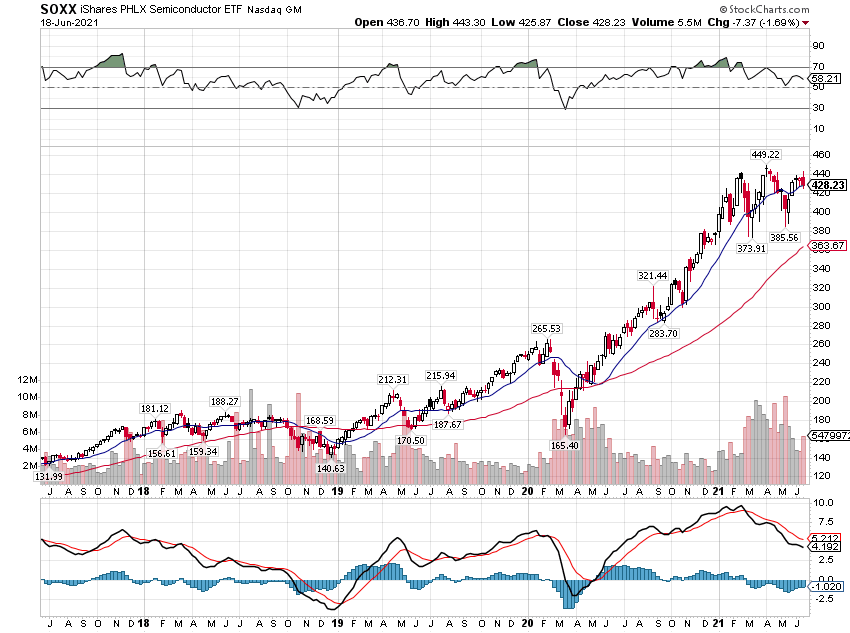

A bit late with this one. RIP David Swensen.

Had an enormous influence on me, helping me to step outside of public securities "tunnel vision" many years ago and diversify with alternative assets.

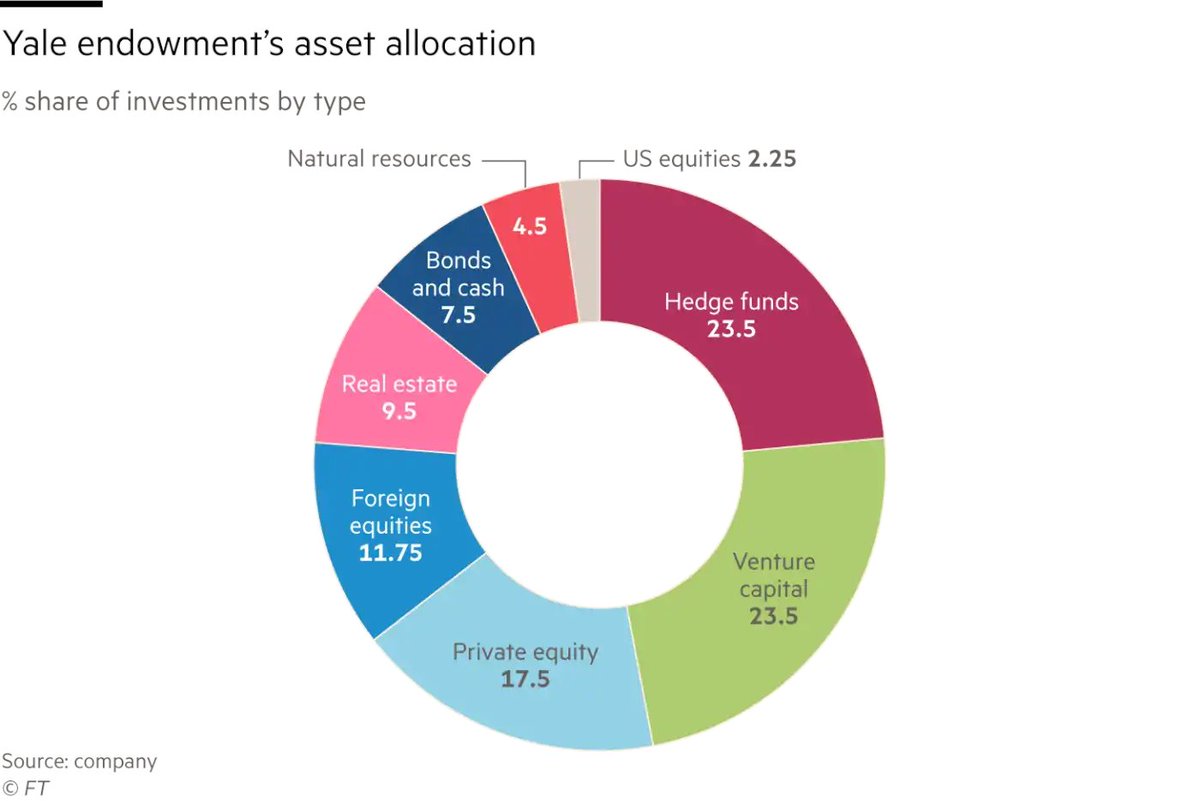

The Yale model changed the way private money allocates.

ft.com/content/e43825…

Had an enormous influence on me, helping me to step outside of public securities "tunnel vision" many years ago and diversify with alternative assets.

The Yale model changed the way private money allocates.

ft.com/content/e43825…

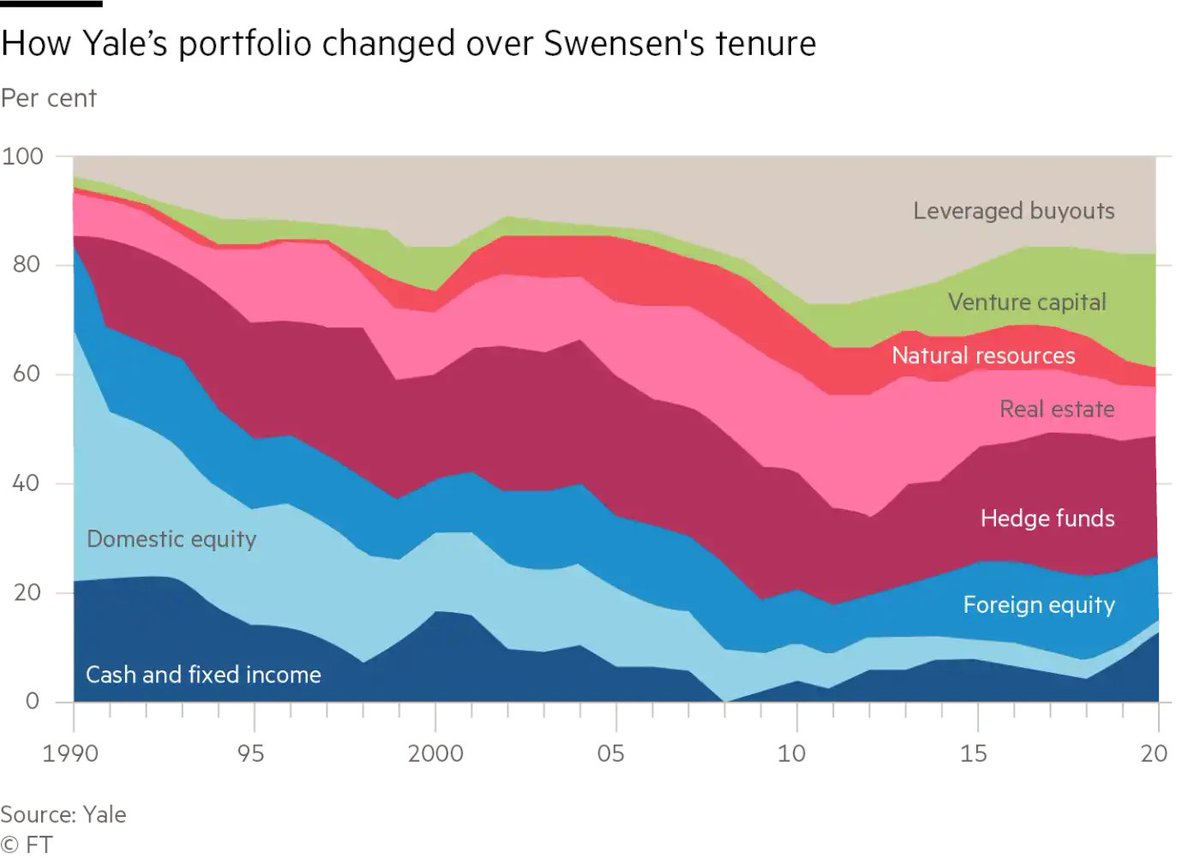

Swensen's portfolio allocation weighting over the years.

"Mr. Swensen often blasted the excessive costs of the mutual-fund industry and the conflicts of interest on Wall Street. He bashed activist investors as value-destroying and asset-gathering managers as out for themselves."

"Mr. Swensen espoused the then-radical idea that institutional investors should de-emphasize stocks & bonds.

Investors should instead take advantage of their long time horizons to invest in hedge funds, real estate & other alternative investments, the Yale model said."

Investors should instead take advantage of their long time horizons to invest in hedge funds, real estate & other alternative investments, the Yale model said."

• • •

Missing some Tweet in this thread? You can try to

force a refresh