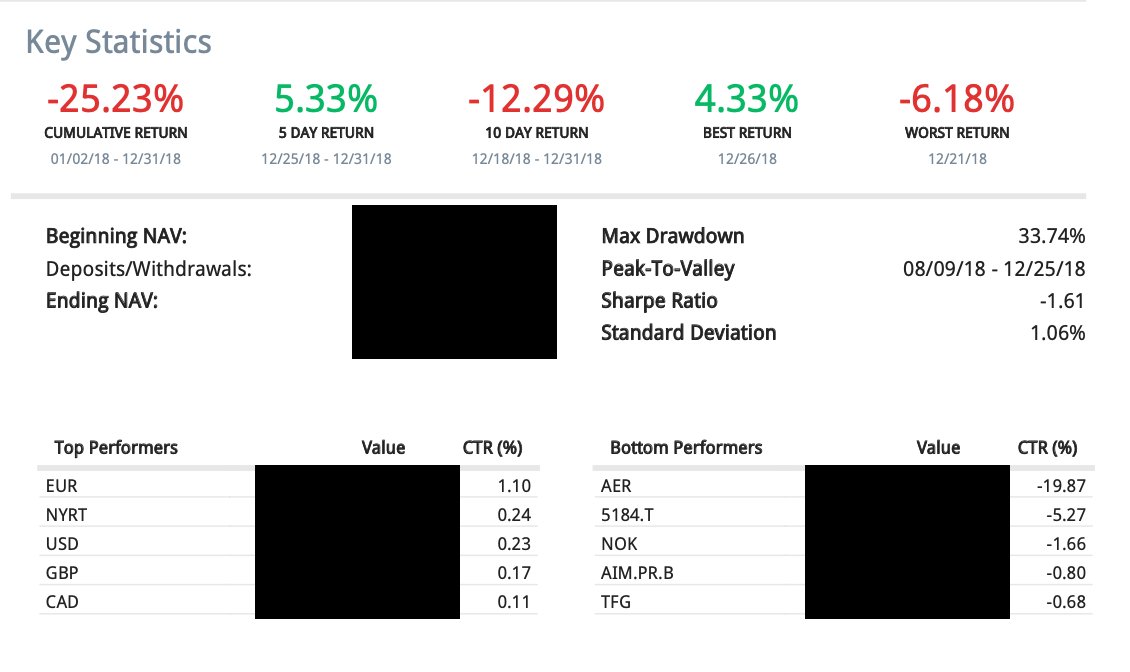

Since $HDG.NA is breaking out to new highs and I’m getting a fair few inbounds, let me open the kimono a little as to my thinking here…

https://twitter.com/puppyeh1/status/1425057564899758080

The short answer is not much has changed. Still (by far) my largest position w the best combo of absolute valuation; execution; and potential event/takeout catalyst.

I think tho some people are realizing the housing/renovation/remodel boom May well continue a good deal longer…

I think tho some people are realizing the housing/renovation/remodel boom May well continue a good deal longer…

Which is basically the message if you listen to most all the building products/home interior 2Q calls.

Maybe one/some woke up to the fact that this is one of the best quality building products names globally but still absurdly cheap (<5x EV/ebitda, unlevered).

Maybe one/some woke up to the fact that this is one of the best quality building products names globally but still absurdly cheap (<5x EV/ebitda, unlevered).

There have also been a number of high profile transactions that basically all occurred at multiples implying we are still mid-cycle for earnings power (Boral NA assets at 13-14x EV/ebitda, etc)

And of course the big one will be the Springs Window (global no2, after HDG) which should print shortly and rumor is well north of 10x EV/ebitda…

Obviously all this implying an HDG stock close or north of 200 EUR, let alone 100…

Which of course only underlines why I think the event angle remains in play….namely Sonnenberg coming back to bid again next April (when the window opens up)…

Which of course only underlines why I think the event angle remains in play….namely Sonnenberg coming back to bid again next April (when the window opens up)…

Because just like all of us they don’t know the future, and sonnenberg prob can’t wait a number of years for the cycle to turn (if it does).

Thus, at 100 or so the calculus is still basically the same. Risk/reward I can’t see anything ‘high beta’ that comes close to the setup…

Thus, at 100 or so the calculus is still basically the same. Risk/reward I can’t see anything ‘high beta’ that comes close to the setup…

And frankly I’m bemused when so many other investors are stumping up big cash to buy even minority stakes in inferior housing/building related businesses at 2-3x the multiple here…

Nothing really new but this basically sums up how i am thinking about it now. $HDG.NA

DYODD 🙏🏻👊🏻

Nothing really new but this basically sums up how i am thinking about it now. $HDG.NA

DYODD 🙏🏻👊🏻

• • •

Missing some Tweet in this thread? You can try to

force a refresh