And just as monetary policy in the U.S. considers the weakest links in the global economic chain, we expect the #ECB to stay on a path of easy policy as they set out to accommodate the weakest links in the #Eurozone.

Hence, we like owning #assets with a low, or declining, cost-of-capital (r), as per the Gordon Growth Model, which given the posture of global central #banks, is the case in much of the world today…

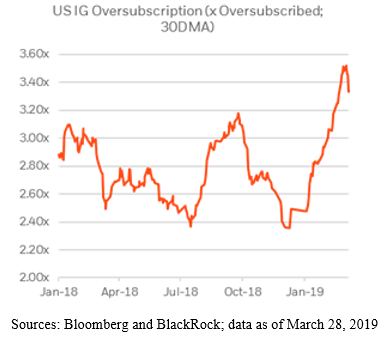

We also like high-quality carrying #assets with some scarcity value, such as U.S. corporate #bonds, where supply this year is almost half of what it was three years ago.

At the same time, demand for corporate bonds is at multi-year highs, fueled by the #demographic need for #income.

Finally, to #hedge risky positions, we like owning U.S. Treasuries and dollars for similar scarcity reasons, as well as their now-entrenched negative #correlation to risky assets.

• • •

Missing some Tweet in this thread? You can try to

force a refresh