Expensify was founded way back in 2008, in the dawn of mobile, and took 13 years to file to IPO

When Covid hit, the business was hit hard as travel stopped

But then ... it's roared back to 60% growth (!) at $140m ARR. And on to IPO shortly!

5 Interesting Learnings: 🔽🔽🔽🔽🔽

When Covid hit, the business was hit hard as travel stopped

But then ... it's roared back to 60% growth (!) at $140m ARR. And on to IPO shortly!

5 Interesting Learnings: 🔽🔽🔽🔽🔽

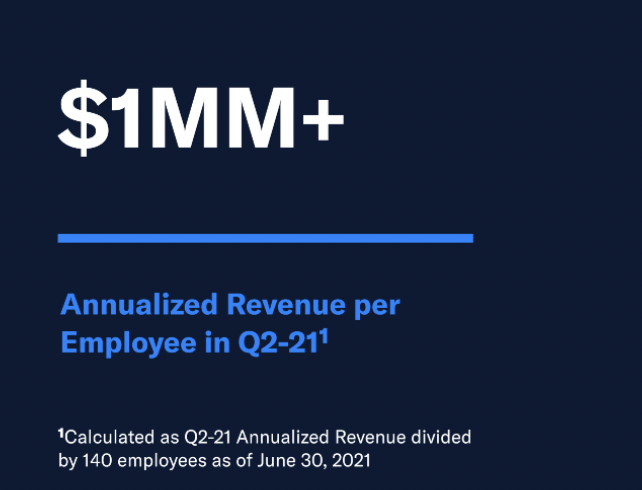

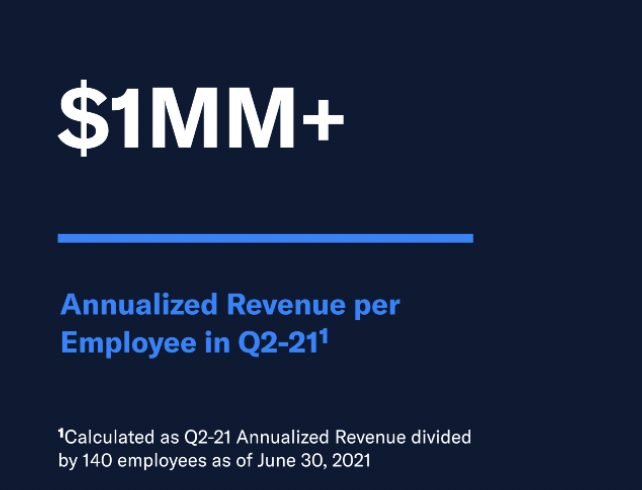

#1. Only 140 employees (!).

$1M in ARR per employee could be a new efficiency record at IPO for SaaS. Expensify kept it lean, maybe almost too lean. They raised little VC capital and became cash-flow positive.

$1M in ARR per employee could be a new efficiency record at IPO for SaaS. Expensify kept it lean, maybe almost too lean. They raised little VC capital and became cash-flow positive.

As part of that, they learned to outsource anything they could (vs hiring internally), and maximized the PLG playbook … leading to a stunning $1m in ARR per employee. We can’t all do this. But it shows it can be done.

#2. An incredible 60% of their revenue comes from "line" employees at companies using the free version on their own, for their own expenses ... and then socializing it to their “boss”, leading to paid conversion later.

PLG before it was hot:

PLG before it was hot:

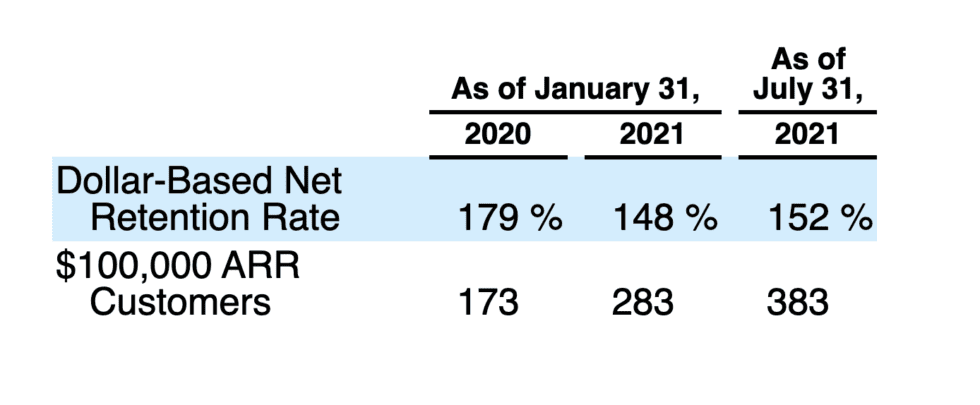

#3. GRR of 86% and NRR of 119% are very impressive for SMBs … although they only count customers with 5+ seats.

119% NRR from SMB is world-class even for 5+ seats accounts and something to strive for if you have similar-sized customers.

119% NRR from SMB is world-class even for 5+ seats accounts and something to strive for if you have similar-sized customers.

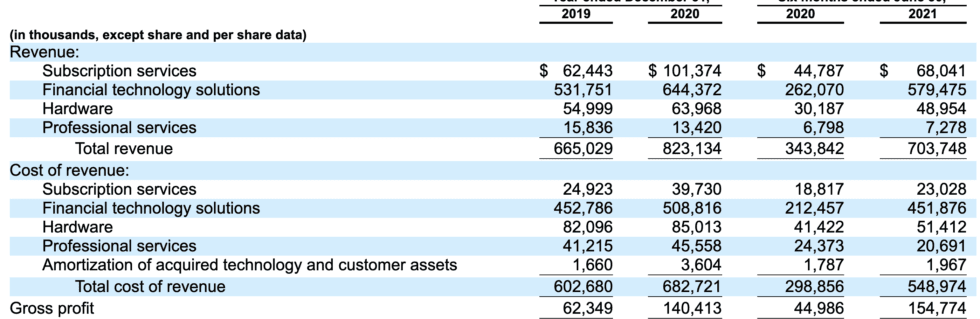

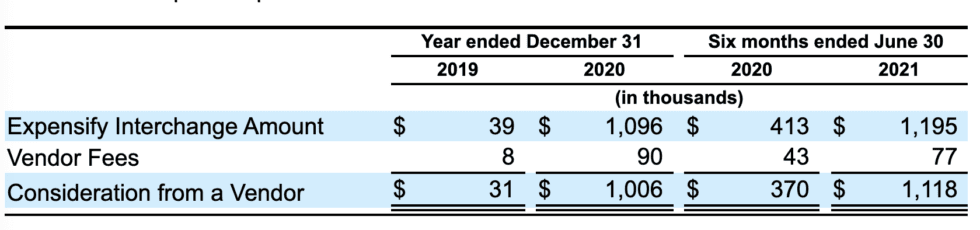

#4. Fintech a key engine of additional growth at scale.

Expense reports are core, but moving money is growth vector (grew 2.5x YoY), just like Shopify, Bill, and more

Expensify only launched credit card products just before Covid, but already contribution is material

Expense reports are core, but moving money is growth vector (grew 2.5x YoY), just like Shopify, Bill, and more

Expensify only launched credit card products just before Covid, but already contribution is material

#5. Growth of only 10% in 2019 to 2020 — but then exploded to 60%!

This is pretty incredible and also close to unprecedented. Covid was a big piece of it. But after adding more credit cards, payments, & coming out of Covid … boom!! From 10% growth to 60%. In one year.

This is pretty incredible and also close to unprecedented. Covid was a big piece of it. But after adding more credit cards, payments, & coming out of Covid … boom!! From 10% growth to 60%. In one year.

And a few bonus learnings:

#6. 90% U.S.-based revenue

Expense management has many localized components, and Expensify has been relatively slow to expand outside U.S., growing from 9% in 2019 to 11% in 2021. Expansion so far is limited to the U.K., Canada, and Australia.

#6. 90% U.S.-based revenue

Expense management has many localized components, and Expensify has been relatively slow to expand outside U.S., growing from 9% in 2019 to 11% in 2021. Expansion so far is limited to the U.K., Canada, and Australia.

#7. Average of 12 seats per customer.

With 639,000 paid members across 53,000 cos., the average customer pays for 12 seats. An SMB sale, but less & less a single-seat sale. 110%+ NRR from SMBs usually requires team-level functionality, & Expensify is a good case study here

With 639,000 paid members across 53,000 cos., the average customer pays for 12 seats. An SMB sale, but less & less a single-seat sale. 110%+ NRR from SMBs usually requires team-level functionality, & Expensify is a good case study here

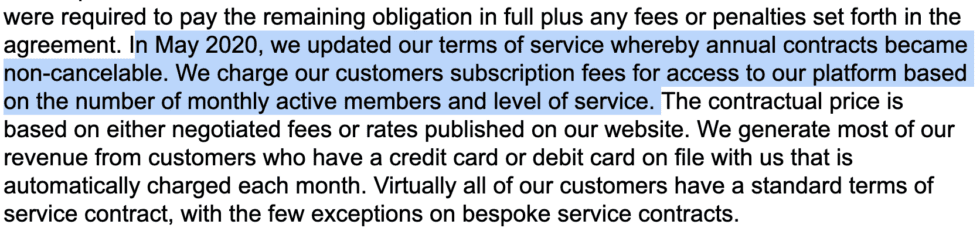

#8. Annual contracts used to be cancelable -- now aren’t

Expensify allowed customers to cancel annual contracts until May 2020. Most likely a change to get ready to IPO in part, & in part to stabilize things post-Covid

Expensify allowed customers to cancel annual contracts until May 2020. Most likely a change to get ready to IPO in part, & in part to stabilize things post-Covid

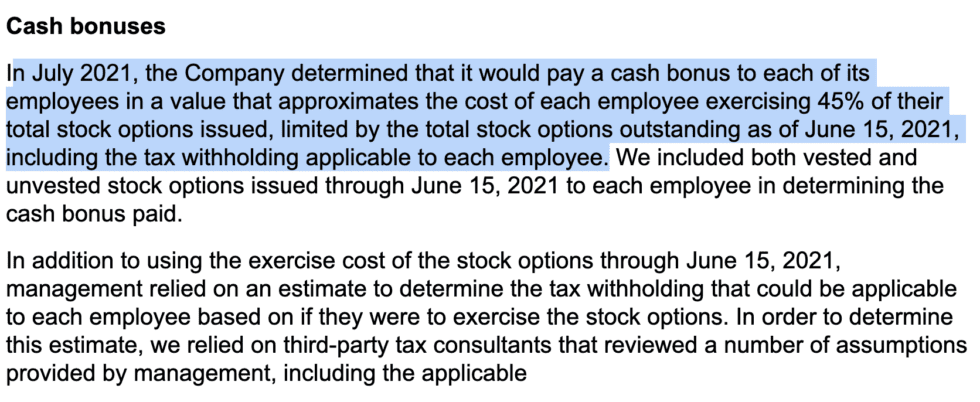

#9. Paid out cash bonuses to help employees buy their options / stock.

This is nice to see. The company paid out $9.5m to help employees pay the costs to exercise up to 45% of their options. The total amounts under this program are $30m-$36m.

This is nice to see. The company paid out $9.5m to help employees pay the costs to exercise up to 45% of their options. The total amounts under this program are $30m-$36m.

#10. Bought out one of their VCs for $43m

Founder-CEO Dave Barrett is famous for his views on the pros and cons of venture capital (see his talk from 2017 SaaStr Annual below) and he bought out the shares for $43m in 2018

Probably less likely today, in the Best of Times

Founder-CEO Dave Barrett is famous for his views on the pros and cons of venture capital (see his talk from 2017 SaaStr Annual below) and he bought out the shares for $43m in 2018

Probably less likely today, in the Best of Times

• • •

Missing some Tweet in this thread? You can try to

force a refresh