We are adding a few more updates on other names. As always, we find these compelling 🤪 but DYODD.

6) $BWMX. Obvi v frustrating year. I often think if this biz had grown 15-20% in 2020 and then this year it would trade at a higher price than having grown 200% then stopped…

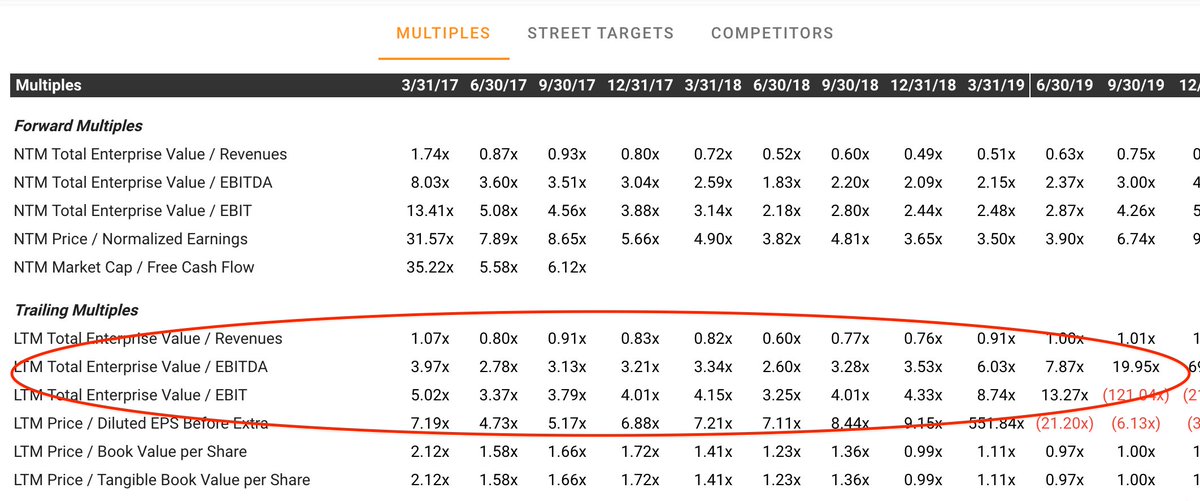

6) $BWMX. Obvi v frustrating year. I often think if this biz had grown 15-20% in 2020 and then this year it would trade at a higher price than having grown 200% then stopped…

https://twitter.com/puppyeh1/status/1461857467583778819

…there are a cpl of issues here re poor IR, lack of management communication, but ultimately this has rerated from high teens P/E to 8x when growth went to near zero. Incredible derate.

If you think they can return to teens growth - something management seems adamant on…

If you think they can return to teens growth - something management seems adamant on…

…then it’s a crazy bargain. They won’t get credit for it for at least one more qtr as 4Q will be weak, but I’ve been adding here and there. Stock just far too cheap, v yieldy while we wait.

7) Simonds $SIO.AX. Total dud so far (-20%) and I am bagholding. Maybe 2x EV/ebitda now.

7) Simonds $SIO.AX. Total dud so far (-20%) and I am bagholding. Maybe 2x EV/ebitda now.

Obvi horrible mgmt, poor M&A as I’ve moaned about. That said potential family catalyst of takeout still in play. Ownership triangle most beautiful resolved eventually. Prob a rough 6mos for the biz given cost escalation but I believe it’s in the price. Not a huge position.

8) Electra Private Equity $ELTA.LN. Both legs have trades weakly since split. Host more looks quite cheap now at 5-6x EV/ebitda but I am not confident in mgmt and thought portrayal of adjusted nos pre split was a bit misleading so I am OUT. Life is too short.

9) Mobruk $MBR.PW. Still core position. Incredible biz performance offset slightly by lack of activity in M&A. Mgmt doing most of the right things re IR. Sell down recently removed an overhang and stock breaking out. Still incredible to me you can buy this biz at <10x CY22 EPS

• • •

Missing some Tweet in this thread? You can try to

force a refresh