Brief thread to look at the damage that the FOMC meeting did to market expectations and the market outlook for the US economy.

Most people point to the sharp decline in 5Y fwd breakevens, which were approaching better levels and now are sinking. Yes, but there is more. 1/6

Most people point to the sharp decline in 5Y fwd breakevens, which were approaching better levels and now are sinking. Yes, but there is more. 1/6

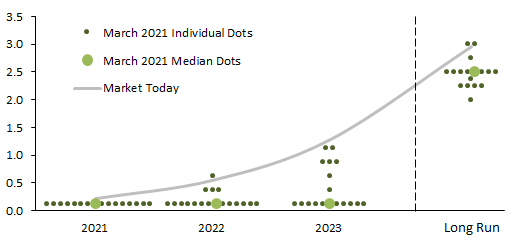

The market is 100% buying that the Fed will raise rates sooner and faster than previously thought (it always did, and even more so after the FOMC). Look at the higher expected trajectory for the FFR for the first four years. 2/6

But, looking again at the chart in the previous tweet, expectations five yrs ahead and beyond have moved *down*. The market thinks that, by being preemptive, the Fed won’t need to hike as much later. Basically, the market thinks the Fed has already abandoned FAIT. 3/6

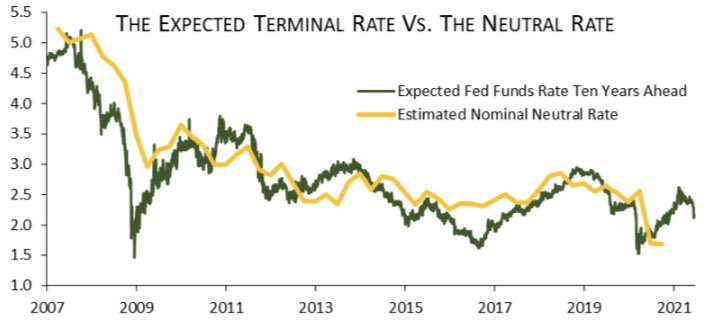

It gets worse. The expected FFR many years ahead is a proxy for the market view of where the nominal neutral rate is headed. That proxy has sunk since Wednesday. Only during the GFC and at the onset of Covid has that expectation dropped more over a three-day period. 4/6

So, before Wednesday the market was hopeful that the combination of expansive fiscal and monetary policies (including FAIT) would lift nominal neutral rate (i.e., better long-term prospects for the economy). Now that’s gone. The mkt thinks we are one step closer to Japan. 5/6

I don’t think the FOMC has abandoned FAIT. I think it was a communication problem. The f’cst, the dots, and the tapering attitude don’t mesh well with each other. That has confused mkts and given the impression of retreat from FAIT. I hope Powell and Williams will clarify. 6/6

• • •

Missing some Tweet in this thread? You can try to

force a refresh