PM @ Segra Capital Managment (@segracapital). Focused on niche & under-followed investment opportunities. Strong advocate for Nuclear Power.

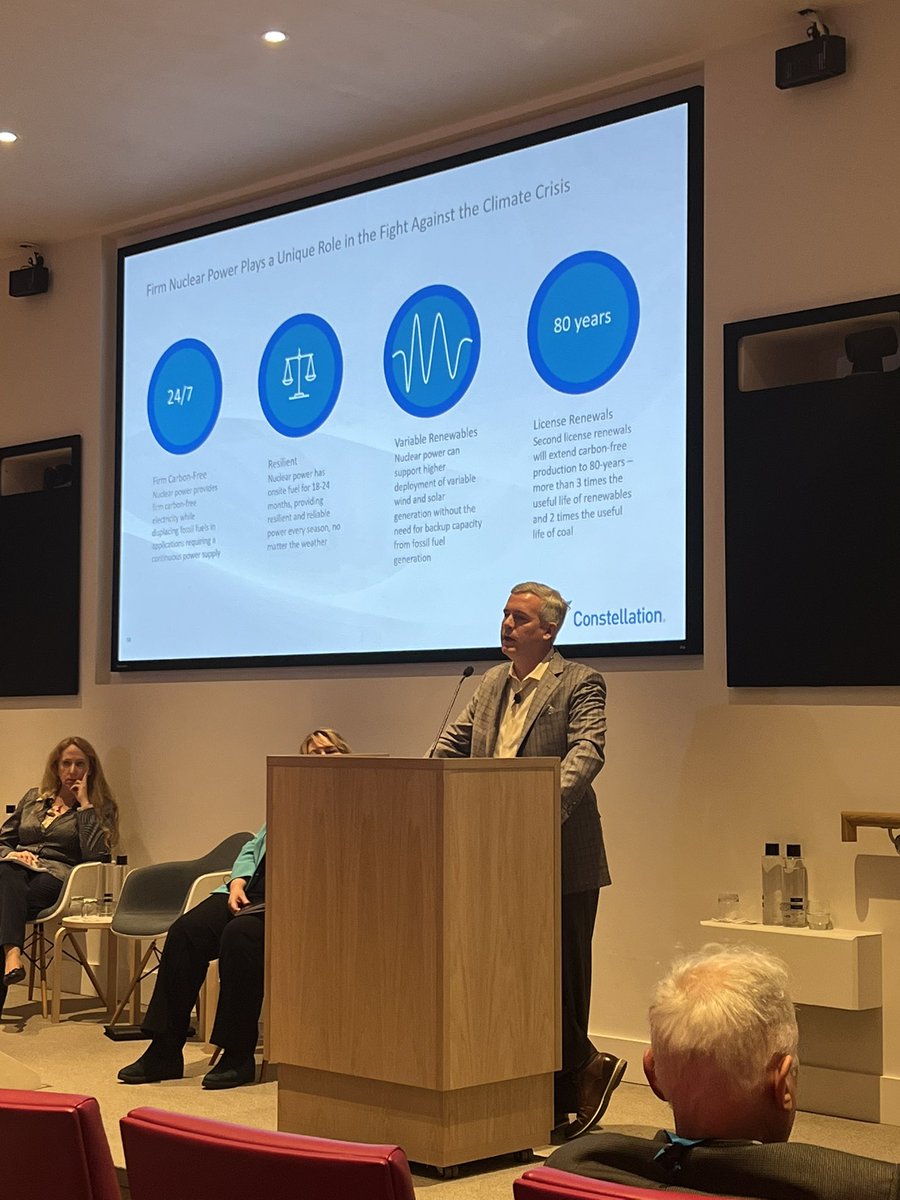

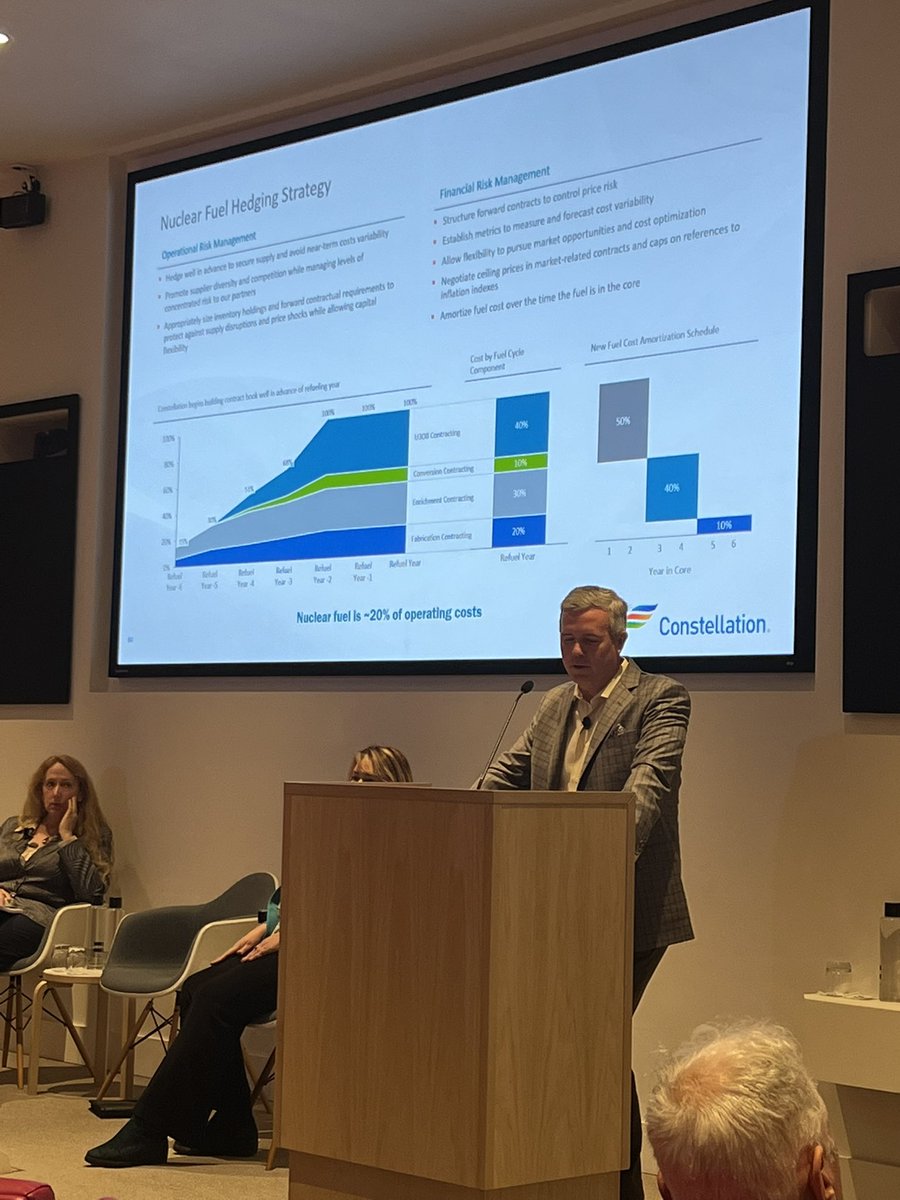

Jason Murphy from @ConstellationEG giving a great talk on the company’s #nuclear fleet - very impressive stats all around. Emphasized that the company intends to pursue life extensions to 80 years for the whole fleet. Also- contracting strategy starts 6 years before any reload!

Jason Murphy from @ConstellationEG giving a great talk on the company’s #nuclear fleet - very impressive stats all around. Emphasized that the company intends to pursue life extensions to 80 years for the whole fleet. Also- contracting strategy starts 6 years before any reload!