So GitLab just hit a $15B market cap

It's one that just ... always was growing at epic rates, from YC Demo Day to IPO

It's growing a stunning 69% a year at $250,000,000+ in ARR

5 Interesting Learnings: 🔽🔽🔽🔽🔽

It's one that just ... always was growing at epic rates, from YC Demo Day to IPO

It's growing a stunning 69% a year at $250,000,000+ in ARR

5 Interesting Learnings: 🔽🔽🔽🔽🔽

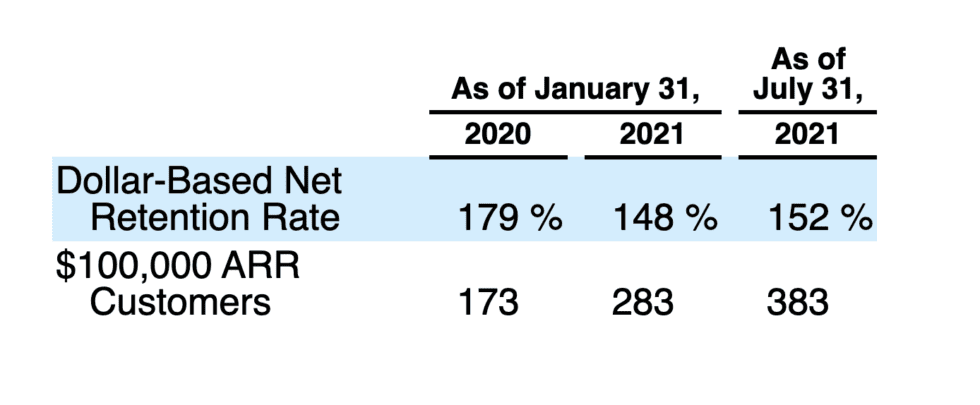

#1. 152% NRR from $100k+ customers.

We’re getting used to seeing these super-high NRR numbers from the top developer-focused leaders, in many cases because utility pricing often encourages it (see also Datadog, Twilio, etc). Still, these are truly top-tier numbers:

We’re getting used to seeing these super-high NRR numbers from the top developer-focused leaders, in many cases because utility pricing often encourages it (see also Datadog, Twilio, etc). Still, these are truly top-tier numbers:

#2. 97% GRR (Gross Retention Rate)

It’s great and helpful to see this broken out as well to compare yourself to. GitLab’s customers … stay. Almost all of them.

97% GRR is world-class. Service Now has 99% -- but their customers sign 3 year contracts!!

It’s great and helpful to see this broken out as well to compare yourself to. GitLab’s customers … stay. Almost all of them.

97% GRR is world-class. Service Now has 99% -- but their customers sign 3 year contracts!!

#3. GitLab China is a new independent company formed in 2021, both SaaS and self-managed, available only in China, Hong Kong and Macau.

We may see this more often

As LinkedIn and others retreat from China, GitLab goes all-in

We may see this more often

As LinkedIn and others retreat from China, GitLab goes all-in

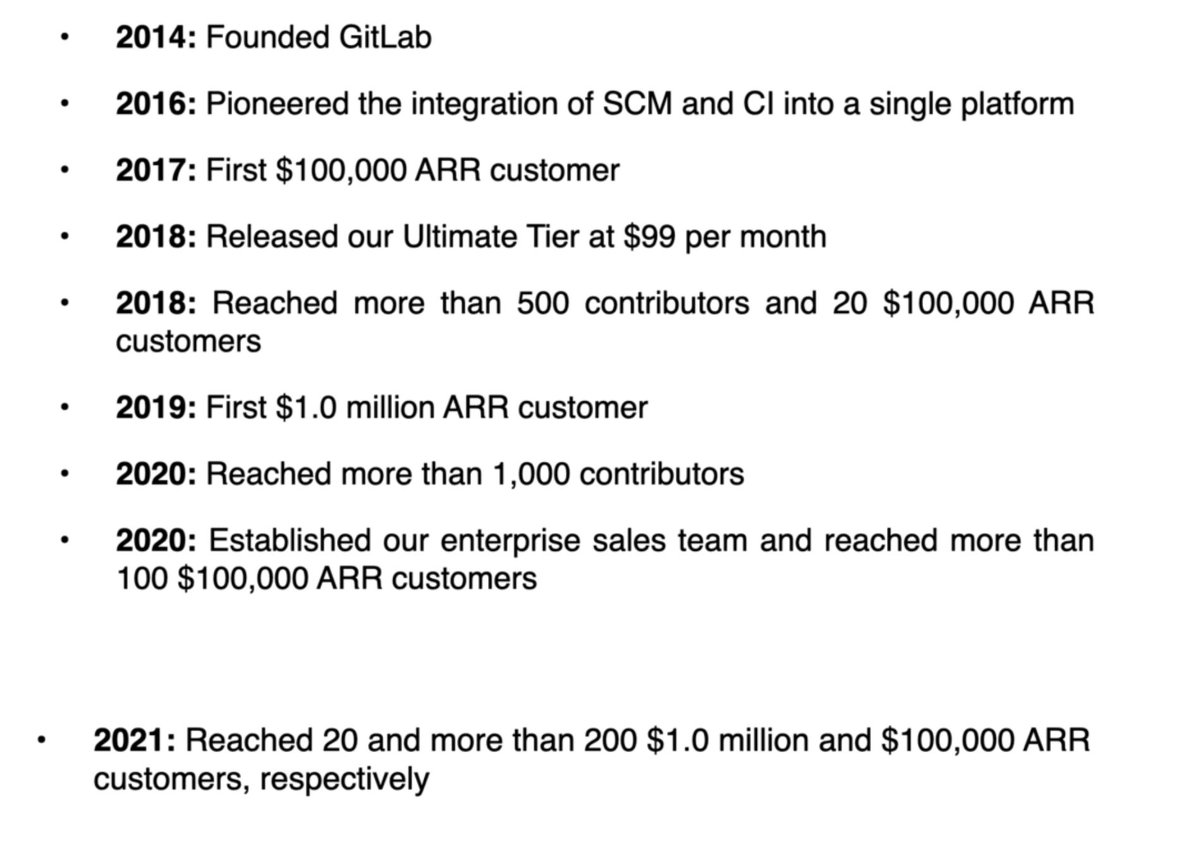

#4. First $100k customer in 2017. Then 20 by 2018. Then 100 by 2020 ... and 200 by 2021.

First $1m customer in 2019. Fast forward 2 years, and they have 20 $1m+ customers

A great chronology on going upmarket:

First $1m customer in 2019. Fast forward 2 years, and they have 20 $1m+ customers

A great chronology on going upmarket:

#5. Most customers still deploy GitLab to their own private or hybrid Cloud.

90% of GitLab’s customers pay by subscription — but most still self-manage the deployment. GitLab’s SaaS revenues are still just 20% of their revenues, although that’s up from 9% in 2020.

90% of GitLab’s customers pay by subscription — but most still self-manage the deployment. GitLab’s SaaS revenues are still just 20% of their revenues, although that’s up from 9% in 2020.

And a few bonus learnings:

#6. Most customers under contract pay annually or multi-year. Perhaps not a surprise, given the larger deal sizes

#7. GitLab has done a new release on 22nd of every month … for 118 months straight! A clear commitment to consistent innovation!

#6. Most customers under contract pay annually or multi-year. Perhaps not a surprise, given the larger deal sizes

#7. GitLab has done a new release on 22nd of every month … for 118 months straight! A clear commitment to consistent innovation!

#8. Define their “Base Customer” as ones at >$5k ACV

An interesting segmentation of core metrics

While GitLab has 15,356 customers, it focuses its metrics on 3,600+ ones with ACV of $5k+. While this makes sense as their core persona it also flatters a lot metrics like NRR

An interesting segmentation of core metrics

While GitLab has 15,356 customers, it focuses its metrics on 3,600+ ones with ACV of $5k+. While this makes sense as their core persona it also flatters a lot metrics like NRR

#9. CEO Sid Sijbrandij has been granted massive additional stock grants — but they are only worth massive amounts if the company’s stock price skyrockets.

To $50B+ in valuation:

To $50B+ in valuation:

• • •

Missing some Tweet in this thread? You can try to

force a refresh