Bitcoin briefly beat its previous all-time-high, only to reverse lower. Short-term holders (less than 3 months) account for only 15% of all bitcoins, which remains below where it has been at most bottoms. So what's going on? (THREAD)

One thing: There’s now a retail vehicle for owning bitcoin, for those investors who don’t want to have to remember their keys. It may not be perfect but it might do for now. /2

In retrospect, some sort of buy-the-rumor, sell-the-news effect was to be expected, although the on-chain dynamics continue to show no signs of a speculative extreme. /3

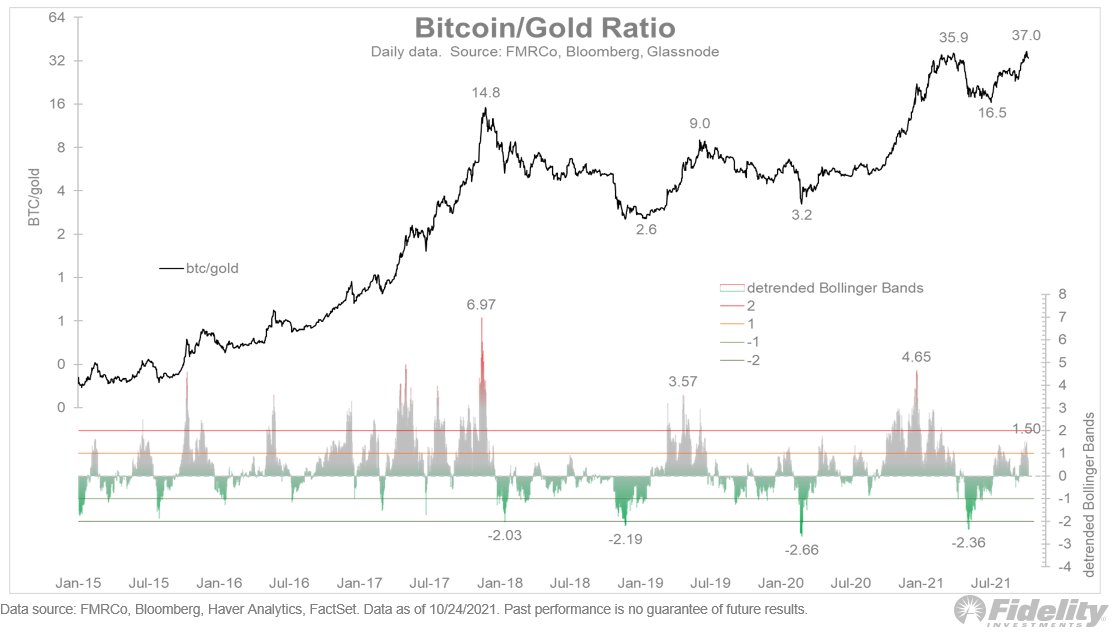

In addition, while the bitcoin-to-gold ratio is back to its all-time highs, on a detrended basis it looks to be far from overbought. Bitcoin is only one standard deviation above gold on a detrended basis. /4

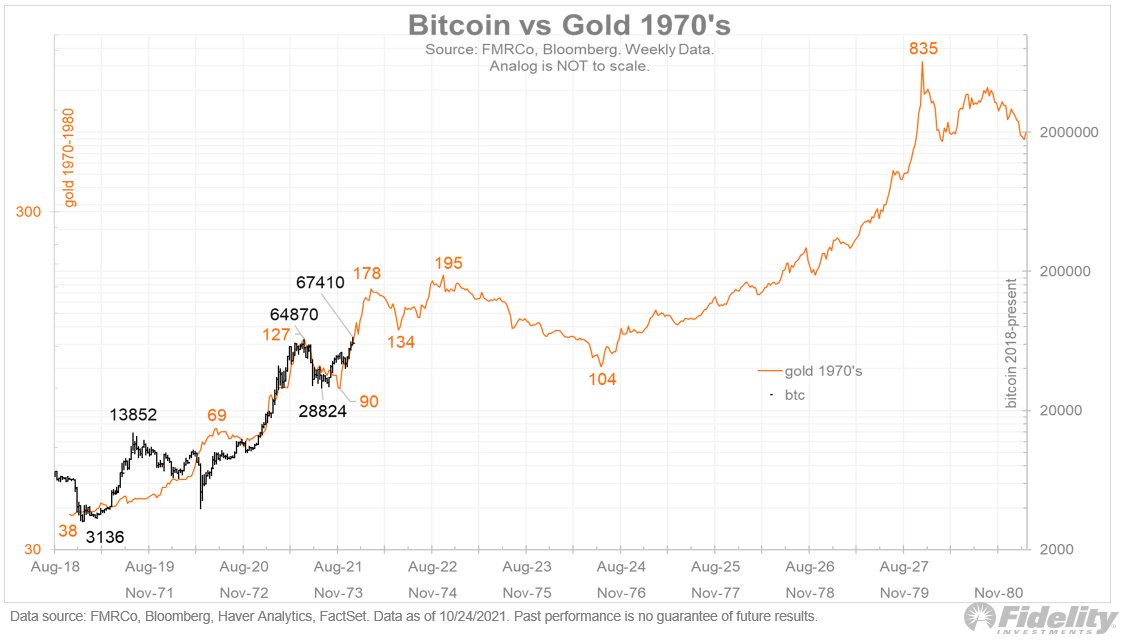

While price analogs are for entertainment purposes only, it’s interesting that my analog to gold in the 1970s continues to track closely. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh