My analysis of the jobs numbers, with Willie Powell. Short version: the pace of job growth picked up as signs continue to point to a tight labor market. A 🧵follows.

piie.com/blogs/realtime…

piie.com/blogs/realtime…

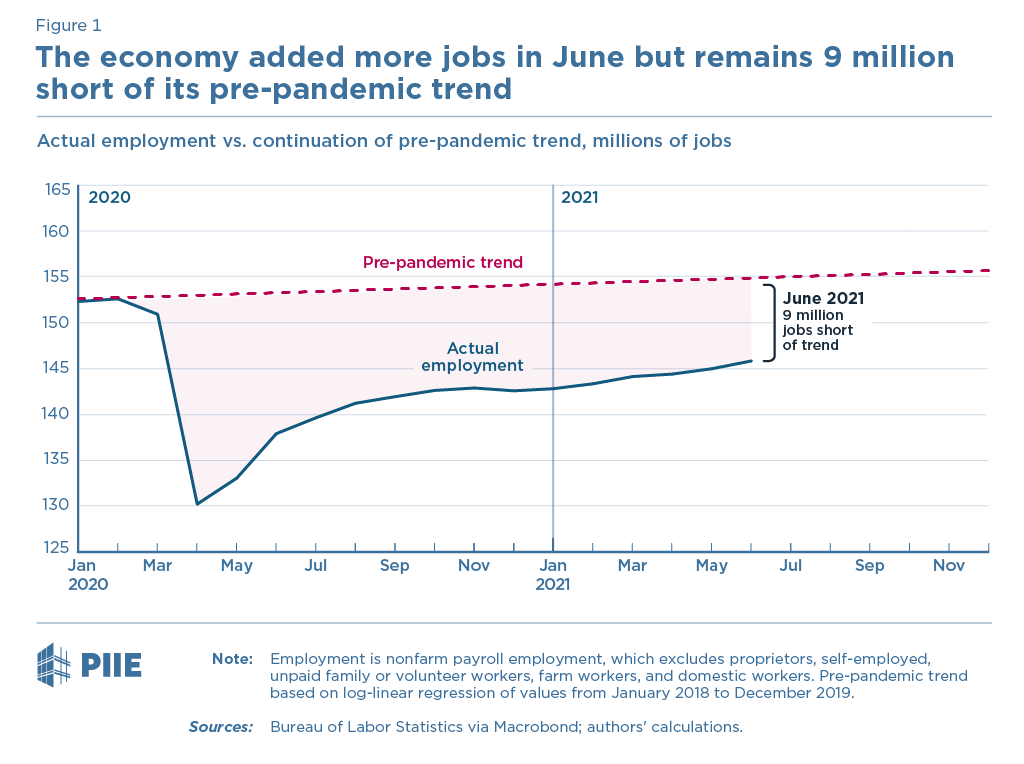

850,000 was a great jobs number but we're still 9m jobs short of trend. We should be able to narrow that gap relatively rapidly for several more months in a row (assuming no dramatic worsening of the virus situation).

The unemployment rate remains elevated. And the "realistic" unemployment rate, which includes the 2.1m people who have left the labor force above and beyond what one would have expected.

One factor holding down job growth in recent months has been that only ~24 percent of unemployed workers have taken jobs per month. It should be more like 29-34 percent. In some ways that is good news, shows much more room before we hit a "speed limit". piie.com/blogs/realtime…

Overall despite the shortfalls the labor market looks like one that is more constrained by labor supply than by labor demand--which is to say, it's a tight labor market. You can see that in openings which now exceed the number of unemployed.

The tightness in most evident in the rapid pace of *nominal* wage growth. Wage growth slowed a little in June but has still been running at a 6%+ nominal rate over the last three months. That is much faster than normal. More on that in this earlier thread.

https://twitter.com/jasonfurman/status/1410969170716643328?s=20

Going forward the two big questions are:

1. Labor supply and labor demand should both continue to increase, but what pace and what relative magnitude?

2. Do we get all 9m jobs back?

FIN

1. Labor supply and labor demand should both continue to increase, but what pace and what relative magnitude?

2. Do we get all 9m jobs back?

FIN

• • •

Missing some Tweet in this thread? You can try to

force a refresh