KPIT Technologies: The best Software Integration Company to invest in?

Here’s our analysis of KPIT Tech, the catalysts, valuations, risks, positioning and more!

A detailed thread below🧵🧵👇🏻

#investing #StocksToWatch

Here’s our analysis of KPIT Tech, the catalysts, valuations, risks, positioning and more!

A detailed thread below🧵🧵👇🏻

#investing #StocksToWatch

(1/16)

• KPIT Technologies Limited is an India-based technology company, which is focused on automobile engineering and mobility solutions.

• It also analyses data for diagnostics, maintenance & tracking of assets & related connectivity solutions, including data and analytics

• KPIT Technologies Limited is an India-based technology company, which is focused on automobile engineering and mobility solutions.

• It also analyses data for diagnostics, maintenance & tracking of assets & related connectivity solutions, including data and analytics

(2/16)

The Backdrop:

• As the auto industry shifts focus towards electric powertrains, R&D spending on CASE (connected, autonomous, shared, electric) technologies at the top 10 global auto R&D spenders is poised to grow multifold

• Europe will ban sales of ICE cars by CY35

The Backdrop:

• As the auto industry shifts focus towards electric powertrains, R&D spending on CASE (connected, autonomous, shared, electric) technologies at the top 10 global auto R&D spenders is poised to grow multifold

• Europe will ban sales of ICE cars by CY35

(3/16)

Why KPIT?

• Next leg of customers to come from semiconductor makers & EV disruptors : KPIT has started programs with EV disruptors & also started working with semiconductor cos to help them integrate their products to varied operating system architectures among OEMs.

Why KPIT?

• Next leg of customers to come from semiconductor makers & EV disruptors : KPIT has started programs with EV disruptors & also started working with semiconductor cos to help them integrate their products to varied operating system architectures among OEMs.

(4/16)

• Due to 100% focus on automotive software, they have high level expertise in high entry barrier domain, unlike many of its peers.

• Electronics, which were 27% of vehicle cost in 2010, currently account for 40%. KPIT excels in integration of Electronic parts.

• Due to 100% focus on automotive software, they have high level expertise in high entry barrier domain, unlike many of its peers.

• Electronics, which were 27% of vehicle cost in 2010, currently account for 40%. KPIT excels in integration of Electronic parts.

(5/16)

• 15%-20% of automotive R&D is outsourced today. As the role of software and electronics expands in the auto industry, OEMs will resort to more outsourcing in order to expand focus on core areas like vehicle operating system architecture. This will surely help KPIT!

• 15%-20% of automotive R&D is outsourced today. As the role of software and electronics expands in the auto industry, OEMs will resort to more outsourcing in order to expand focus on core areas like vehicle operating system architecture. This will surely help KPIT!

(6/16)

• KPIT Tech Revenue breakup:

1) Connected Vehicles - 10% ( Infotainment, Payments, Maps)

2) Autonomous driving & ADAS - 20% of the revenue

(Anti collision, Parking assist, etc)

3) Electric Powertrain - 30%

4) ICE Powertrain - 10%

5) Others - 30%

• KPIT Tech Revenue breakup:

1) Connected Vehicles - 10% ( Infotainment, Payments, Maps)

2) Autonomous driving & ADAS - 20% of the revenue

(Anti collision, Parking assist, etc)

3) Electric Powertrain - 30%

4) ICE Powertrain - 10%

5) Others - 30%

(7/16)

• KPIT’s two decades of experience working on more than 300 vehicle production programs have positioned it well to participate in higher entry barrier & newer technology areas in the global auto tech.

80% of its revenue comes from Higher Enter Barrier Practices

• KPIT’s two decades of experience working on more than 300 vehicle production programs have positioned it well to participate in higher entry barrier & newer technology areas in the global auto tech.

80% of its revenue comes from Higher Enter Barrier Practices

(8/16)

• Let’s look into CASE R&D spending:

1) KPIT works with more than 10 of the top 15 automotive OEMs globally, CASE spending is exp to grow multifold in the next 5 years.

2) Factors acting as catalysts are:

• Europe’s decision to ban sale of ICE vehicles starting 2035

• Let’s look into CASE R&D spending:

1) KPIT works with more than 10 of the top 15 automotive OEMs globally, CASE spending is exp to grow multifold in the next 5 years.

2) Factors acting as catalysts are:

• Europe’s decision to ban sale of ICE vehicles starting 2035

(9/16)

• Increasing regulatory penalties to auto manufacturers for non-compliance with CO2 emission standards

• Increasing activism across industries, governments and investors in relation to sustainability and decarbonization.

• Increasing regulatory penalties to auto manufacturers for non-compliance with CO2 emission standards

• Increasing activism across industries, governments and investors in relation to sustainability and decarbonization.

(10/16)

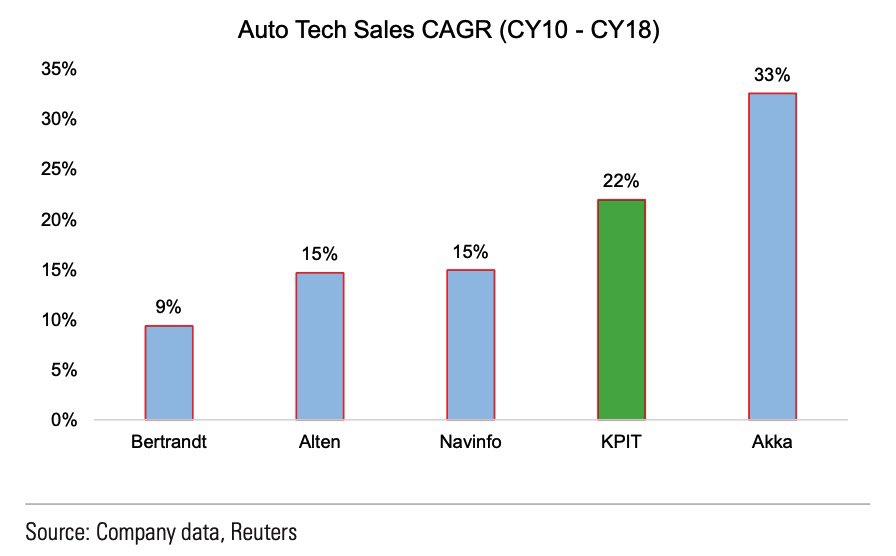

• KPIT’s Positioning among its global peers:

1) KPIT is one of the very few software integrators in the auto tech field which earns 100% of its revenue from auto tech end markets. This could boost its capability to win incremental share of contracts in this space

• KPIT’s Positioning among its global peers:

1) KPIT is one of the very few software integrators in the auto tech field which earns 100% of its revenue from auto tech end markets. This could boost its capability to win incremental share of contracts in this space

(11/16)

2) KPIT’s dedicated auto headcount of ~6,400 is among the top 3 in comparison to the broader peer group, trailing only Bertrandt and Akka.

3) Outsourcing in middleware and integration likely to grow and KPIT is positioned perfectly to benefit from this

2) KPIT’s dedicated auto headcount of ~6,400 is among the top 3 in comparison to the broader peer group, trailing only Bertrandt and Akka.

3) Outsourcing in middleware and integration likely to grow and KPIT is positioned perfectly to benefit from this

(12/16)

4) In comparison to some peers which are exclusively focused on segments like autonomous or navigation, KPIT offers a broad range of CASE solutions to customers including Infotainment, electrification, autonomous, mobility solutions, vehicle diagnostics & others

4) In comparison to some peers which are exclusively focused on segments like autonomous or navigation, KPIT offers a broad range of CASE solutions to customers including Infotainment, electrification, autonomous, mobility solutions, vehicle diagnostics & others

(13/16)

• KPIT has been consistently winning a mix of both large (£50mn+) & small deal. The consistent pattern of business wins from key customers gives us confidence in KPIT’s ability to execute on existing client offering a good foundation to pitch for new customers

• KPIT has been consistently winning a mix of both large (£50mn+) & small deal. The consistent pattern of business wins from key customers gives us confidence in KPIT’s ability to execute on existing client offering a good foundation to pitch for new customers

(14/16)

• Valuation:

• Valuation:

(15/16)

• KPITs expertise in High entry barrier areas, having the third largest talent pool globally, addition of semiconductor and EV disruptors cos to its client base, rise in CASE R&D spending & increasing share in new technology areas all bodes well for its future!

• KPITs expertise in High entry barrier areas, having the third largest talent pool globally, addition of semiconductor and EV disruptors cos to its client base, rise in CASE R&D spending & increasing share in new technology areas all bodes well for its future!

(16/16)

What do you think about KPIT and it’s growth prospects?

Comment down below and don’t forget to hit the retweet!

@PAlearner @KirtanShahCFP @caniravkaria @nid_rockz @sahil_vi @datta_arvind

What do you think about KPIT and it’s growth prospects?

Comment down below and don’t forget to hit the retweet!

@PAlearner @KirtanShahCFP @caniravkaria @nid_rockz @sahil_vi @datta_arvind

• • •

Missing some Tweet in this thread? You can try to

force a refresh