 1% in SaaS)

vi) Clear market leader by market share & as ranked by Industry Research like Gartner.

Hence, Market Leadership + TAM >> positions them to capture a large piece of the 60B+ TAM = long-run growth potential.

v) 1st Class Financials- Both on top & bottom line (Top 1% in SaaS)

vi) Clear market leader by market share & as ranked by Industry Research like Gartner.

Hence, Market Leadership + TAM >> positions them to capture a large piece of the 60B+ TAM = long-run growth potential.

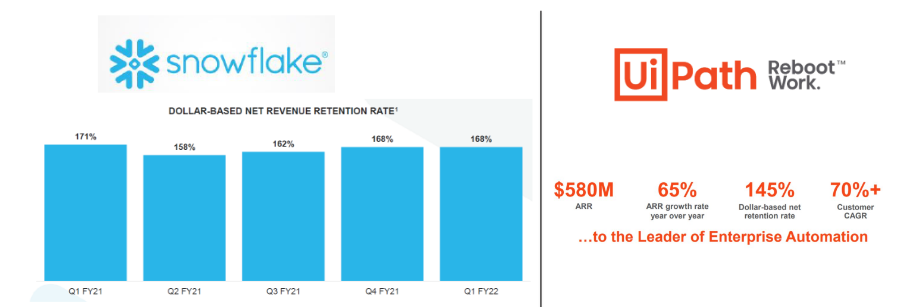

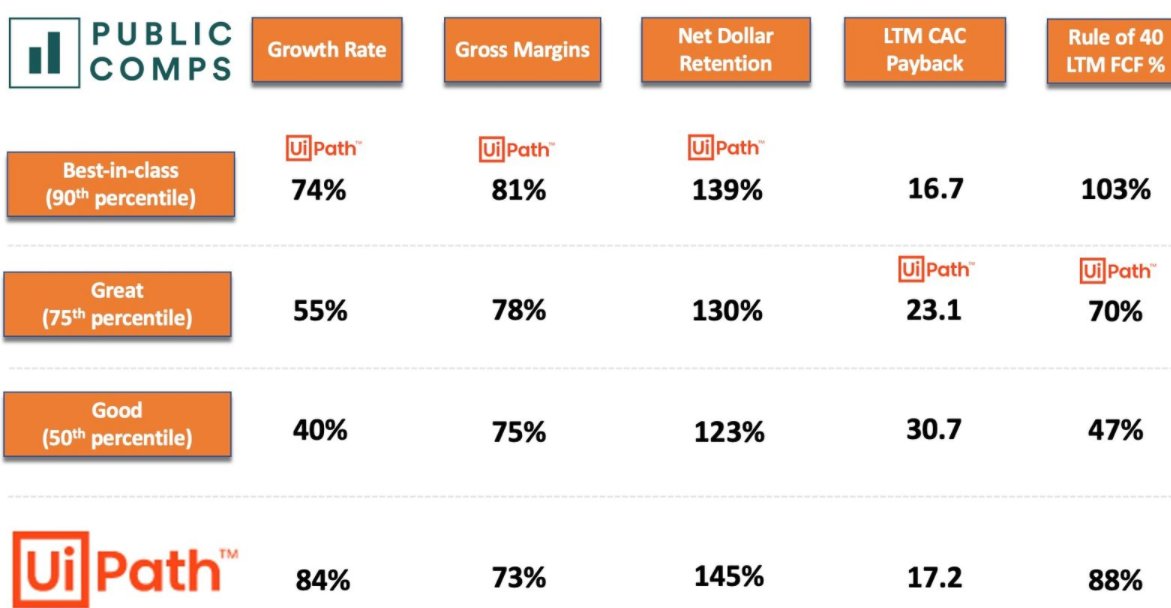

26/

This pre Q1 earnings data by @publiccomps summarizes my investing decision and why I believe $PATH will not be 'cheap'

I believe w. the rise of new SaaS B-Models since 2009 like $SNOW etc. Traditional valuation metric will not be as effective as they have been in the past.

:

This pre Q1 earnings data by @publiccomps summarizes my investing decision and why I believe $PATH will not be 'cheap'

I believe w. the rise of new SaaS B-Models since 2009 like $SNOW etc. Traditional valuation metric will not be as effective as they have been in the past.

:

27/ And let's be honest. The future of work for the enterprise is moving towards automating tedious/manual tasks. This will allow for more productivity.

UI Path is currently well positioned to capture this opportunity. This explains some of the reason for its premium valuation.

UI Path is currently well positioned to capture this opportunity. This explains some of the reason for its premium valuation.

28/28 This thread is v. long, so I'm hoping to put everything in a cohesive format into my newsletter (and some highlights from Snowflake) by next week investianalystnewsletter.substack.com/welcome

This is my longest thread. If you are still with me, hope this was helpful! Thank you! @InvestiAnalyst

This is my longest thread. If you are still with me, hope this was helpful! Thank you! @InvestiAnalyst

• • •

Missing some Tweet in this thread? You can try to

force a refresh