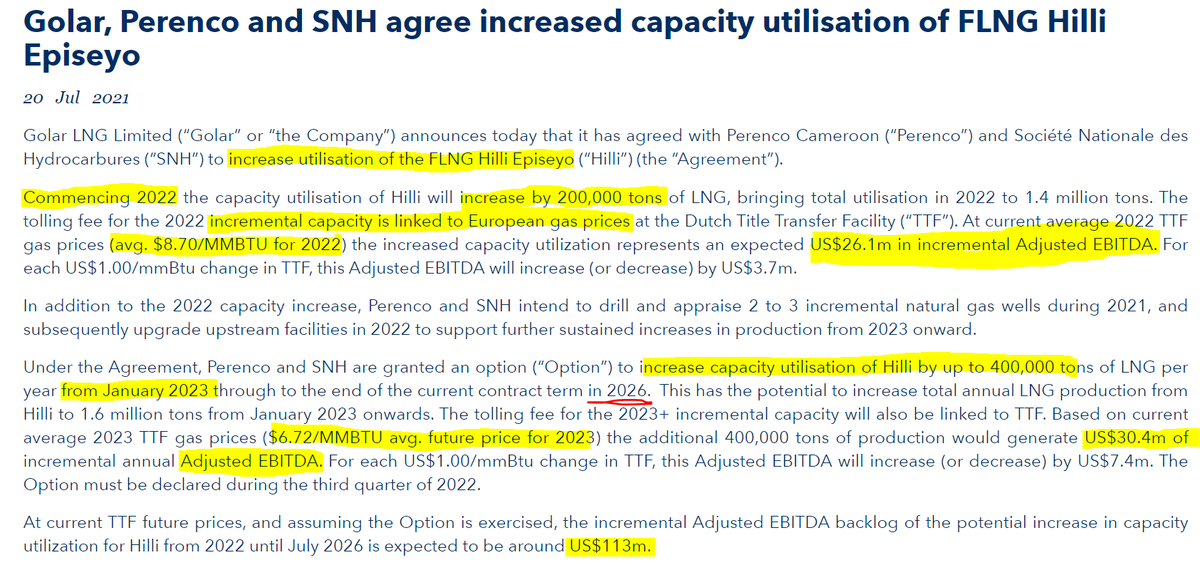

My thoughts on Pax Global: Amazing results proving once again that the business isn't commodity generating 20% ROEs and >50% ROCEs.

Pax is leading the Android terminal transition with 35% total revenue coming from APOS and expected to be >70% in four years

Pax is leading the Android terminal transition with 35% total revenue coming from APOS and expected to be >70% in four years

APAC grew 23% despite COVID issues. India is the biggest country and Pax is the market leader. Paytm (supported by Alibaba) and Pinelabs (Pax customers) looking for IPO which would accelerate their growth. Do you remember the impact of Pagseguro and Stone IPOs on Pax in 2018?

Big customers asking for Pax solutions in Europe and USCA. Gaining market share to Ingenico and Verifone due to its superior product portfolio. I expect Pax keeping amazing growth for years. Pax market share is 10% and they plan to double it in the next 4 years (Ingenico 25%)

LACIS. Growing strongly (+17% yoy) despite COVID, forex and being the market leader by far. Customers (Pagseguro, Stone, Mercadopago) highly optimistic on future prospects. LATAM still highly underpenetrated!! Cashless trend can't stop!

Saas Business grew 320%. PAXSTORE is the largest platform despite Pax is not promoting it with aggressive discounts. We received really good feedback from customers. The platform is providing unique value and huge volume will follow.

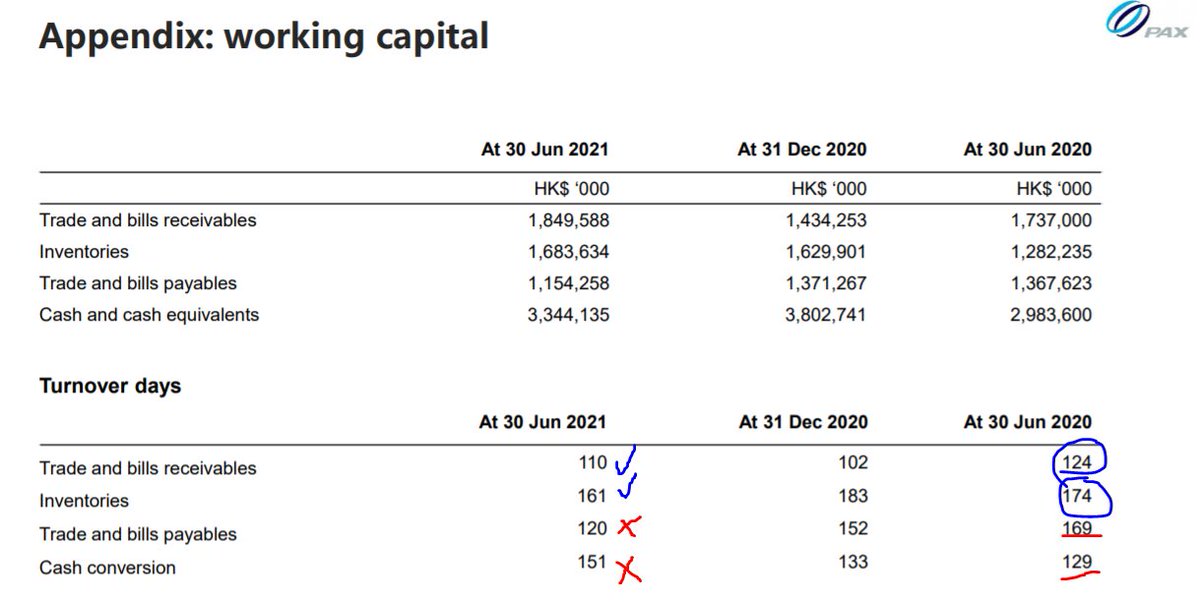

FCF generation is in line. It is seasonal, being the second half the strongest. Receivables and inventory were in line, but payables came lower than expected. Pax took advantage of its strong balance sheet to ensure the orders paying in advance (semis shortage). Temporal!

Pax is raising its annual targets. If semis shortage eases, I think Pax will beat their own aggressive targets. They are supply constrained and are investing in the Smart Terminal Industrial Park to expand production capacity from 12M to 22M

Pax stock is a bargain trading at 1.5x sales and 9x earnings. It is ridiculous for a business with moat and excellent management growing above 20%, buying back shares and raising the dividend (+72% yoy). Consensus 2021 eps is at HK$1, I expect Pax beating them by at least 5%.

Catalysts:

1. More broker coverage coming

2. Sunmi IPO. Xiaomi is looking to IPO its POS business in mainland China by the end of the year at 100-200x earnings. Sunmui gross margin is only 20% compared to 40% of Pax. Lower portfolio quality and sales (half of Pax sales)

1. More broker coverage coming

2. Sunmi IPO. Xiaomi is looking to IPO its POS business in mainland China by the end of the year at 100-200x earnings. Sunmui gross margin is only 20% compared to 40% of Pax. Lower portfolio quality and sales (half of Pax sales)

Sunmi IPO should attract mainland investors to Pax.

3. Indian customers IPO

4. Pax may be included in Shenzhen Stock Connect as soon as this year allowing PRC retail investors to invest in Pax. Currently, a mainland retail investor can't buy HK shares due to capital restrictions

3. Indian customers IPO

4. Pax may be included in Shenzhen Stock Connect as soon as this year allowing PRC retail investors to invest in Pax. Currently, a mainland retail investor can't buy HK shares due to capital restrictions

As I wrote, we added more shares after the amazing results thanks to market disconnection and we are not selling at the current prices. We expect a rerating and maintain our 2023 target of HK$ 20!

For those who read the full thread I will give a bonus. Pax Global 1H 2021 earning transcript attached

slideshare.net/GabrielCastroC…

slideshare.net/GabrielCastroC…

• • •

Missing some Tweet in this thread? You can try to

force a refresh