Can crude really touch $100/bbl?. After initial commentary globally around the probability of $100/barrel on crude, the narrative appears to be moderating a bit. The global oil market that was in a surplus of 2mn barrels per day (mbpd) in 2020 and turned into a...(1/6)

...deficit of (1.6)mbpd during the first six months of this year 2021. This deficit is an artificial one, on account of the production cuts imposed by the OPEC+ to keep prices elevated. Commentators appear to increasingly feel that crude could peak around $80/bbl. Higher...(2/6)

...spare capacities and the attractiveness of selling at elevated crude prices on the one hand could lead to an increase in supply on the sidelines. On the other hand, experts see a realistic possibility of Iranian crude resumption by the end of this year. While...(3/6)

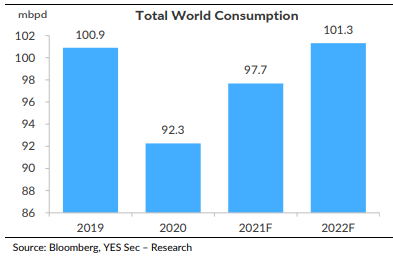

...the recent price rise is largely on the back of planned supply cuts, demand is also on the rise. However, the demand pickup is more on the back of depressed demand and therefore the . Global oil demand for 2021 is broadly seen at 3mbpd below what was seen in...(4/6)

...2019. With supply curbs in place, some commentators see the demand-supply deficit at 0.8mbpd. There is now a focus on the infections curve, possibility of Iran oil resumption and the likelihood of a shale resumption, if crude staying higher for longer...(5/6)

...($60/bbl is the shale breakeven). In addition, against the 0.8mbpd deficit, spare production is at a record high of 7mbpd. Viewed against all of the above, $100/bbl appears a stretch for now.(6/6)

Charts from Yes Securities' comprehensive report Oil-nomics.

Charts from Yes Securities' comprehensive report Oil-nomics.

• • •

Missing some Tweet in this thread? You can try to

force a refresh