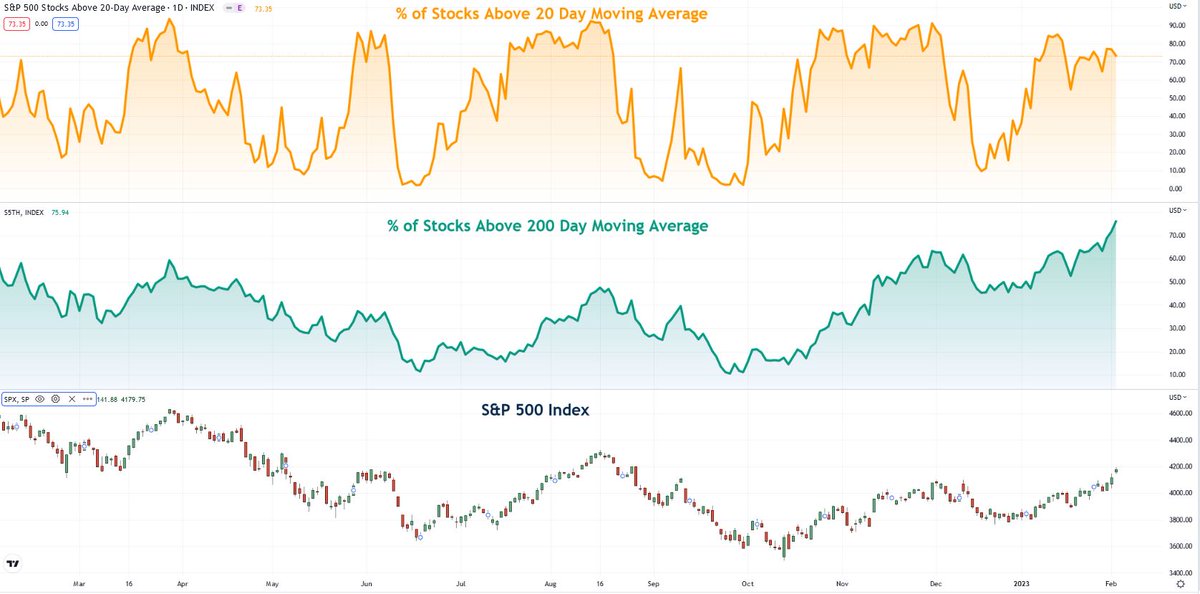

#SPX $SPY Breadth Ratio update 🧵:

This situation continues to get more intriguing. After the rally the last 2 days, I expected this signal to be resoundingly rejected

But the % of stocks > their 20 day MA relative to those above 200 MA has fallen below 1... 1/4

$QQQ #stocks

This situation continues to get more intriguing. After the rally the last 2 days, I expected this signal to be resoundingly rejected

But the % of stocks > their 20 day MA relative to those above 200 MA has fallen below 1... 1/4

$QQQ #stocks

https://twitter.com/andycwest/status/1620230875542847488

2/4 Whats this really showing?

Individual components of the ratio shown below

An increasing % of #stocks are above their 200 MA as expected in a rally, but the % above their 20 MA is flat potentially presaging declining momentum of the rally...

$SPY $QQQ #SPX

Individual components of the ratio shown below

An increasing % of #stocks are above their 200 MA as expected in a rally, but the % above their 20 MA is flat potentially presaging declining momentum of the rally...

$SPY $QQQ #SPX

3/5 When the % > 200MA is very high like now, but the % > 20 day MA starts to weaken, then we typically conclude the rally is in late stage and at risk

This may not be yet - as seen in orange the % > 20DMA can fluctuate at highs for a while. But given some weakening 2day...

This may not be yet - as seen in orange the % > 20DMA can fluctuate at highs for a while. But given some weakening 2day...

4/5 even as the market as a whole rallied, it bears close watching.

There is a LOT of ROTATION underneath the surface of this market that I will post separately. Materials stocks down, tech up (past winners dwn, losers up). Given size of tech generals, its carrying the market...

There is a LOT of ROTATION underneath the surface of this market that I will post separately. Materials stocks down, tech up (past winners dwn, losers up). Given size of tech generals, its carrying the market...

as a whole. Moving away from tech, the DJIA was flat showing another view of a different set of exposures.

Point being - this breadth ratio bears watching closely, as does rotational dynamics to look under the surface of the $SPY movements after such a strong January 5/5

Point being - this breadth ratio bears watching closely, as does rotational dynamics to look under the surface of the $SPY movements after such a strong January 5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh