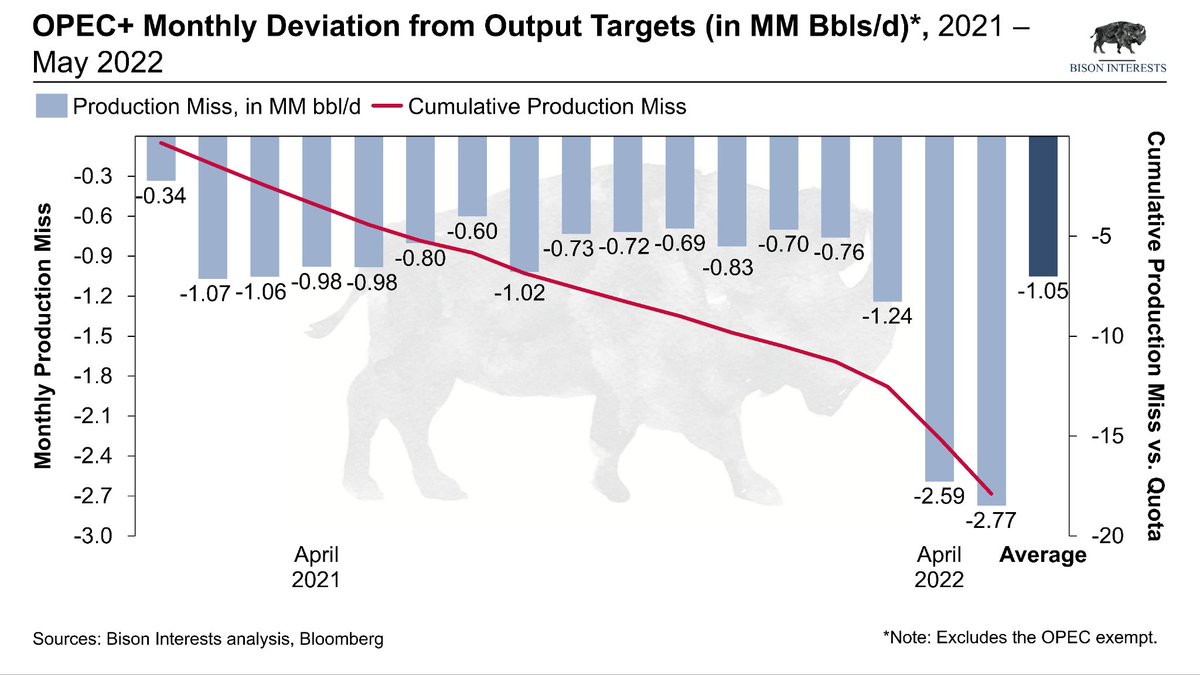

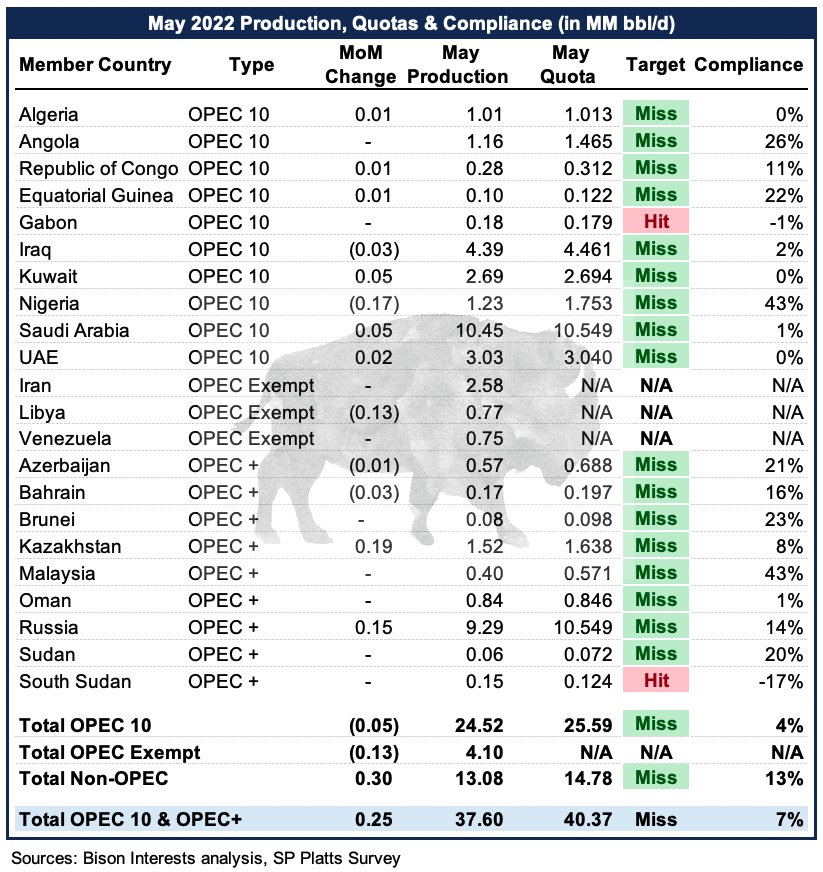

OPEC+ missed their #oil output target even more in May. Short thread with charts. 🧵

This was the worst month for OPEC+ since we started sharing comments on this. Highlights (all in MM bbl/d):

Total production for OPEC+ countries (excluding the OPEC exempt) was 37.60, falling short of the 40.37 quota by 2.77 MM bbl/d.

OPEC 13 production increased by 0.25, 0.15 short of their target increase

OPEC 13 production increased by 0.25, 0.15 short of their target increase

17/19 OPEC+ countries (excluding the exempt) missed their production quotas, the highest number of misses ever since we started sharing comments on this.

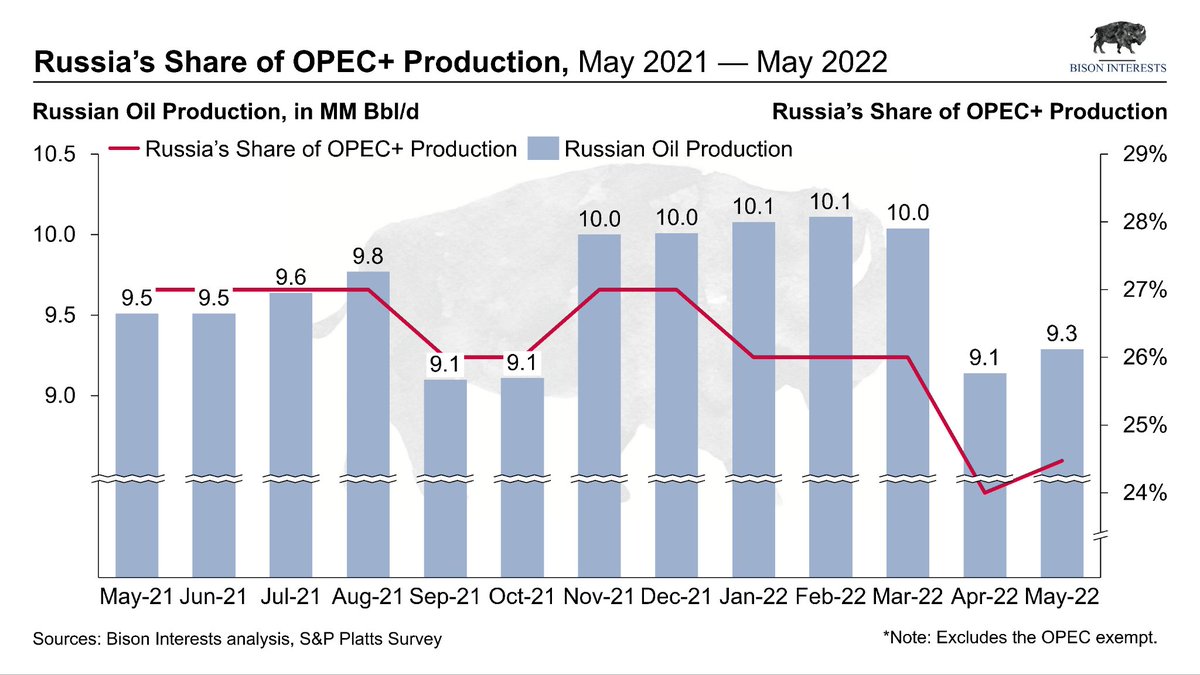

Russian production is up materially, for now. Worth noting.

Our original white paper on "The Myth of OPEC+ Spare Capacity" bisoninterests.com/content/f/the-…

And the updated and more in depth "OPEC+ Spare Capacity is Insufficient Amid Global Energy Crisis"

bisoninterests.com/content/f/opec…

bisoninterests.com/content/f/opec…

• • •

Missing some Tweet in this thread? You can try to

force a refresh